7 from 7

Once a quarter, we have a crack at answering the most common questions we get from our clients. We try to be clear and simple in our responses. We tend to find that the September edition ends up a little bit more meaty, in terms of both questions and answers – maybe because people switch off from the markets over summer, and come back with lots of fresh thoughts!

1. Are we worried about a slowdown in economic growth – and what does it mean for our positioning?

Ben

Simply, no. The slowdown (if it’s happening at all) is temporary. Growth is coming, and our portfolios are ready for it.

At the moment, investors are finding it hard to let go of the thought patterns which guided them post-Global Financial Crisis – low growth, low inflation, and low confidence. Around 18 months on from the start of the COVID-19 pandemic, and they’re already worrying about the next recession. So, every positive growth indicator is viewed as temporary, and every negative one is taken to be structural, or systemic, or secular.

We think that view is wrong. We believe that the next decade will be different from the last, and that we’ll see a stronger economic cycle. People are ready to spend while governments are thinking about the future, and business confidence is surging as a result. More confidence means more spending, which creates more jobs and more demand; a virtuous circle leading to a genuine wave of growth.

In our portfolios, you’ll see tilts towards the “new cycle” winners, with equity investments in undervalued sectors and regions, such as industrials, mid-caps and emerging markets, at the expense of the large US tech stocks.

It can take time before investors acknowledge the new cycle, though, as Ahmer pointed out in his Q3 Investment Update, called “We spent the last year tilting our portfolios towards the new economic cycle. Now we wait…”

2. Is inflation going to break everything, and what should we do?

Salim

Inflation will be higher in the next decade than the last. Wage growth is strong, globalisation is slowing, and central bankers want more inflation. But, that isn’t a bad thing.

When talking about inflation, people seem to forget that central banks have inflation targets because some inflation is good for growth. In more developed countries, inflation has been below these targets for some time, and so has growth! Unless we want the whole world to have Japan’s experience of no inflation and no growth since the 1980’s, we should be welcoming some inflation.

There’s a lot of noise around supply chain issues at the moment – and lots of it is justified. But supply chain disruptions are likely to be localised and temporary, solved by the normal mechanism of supply and demand. Take wood prices in the US, for example; it quadrupled at the start of 2021 before falling back to where it started within six months.

What happened? As prices increased, lumberyards cut more trees, to make more money. Now, though, there’s about the right amount of wood to keep the market steady. The same will be true of semi-conductors, new cars, building supplies, and iPhones. It’s capitalism at work, reining in short-time price dislocations, therefore keeping inflation contained.

Source: Bloomberg Finance L.P. /7IM

Of course, if inflation is picking up, it’s natural to ask about the likelihood of and impact of interest rate hikes.

Predicting exactly when rate hikes will happen is a fool’s game. Unless you are Chair of the Federal Reserve (in which case, “hi, Jerome, thanks for reading!”), you really won’t be able to call it. At some point, central banks will have to begin a hiking cycle; it’s a question of when, not if.

But this doesn’t mean that we can’t prepare for rate rises. Our portfolios are all-weather by design, and we’ve got a few tactical positions which are also designed to do well in a rising-rate environment: underweight government bonds, overweight alternatives, overweight value and underweight tech.

3. How long can the Nasdaq (US tech sector) continue with its record climb?

Ben

In an absolute sense, the NASDAQ should keep rising. This isn’t the dotcom-boom NASDAQ; it’s full of lots of companies that have great business models and make a huge amount of money. As Salim noted a few months ago, all-time highs are to be expected in a growing world.

But, the real question is whether the NASDAQ can keep rising more quickly than the broader market – will mega-cap tech/internet companies continue to do better than the other sectors?

As mentioned above, once economic growth gets going, we think this will lead to investors starting to re-evaluate the relative attractiveness of the Googles, Apples and Amazons of the world. It’s not that they won’t be making money – just that other sectors might be making more.

There’s a lot of capital spending going on across the corporate world at the moment, as companies use the innovations of the last decade to improve their productivity. The winners of the next cycle will be users of technology, rather than creators of it. Again, as I said before, it might take a while for investors to realise this – but, they will.

4. Do the recent government interventions in China create opportunities to invest, or do they make the market less attractive?

Ben

In the short term, the recent interventions are a reminder of the types of extra risks which investors take in emerging markets – simply part of the territory, like defaults, coups or natural disasters. In the long term, this doesn’t change our view that investor allocations to China are only going to increase.

It is helpful to remind ourselves of the timelines on which China operates; which are far longer than most Western parliamentary democracies. The famous five-year plans are actually just stepping-stones. The real, long-term aim of President Xi is that by 2035, China should double its GDP from the $15 trillion 2020 level and triple its GDP per capita to $30,000.

That plan requires more investment and capital market involvement, from both domestic Chinese investors and foreigners. Of course the Chinese government will want to have control over businesses in a way which might feel unfamiliar to the West (although lots of European governments do have “golden shares” in nationally important companies, which isn’t a million miles off). But that is likely to be the price that investors pay, if they want to be part of the biggest growth story of the next century.

If you’ve got the right time horizon, and a strong stomach, President Xi just put Chinese assets on sale.

5. “Classic” 60/40 portfolios still seem to be churning out performance. Why do we think that’s going to end?

