Monthly commentary

Portfolio Performance

At 7IM, we believe that taking a long-term view is essential when investing. We can’t always avoid the short-term bumps and shocks that the financial world has in store, but a well-diversified portfolio goes a long way towards smoothing out some of the journey. The long-term nature of our strategic and tactical process is a good complement to the Succession Matrix Expected Parameters.

| Q2/2018 - Q2/2019 | Q2/2019 - Q2/2020 | Q2/2020 - Q2/2021 | Q2/2021 - Q2/2022 | Q2/2022 - Q2/2023 | 3 Year Ann. Return | 5 Year Ann. Return | Succession Matrix Expected Parameters – Ann. Return | |

|---|---|---|---|---|---|---|---|---|

| Defensive | 2.84% | 3.35% | 4.61% | -5.95% | -1.55% | -1.05% | 0.58% | 3.0 - 4.5% |

| Cautious | 2.45% | 2.74% | 8.37% | -5.50% | 0.36% | 0.92% | 1.59% | 4.5 - 6.0% |

| Balanced | 2.08% | 1.96% | 12.90% | -5.09% | 2.80% | 3.28% | 2.77% | 5.2 - 7.5% |

| Moderately Adventurous | 1.59% | 0.44% | 17.07% | -4.27% | 5.04% | 5.59% | 3.73% | 6.0 - 8.0% |

| Adventurous | 1.45% | -0.95% | 20.11% | -3.83% | 5.63% | 6.86% | 4.16% | 7.0 - 10.0% |

| Income | 5.40% | -2.60% | 11.95% | -4.99% | 1.19% | 2.48% | 2.02% |

Source: 7IM/FE. Annualised return is defined as ‘Ann. Return’ in the performance table above and is as at end July 2023. Market returns have been poor in absolute terms since the beginning of 2020 with the Covid pandemic and then the inflationary shock of 2022. While portfolios have held up well relative to peers, the 3 and 5 year absolute returns are lower than average, even though the since inception longer term numbers are in line with expected parameters.

Summary

July has been a pretty busy month. The world experienced the hottest month on record, Alcaraz won his first Wimbledon title, ‘Barbenheimer’’ box office sales soared, Twitter lost its wings, and back at home, we have seen a ‘Farage vs. Banks’ battle brewing.

The financial markets have also been dealing with lots of events this month, so let’s take a closer look:

- Sticking to the inflation fight… In line with market expectations, central banks continued their fights against rising inflation. Across the pond, the Fed hiked rates by 25bps to a 22-year high after a “break” in June. In the Eurozone, the ECB is determined to return inflation to its 2% medium-term target, also raising rates as a result. The Bank of Japan also joined the tightening wave after decades of monetary stimulus, which surprised the market a little, sending Japanese yields to a nine-year high.

- In the midst of rate hikes, global equity markets have been buoyant:

| Index | July performance |

|---|---|

| S&P 500 | 3.2% |

| Nasdaq | 3.8% |

| FTSE 100 | 2.4% |

| Eurostoxx 50 | 1.8% |

| TOPIX | 1.5% |

With everyone piling into stocks, the S&P 500 and Nasdaq continue to lead the party. The long streak of monthly gains shows the market remains bullish following stronger-than-expected growth data, corporate earnings, and cooling inflation. The AI mania remains a driver of performance of US stocks. As the Q2 earnings start to come out in August, the mega-cap Magnificent Seven will have to show they’re worth the hype.

- Positive economic rumbles in Beijing… China signalled more support for the real estate sector, which has been in a multi-year growth drag, and to boost domestic consumption. Hope is running high, as Chinese equities had their largest rally since January and the gains continue into August.

Portfolio Positioning and Changes

During July, we did not make any major changes to portfolios.

Core investment views

At 7IM, we have a number of long-term core views that help to guide our investment decisions and allocations within portfolios.

