Monthly commentary

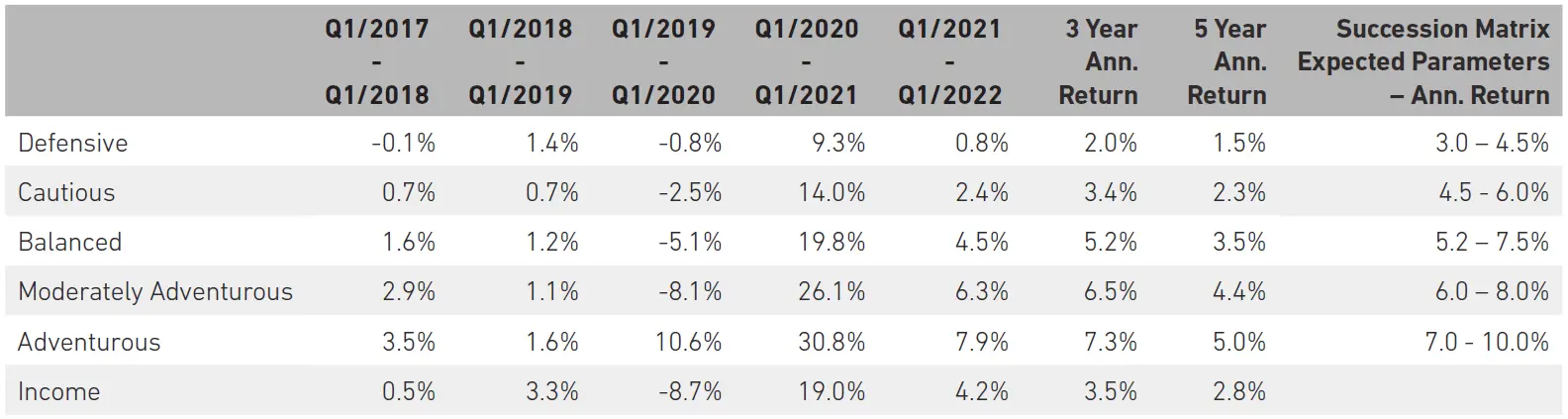

Portfolio Performance

At 7IM, we believe that taking a long-term view is essential when investing. We can’t always avoid the short-term bumps and shocks that the financial world has in store, but a well-diversified portfolio goes a long way towards smoothing out some of the journey. The long-term nature of our strategic and tactical process is a good complement to the Succession Matrix Expected Parameters.

Source: 7IM/FE. Annualised return is defined as ‘Ann. Return’ in the performance table above and is as at end May 2022. The extreme COVID-19 related drawdown at the start of 2020 means performance should continue be viewed with caution. Portfolios are towards the lower end of their ranges for the five-year returns, with the more defensive end struggling a little in the face of low interest rates.

Market and Portfolio Review

Global equity has been hit hard since the beginning of the year, but during May, the MSCI ACWI managed to stay flat to marginally up. Despite this slightly positive general direction, relative moves in markets which we have seen since the beginning of the year have persisted: growth stocks continued to underperform and lost a further 2.2% over the month, while value gained 2.2%; commodities rallied by 1.5% over the month, helping to prop up the UK markets, which are now up 1.5% over the year.

Unfortunately, this small move in a positive direction has not convinced investors that the bear market is over. Bloomberg data is suggesting that market commentators are losing interest in writing about ‘buy the dip’, but are gaining interest in writing about the ‘bear market rally’:

There could be a whole number of reasons for this, but the one at the front of people’s minds is still rates, as central banks remained hawkish:

The Bank of England raised rates to 1% in May, and with inflation at 9%, it seems unlikely they won’t raise them further in June. Lagarde also took to the ECB website to set out a new and more hawkish policy for European rates, committing to two interest rate hikes by September. This marks a pretty big move for Europe, as they are turning away from a decade of aggressively dovish policy and back towards positive rates. Lagarde noted that the “disinflationary dynamics of the past decade are unlikely to return”, and after inflation data came in higher than expected, it looks like commitment to European monetary tightening is here to stay.

Despite the Fed not changing targets, recent meetings and events look like a soft attempt at forward guidance – a policy tool whereby central banks simply communicate with the public to give signals of future policy to manage market expectations. Over the month, messaging from the Fed became less hawkish. At the beginning of the month, Powell stated that the Fed would not hold back in raising rates beyond neutral, even if it meant an increase in unemployment. As the month went on and poor growth became a more real threat, messaging became less clear.

This episode did introduce some volatility, but the market is pricing in 50 bps Fed hikes in June and July, so not much has actually changed.

Portfolio Positioning and Changes

During May, we rebalanced the Succession model portfolios and made the following changes:

We sold out of the part of our cyclical basket that was in global mid-caps. This is due to a deterioration of the outlook for mid-caps generally. Mid-cap indices tend to have significant overweights to Europe, and a lot of these stocks have been shown to be quite sensitive to events in Ukraine. We would prefer to minimise our risk to the Russia Ukraine conflict as second-guessing what will happen next is extremely difficult. The cash freed up by this decision was recycled into our SAA global equity allocation.

This quarter we have introduced the Fulcrum Diversified Core Absolute Return Fund to our alternatives basket. The fund is a combination of multiple alternative building blocks together in a single strategy. Together it is taking many of the individually attractive and available strategies from Fulcrum and combining them in to one. This includes strategies we own on a standalone basis elsewhere (dispersion) and strategies we have looked at individually as part of other searches (trend following).

