Monthly commentary

Summary

After a strong rally for global equities this year, the financial markets faced the first monthly decline in US equities since February. The S&P 500 lost 1.6%, while the technology-heavy Nasdaq lost 2.1% over the month of August.

As we mentioned last month, the S&P 500 has relied heavily on the ‘Magnificent Seven’ (Meta, Microsoft, Alphabet, Apple, Amazon, Tesla and Nvidia) this year. However, it has been Nvidia who has grabbed the headlines and been the main driver of the seven’s performance.

While it used to be a gaming company, now it is all about data centres. The AI revolution boosted the demand for data centres as everyone raced to build their own ChatGPT rivals. Hopes for the company’s quarterly results were high, but Nvidia’s whopping US$13.5bn in revenue surpassed analysts’ wildest expectations by US$2bn.

The concept of AI has been around for decades now, from AI vs humanity in the Terminator franchise, to creepy AI realities in the Netflix series Black Mirror. But now it has invaded real life.

So, are we in an AI stock bubble? Investopedia summarises the five stages of a stock bubble as follows, and we can see whether AI fits into this:

- Displacement occurs when investors get enamored with a new paradigm – √

- Price rises slowly at first, then gains momentum –√

- Euphoria in markets as prices skyrocket and valuations reach extreme levels – √

- Profit taking when warning signs show the bubble is about to burst – X

- The bubble is pricked and bursts – X

It is looking increasingly likely that we are in an AI-related bubble. We’ve had bubbles before, and we know that they correct in due course – often violently.

