Quarterly Rebalance Commentary

Overview

The past three months have seen some interesting reversals in both bond and equity markets.

In May, global equity managed to avoid further losses from the start of the year, but the relative market moves continued – global growth continued to fall while value managed to stay above water.

June rounded off a torrid first half of the year for equities and bonds as investors continued to price in aggressive rate hikes. The simultaneous sell-off in both bonds and equities made it especially hard for multi-asset investors as there were very few places to hide.

July saw a dramatic reversal in markets. Equity markets bounced back very healthily, with growth stocks leading the way – this was largely driven by a change in sentiment around rates. Investors felt that rate hikes were overly priced in, and rate cuts began to get priced in.

Positive sentiment has carried through to August so far, with the S&P and FTSE continuing to rally.

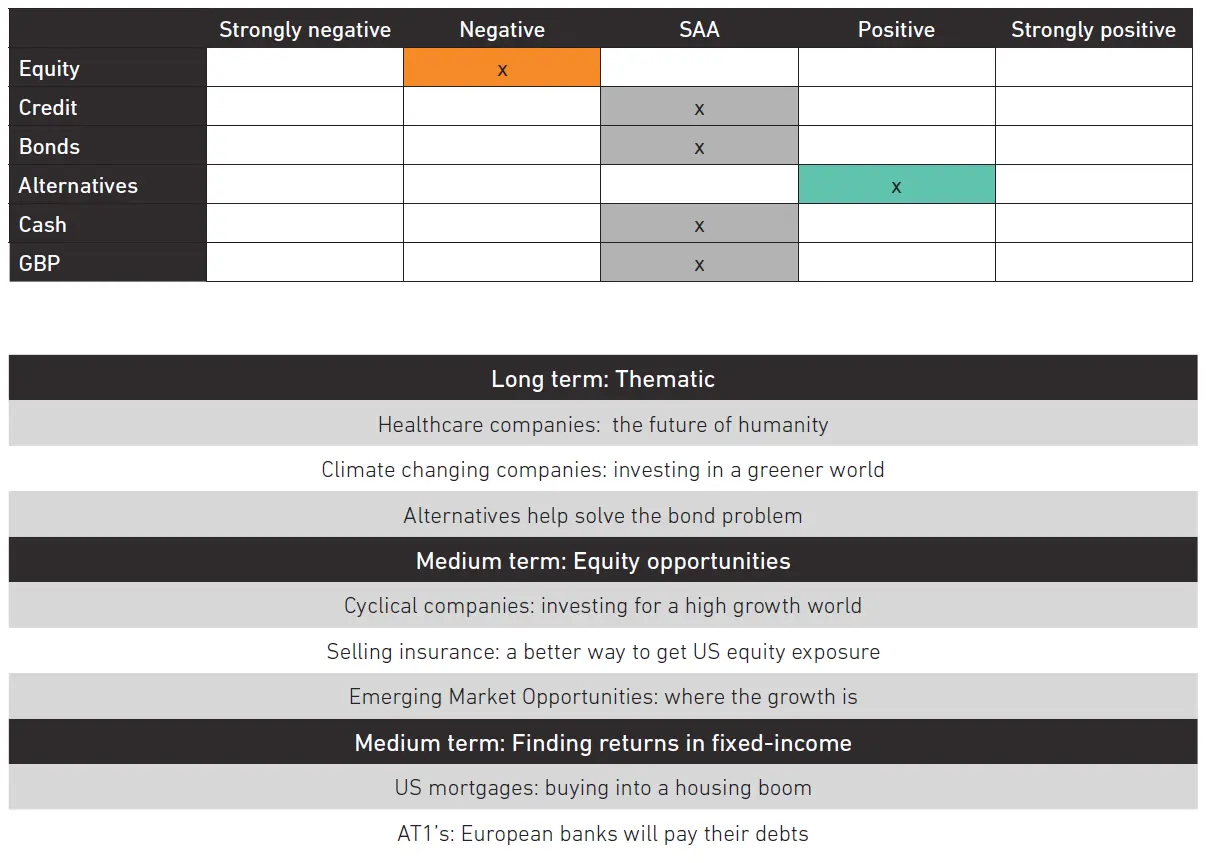

Core investment views

Economic uncertainty creates unstable markets

- A global manufacturing downturn is unavoidable… the service sector should be resilient, but the pain will be real

- Inflation will fall eventually… but the short-term outlook is going to make negative headlines

- Central bankers are under pressure… but they’re more scared of inflation than of recessions

- Corporate profit margins have peaked… most companies will keep growing earnings, but the easy wins are gone.

A recession can’t be ruled out… caution is advised

- The economic data isn’t likely to get better until we reach 2023. And lack of confidence is becoming widespread

- That means nervousness will continue to bleed from the financial markets to the real economy. Many people are still scarred by the financial crisis – and while most recessions are far less savage, it will still feel extremely uncomfortable for ordinary consumers and for unprepared investors.

7IM portfolios are diversified and robust to geopolitical shocks

- Diversified equities (not just US equity)

- Diversified non-equity risk (high yield/emerging market bonds vs. equities), credit positions protected from defaults (RMBS/AT1s)

- Diversified defensive assets (alternatives)

- Global healthcare tends to be defensive

- Climate change solutions are not linked to the economic cycle

- Selling market insurance during bouts of fear is profitable

- Underweight equity risk

Asset allocation changes

A lot has happened through 2022. A sharp rise in interest rates, inflation higher and stickier than expected, and the start of economic normalisation. Portfolios need to reflect this changing world. While interest rate uncertainty isn’t over, the chances of a sell-off in bonds like the one we saw in the first half of the year, has come down. As such, we moved our exposure to bonds much closer to a neutral position.

While we believe inflation is coming down, there is still a long way to go. This is making central bankers nervous and is precipitating a ‘cost-of-living crisis’ that is seeing real incomes squeezed and spending come down. Also, the boom in manufacturing is over (as we spend less on goods), this is going to weigh down on company earnings. Put together, we have taken down our equity risk compared to our long-run strategic benchmarks.

Finally, the world we see coming will be sideways and volatile for most risk assets. In a world where risk assets are going to struggle, and fear is elevated, it pays to sell the market insurance. So, we increase our exposure to the Put Selling Strategy (‘selling insurance: a better way to get US equity exposure’).

Manager Changes

This quarter, we have introduced the Schroder Prime UK Equity Fund into our active model portfolios. This proven strategy aims to add value through solid stock selection rather than large sector or factor bets. It is typically more focussed on larger companies than many of its peers in the UK sector, something we favour right now. This addition further diversifies our UK equity line up and slightly reduces the overall cost of the portfolio.

We have also introduced the iShares US Treasury 20+ year bond ETF across our blended and active model portfolios. This is a cheap and effective way to manage the bond exposure in portfolios, allowing us to increase duration with a relatively small holding.

In our Passive mandates, we also added the iShares Emerging Markets Hard Currency Debt GBP Hedged Fund, allowing us to shave a bit more of the overall cost out of portfolios while keeping our FX exposures aligned with targets.

Please note: All of the comments in this document refer to the models we run on the 7IM platform, but the models are also available on a range of other platforms. As much as possible, we try to replicate the models we run of the 7IM platform across all platforms, but due to differing security availability, not all of the points outlined in this document may be relevant across these platforms. If you are unsure whether certain changes apply to models on a specific platform, please reach out to a member of the team.

Read more from 7IM

You can download the commentary as a PDF here.