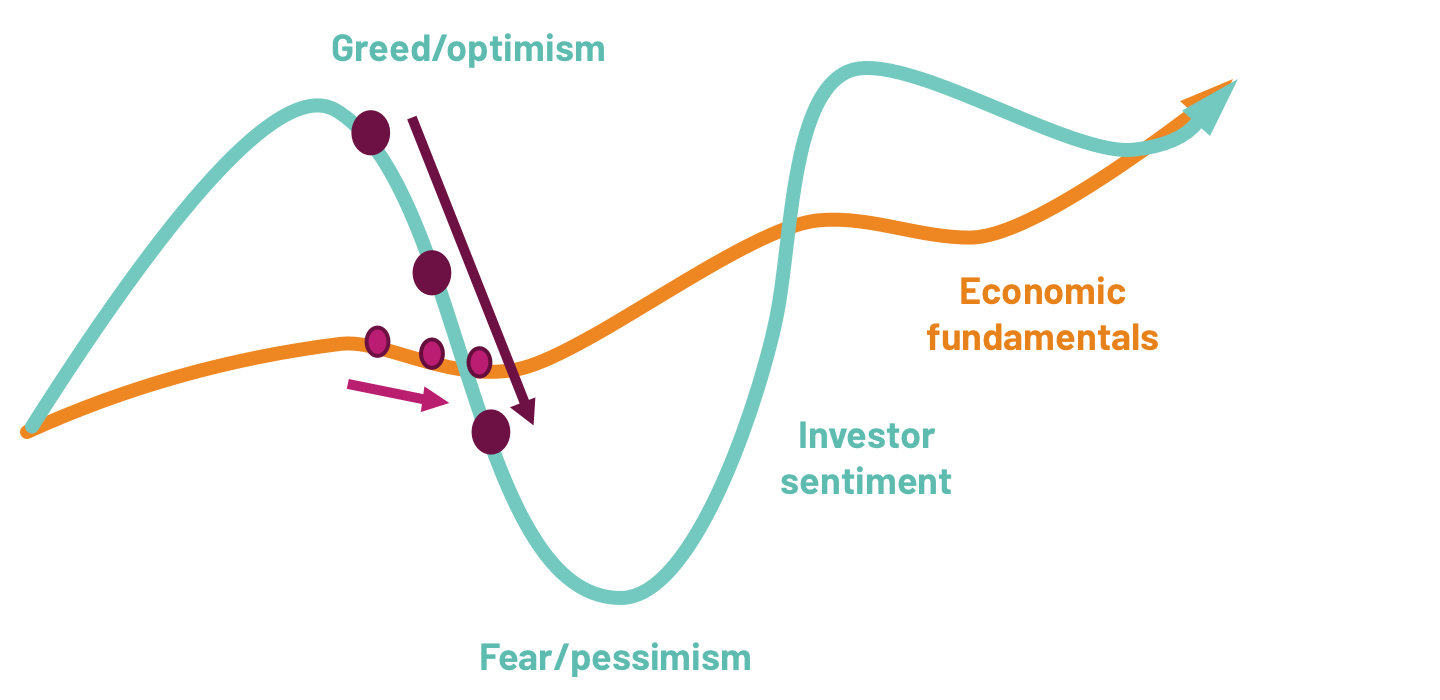

Over the next 12 months, we think that the global economy will slow down – prompting bouts of volatility. In this environment, it is important to rely on a stable identity. Economic uncertainty creates fear and investor sentiment tends to overreact to economic turning points. Going forward, we believe that:

- Inflation will come down. Goods inflation is slowly normalising, and supply chain pressures are going.

- Central banks are getting close to the end of their hiking cycles, but there is still a bit more work to do.

- A mild US recession is still likely. Most leading indicators point towards a recession, but the recession shouldn’t be too long or deep.

In such an environment, investors will start to worry about what’s next for financial markets. Economic data isn’t likely to stabilise until next year. Equity markets are unlikely to perform well in the medium term.

We know our investment identity helps us to deliver in just these kinds of environments. We have positions that can generate returns despite this volatile backdrop.

Investor sentiment overreacts to economic turning points …

… with slightly weaker data leading to panic right now

Source: 7IM

Asset allocation

Detailed asset allocation

| Cautious TAA | Moderately Cautious TAA | Balanced TAA | Moderately Adventurous TAA | Adventurous TAA | Income TAA | |

|---|---|---|---|---|---|---|

| UK Equities | 6.25% | 8.00% | 16.75% | 19.75% | 22.25% | 10.50% |

| US Equities | 3.50% | 6.00% | 10.75% | 11.50% | 11.75% | 8.00% |

| European Equities | 2.75% | 3.25% | 3.75% | 6.00% | 6.75% | 3.75% |

| Japan Equities | 2.25% | 3.25% | 4.50% | 7.00% | 8.75% | 2.50% |

| Emerging Markets Equities | 1.75% | 2.75% | 2.25% | 4.75% | 8.00% | 2.50% |

| Global Themes | 5.00% | 6.50% | 10.50% | 14.50% | 18.50% | 4.00% |

| Global Government Bonds | 26.00% | 13.00% | 8.50% | 0.00% | 0.00% | 13.00% |

| Gilts* | 11.00% | 3.00% | 2.50% | 0.00% | 0.00% | 6.00% |

| UK Corporate Bonds | 5.00% | 8.50% | 5.00% | 0.00% | 0.00% | 10.00% |

| Global Corporate Bonds** | 6.25% | 12.75% | 4.00% | 0.00% | 0.00% | 18.75% |

| Global High Yield Bonds | 3.50% | 3.50% | 4.50% | 5.00% | 5.00% | 6.00% |

| Emerging Markets Bonds | 3.00% | 6.00% | 6.00% | 5.00% | 0.00% | 11.00% |

| Global Inflation Linked Bonds | 6.00% | 3.00% | 0.00% | 0.00% | 0.00% | 0.00% |

| Real Assets*** | 0.75% | 4.00% | 3.25% | 2.75% | 4.50% | 4.75% |

| Alternatives/Hedge Funds | 20.50% | 17.50% | 15.00% | 14.50% | 12.00% | 0.00% |

| Cash | -3.50% | -1.00% | 2.75% | 9.25% | 2.50% | -0.75% |

Source: 7IM. *Includes Short Term Sterling Bonds **Includes Convertible Bonds ***Includes Infrastructure

You can download the commentary as a PDF here.