Ben

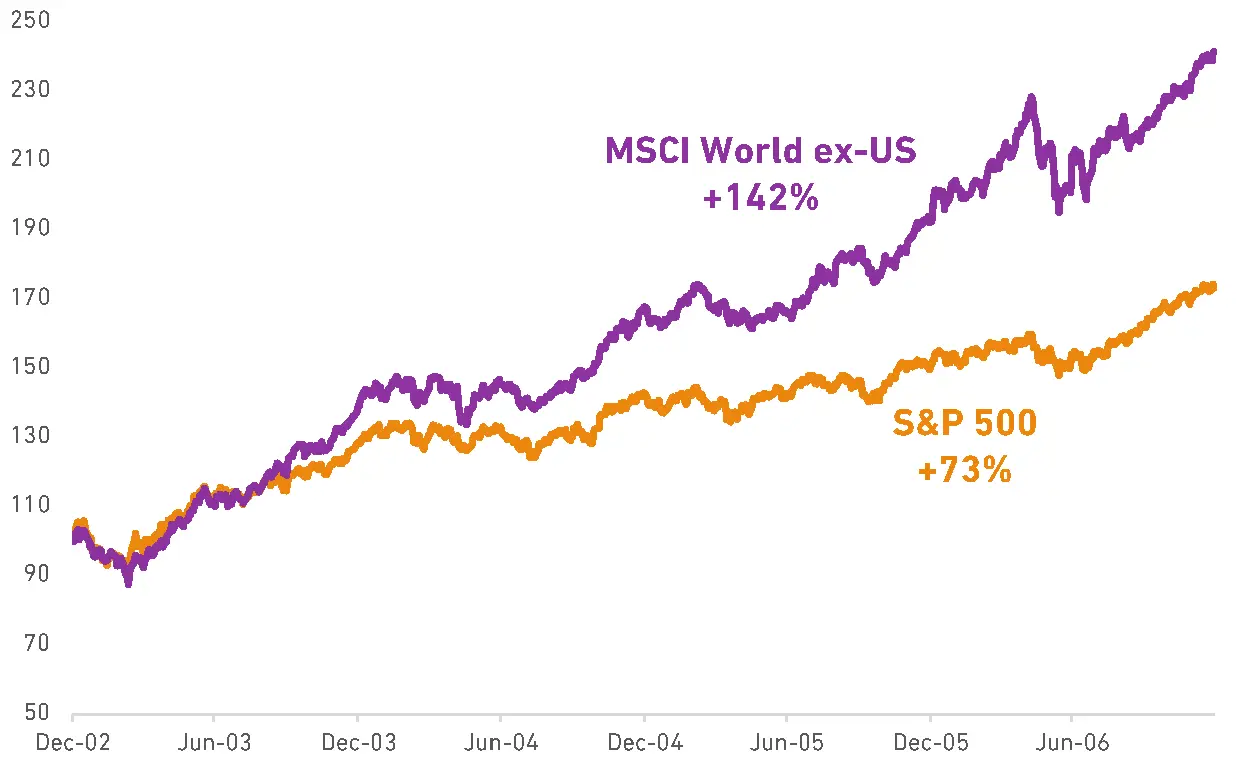

First, the equity part. The “60” tends to be dominated by US equities, which are dominated by technology companies, which drove the past cycle. And after such a long time, we lose the ability to think of a world in which US equities don’t dominate.

But, it wasn’t so long ago that things were different. After a long period of US outperformance in the late 1990’s, US equities underperformed non-US global stocks by 70% between 2003 and the end of 2006 (see below)! In that environment, the equity part of the conventional, US-heavy 60-40 portfolio would have significantly underperformed a more geographically diversified index.

Second, the “40” is usually allocated to government bonds. Let’s be clear, defensive bonds absolutely DO have a part to play in a diversified portfolio.

However, we think investors should also allocate to higher yielding parts of the fixed-income universe, and towards alternatives. As interest rates begin to grind upwards again, investing in bonds which have a little more protection in the form of higher coupon payments will be beneficial – as will investing in an alternative portfolio which has no correlation at all to interest rates.

Source: Bloomberg Finance L.P. /7IM

6. Why do we think we are in a world of lower returns - we can clearly see strong/consistent market performance?

Salim

It is true that most equity markets have been doing well. Although, let’s acknowledge that people weren’t predicting that outcome in the summer of 2020! But, more importantly, as multi-asset investors, we think about portfolio returns.

The majority of our portfolios contain more than just equity; they also contain bonds, and as we all know, yields are historically very, very low. Unlike with equities, the returns that you get from a bond are largely driven by the yield – the best expected return predictor for a bond is the yield you buy it at. UK government bonds currently pay a rate of 0.75% a year, for ten years.

So, without saying anything about equities, the returns you’re getting from bonds are lower, so you would expect portfolio returns to be lower.

But that’s not the end of the story. Matthew Yeates, our head of Alternatives and Quantitative strategy writes about it here.

7. Are we ‘walking the walk’ with our ESG proposition? Is our business making the same difference as our investment products?

Salim

Yes. In lots of ways – a few here below:

Structural investment

In our existing investment propositions, we are building ESG factors into our Strategic Asset Allocation (SAA). This means that the foundation of our investment process takes ESG scores into account, and we have a goal of reducing overall SAA emissions by 30% over a 5-year period. The work isn’t finished either…

Tactical investment

We have a position in our portfolios which is specifically aimed at benefitting from the transition to a greener economy. Terence Moll wrote about it in his recent piece.

Third-party review

We have also developed an ESG questionnaire and rating system for third-party managers that are held in our funds. It covers all broad ESG themes: firm; staff and stakeholder engagement; strategy and investment process; and voting and engagement. By having our own ESG questionnaire and rating system, we can engage with third party fund managers in a more structured way, focussing on the elements of ESG that we consider most important.

Corporate level initiatives

This is an investment-focussed Q&A so we’ll leave the rest to our sustainability and stewardship team; check back regularly for more here.

We believe that the next decade will be different from the last, and that we’ll see a stronger economic cycle.

Discover more