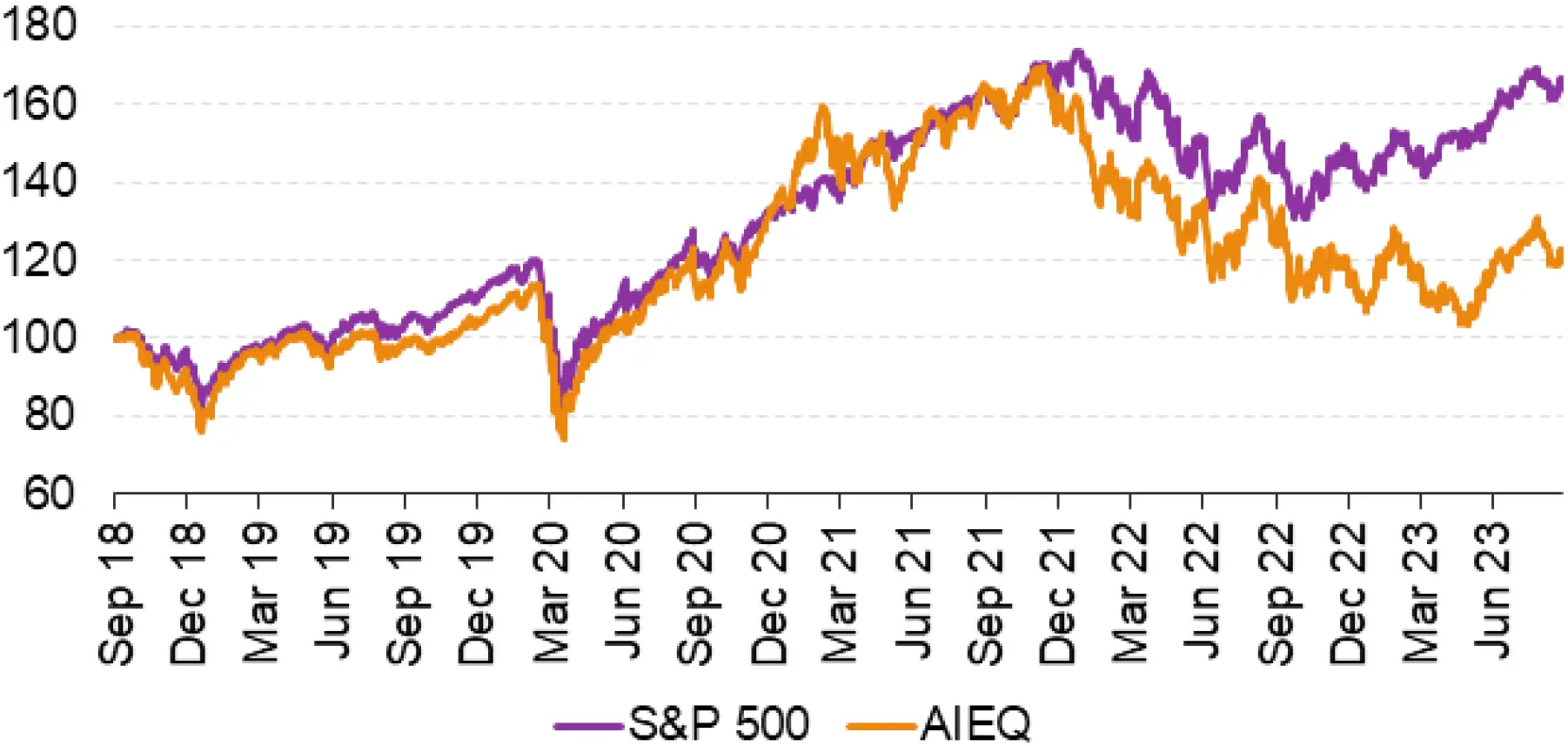

Ironically, in the midst of all this AI hype, it looks like AI-powered ETFs are not keeping up with the AI computing boom!

Source: Bloomberg Fincance L.P.

This just shows AI can’t replace everything, human intervention and expertise is still vital in the world of investing.

Taking a deeper look at why we had a dip in the equity markets this month:

- US Treasury Yields increased given better-than-expected economic data, dragging down US stocks. The Fed has reaffirmed that they are determined to get inflation back to 2%, meaning the interest rate could stay higher for longer. US credit was also downgraded by Fitch earlier in the month due to “a high and growing general government debt burden, and the erosion of governance”1, although this had a limited impact on yields

- Closer to home, we also saw a decline in FTSE 100 and Eurostoxx 50, returning -2.6% and -3.8%, respectively, as the inflation and interest rate story continues

- China also played a part in August’s loss. Beijing has put in measures, such as lowering the interest rate, to boost sluggish growth, but fears of economic slowdown and property crisis persist. Economic data came in weaker than expected, with youth unemployment at record highs.

Actions taken

During August, we did not make any major changes to portfolios.

Core investment views

At 7IM, we have a number of long-term core views that help to guide our investment decisions and allocations within portfolios.

Over the next 12 months, we think that the global economy will slow down – prompting bouts of volatility. In this environment, it is important to rely on a stable identity. Economic uncertainty creates fear and investor sentiment tends to overreact to economic turning points. Going forward, we believe that:

- Inflation is coming down: Across the developed world, inflation has peaked, and is mostly falling. Supply-chain disruptions have eased, energy prices are a little more settled, and companies are no longer reporting issues with finding workers. Of course, slower inflation still means rising prices – so the cost of living pain isn’t going away quickly

- Interest rates are high: We’re now over a year into the rate hiking cycle. Interest rates are unambiguously high when compared with the past decade. The impact of higher rates is always the same – although time-to-effect changes in every cycle

- The economy is slowing: For consumers and companies, day-to-day life is getting harder – whether it’s rising costs or increased debt, there’s less money left at the end of the week or month. As the flow of money around the economy slows, strong growth is more difficult to achieve. The world may or may not slip into a ‘technical’ recession in the next three months, but a sluggish growth environment is already here.

Sluggish and sideways… In an environment with lots of uncertainty and a lack of confidence, we want to make sure portfolios are insulated against shocks, while still generating sufficient returns to make investing worthwhile. And we think our portfolios are set up to do just that.

There’s no one answer… When managing a diversified long-term portfolio, there shouldn’t be a single ‘big’ call. For an outlook that calls for selectivity, especially in the medium and short term, we’re finding lots of different opportunities – both to protect capital and to grow it.

You can download the commentary as a PDF here.

I confirm that I am a Financial Adviser, Solicitor or Accountant and authorised to conduct investment business.

If you do not meet this criteria then you must leave the website or select an appropriate audience.