Quarterly Rebalance Commentary

Overview

Our view of the world hasn’t changed much this quarter. Despite the emergence of new variants, the world is slowly but surely learning how to deal with COVID. The stability of our views over the quarter reflects that we run money as long-term investors. We don’t flail around, changing our view every time the market moves. Instead, we carefully consider the factors and information most relevant to us and refresh our views accordingly. As we said last quarter, we’re looking past the recovery phase, and instead positioning ourselves for the post-pandemic growth boom.

Core investment views

A new wave of economic growth… For the past decade or so, the virtuous circle of consumption and investment has just not been able to get going. The scars of the financial crisis were too deep – people bought less stuff while governments reined in spending. As a result, companies kept putting off investing in longer-term projects.

The 2020 recession hit the reset button. People are willing to spend again, while governments have ditched austerity. Policymakers around the world have made it clear that they’ll stay supportive for a long, long time. And so, companies are starting to invest for the future. We are now at the start of a sustained period of growth, fuelled by confidence and expansion across all sectors of the global economy.

And a little inflation won’t hurt… Economists tend to dislike thinking about the psychology of inflation, but in a lot of ways, someone’s inflation expectations are a good proxy for their confidence levels. With the right amount of price and wage growth, people are encouraged to make life decisions which are positive for the economy. We haven’t heard the word “Goldilocks” for some years now, but there really is an amount of inflation which is just right to keep things humming.

7IM portfolios are positioned for a changing environment… For this coming growth phase, we believe a more selective exposure will be better than a large overweight to the broad equity market. A more robust consumer-driven cycle will see different winners emerge. Regions and industries which have struggled to attract investors over the past decade are better positioned to capitalise than the huge US tech giants (although there are lots of small US companies which will do well).

We’ve also made sure that our fixed income positioning isn’t unnecessarily exposed to rate rises, using allocations to alternatives and to non-mainstream asset classes.

| TAA themes | Implementation |

|---|---|

| The world is getting older | Healthcare companies |

| Bond safety comes at a price | Alternatives |

| Go to Asia for yield | Asia high yield |

| A US housing boom is underway | US mortgages |

| European Banks aren’t scary | European alternative tier 1s |

| The COVID-19 recovery has kickstarted a new economic cycle | Growth+ basket |

| Selling equity market insurance after a disaster | US equity volatility carry |

| Investing in a cleaner future | Climate change solutions |

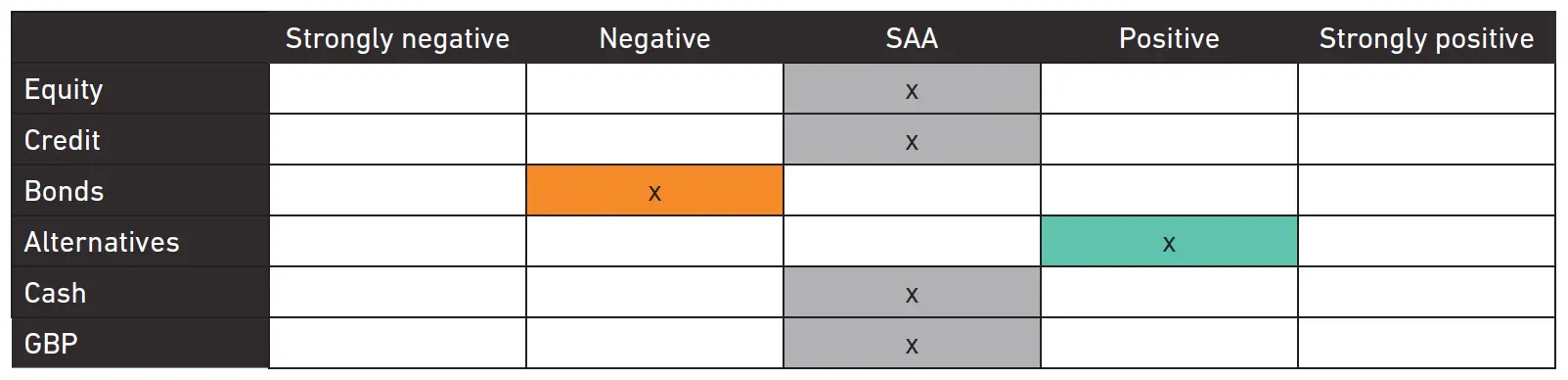

Asset allocation changes

Since we went overweight equities in the models in August 2020, equity markets are up just under 40%1. Which is why, in this quarter, we have decided to take our profits from our overweight equity position and return to neutral, resulting in slightly higher cash and alternatives allocations. As our core views suggest, we still believe that the world is well placed for strong economic growth, but this is now being priced in more than it was previously, as the strong bull market suggests.

We have also introduced our Asia High Yield position into the adventurous risk profile models by recycling some of our overweight equity profits into the asset class. Our conviction in the asset class is strong, and given the recent issues in the Chinese property sector, we now believe that Asia High Yield is offering returns attractive for an adventurous risk profile.

Manager updates

No completely new holdings have entered our models in this rebalance. We are always looking to optimise portfolios but remain very happy with how our existing mangers are performing, so there has been no need to bring in any new holdings this quarter.

1 “Equity markets” as measured by MSCI world (source BBG).

Please note: All of the comments in this document refer to the models we run on the 7IM platform, but the models are also available on a range of other platforms. As much as possible, we try to replicate the models we run of the 7IM platform across all platforms, but due to differing security availability, not all of the points outlined in this document may be relevant across these platforms. If you are unsure whether certain changes apply to models on a specific platform, please reach out to a member of the team.

The past performance of investments is not a guide to future performance. The value of investments can go down as well as up and you may get back less than you originally invested. Any reference to specific investments are included for information purposes only and are not intended to provide stock recommendation or investment recommendations to individual investors.

Read more from 7IM