Core views

At 7IM, we have a number of long-term core views that help to guide our investment decisions and allocations within portfolios.

We expect equity markets to go sideways… as the world normalises, manufacturing will slow, and services will recover. How deep will the slowdown be? How long will it last? Will services be able to take up the slack?

These questions will be on investors’ minds for a while. Without a clear direction for the economy, equity markets will struggle to move meaningfully higher as investors question both valuations and future earnings streams. Put selling and higher credit allocations should do well in this world.

Bond yields have more symmetry now… inflation is the other uncertainty hanging over investors. When will inflation come down? How low will it go? What will the Fed do next? This uncertainty has led to the volatility we have seen so far. The flip side of that volatility is that it doesn’t pay to be as underweight. Bond yields, at these levels, have more symmetry. Adding government and corporate bonds looks sensible.

Remain diversified… the lack of direction will have an impact across different markets. Will a particular factor (growth/value) work out? Should we favour defensives or cyclical stocks? Are there obvious sector winners? The market is not providing us with opportunities to pick a side right now. So, we remain diversified… properly diversified. Our portfolio of diversified holdings across asset classes, time horizons and alternatives should do well.

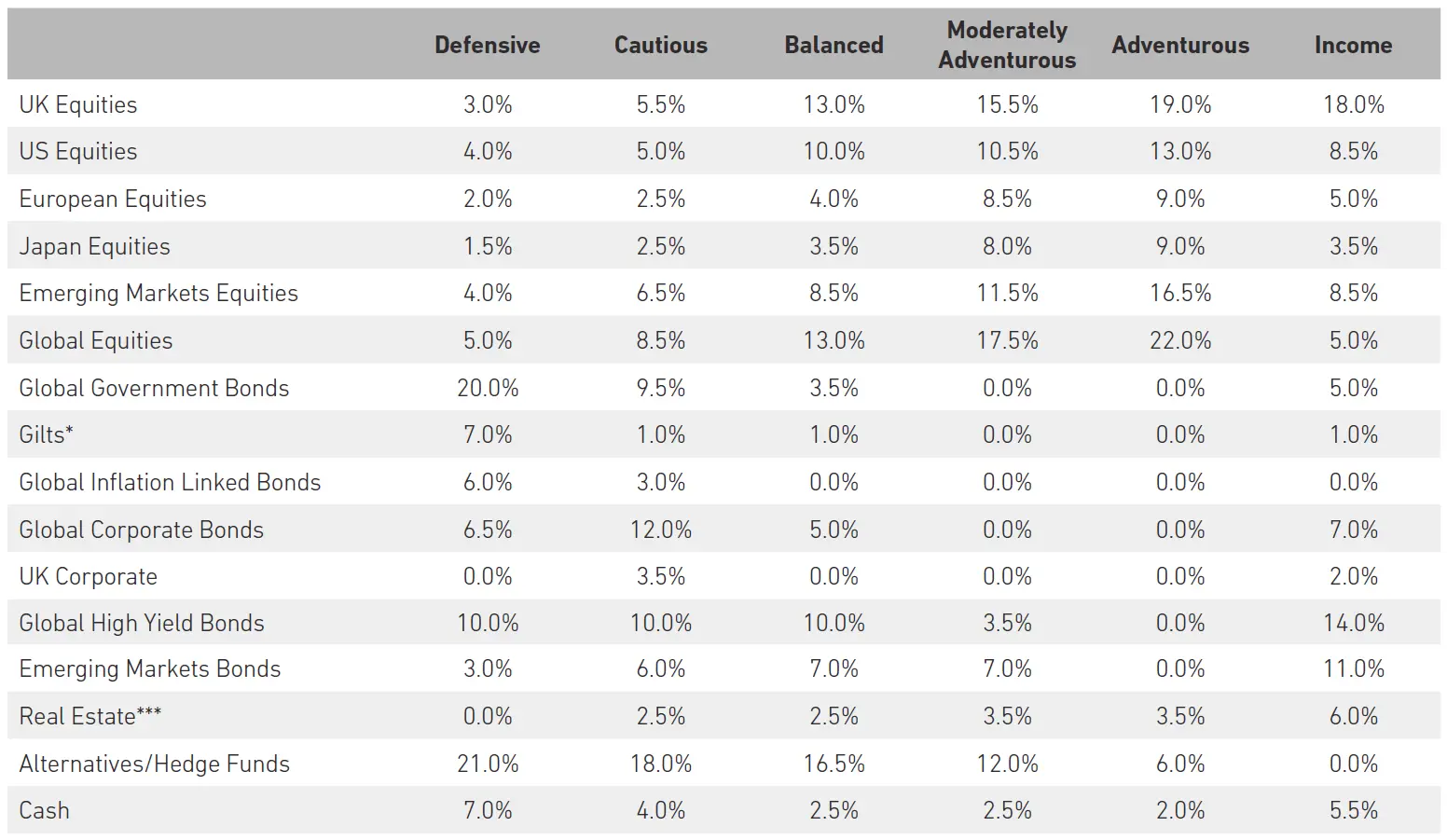

Detailed asset allocation

Source: 7IM. *Includes Short Term Sterling Bonds **Includes Convertible Bonds ***Includes Infrastructure

Read more from 7IM

You can download the commentary as a PDF here.