Monthly commentary

Monthly musings: The mouldy side of volatilité

In Europe, when many families gather round to celebrate Christmas, there’s a chance there will be a cheese or two of some description at the table, and perhaps a liver pâté that compliments all those elements that make up that carefully curated cheese board.

Then, a few days later, some will celebrate the start to the new year by opening a bottle of sparkling wine of some description.

There’s a lot to thank France for in December – and not only at the dinner table, but also for producing luxury goods (like Louis Vuitton or Cartier) for those generously looking to thank (or apologise to) someone special.

But as an economy in 2024, France needed a bit more than camembert, foie gras or champagne for a boost. It needed a Christmas miracle that is yet to happen.

There are several reasons why France struggled towards the end of 2024. The first reason (and the main source of trouble) is the rising political volatility in the country, peaking in December after the resignation of Michel Barnier, France’s third prime minister in 2024.

Four prime ministers in, Moody’s downgraded the country’s credit rating on the grounds of “political fragmentation” and “a very low probability” of reducing the fiscal deficit.

Looking at other parts of the world, it’s easy to see that bad politics rarely affects the financial markets. But really bad politics (remember Liz Truss?) does move markets.

Sadly, France is on the really bad boat. The CAC 40, France’s benchmark equity index, fell 3% on the year. For reference, European index Stoxx Europe 600 went up 7%.

Unfortunately, that’s not the only source of struggle. Because China has been a little bit busy recently dealing with its slow growth issues, lacklustre demand for those luxury goods hasn’t favoured the French names.

After all this, investors are looking at France carefully before investing their money there. If history is any indication, that can only go away when France is in a position to tell investors a story of stabilité.

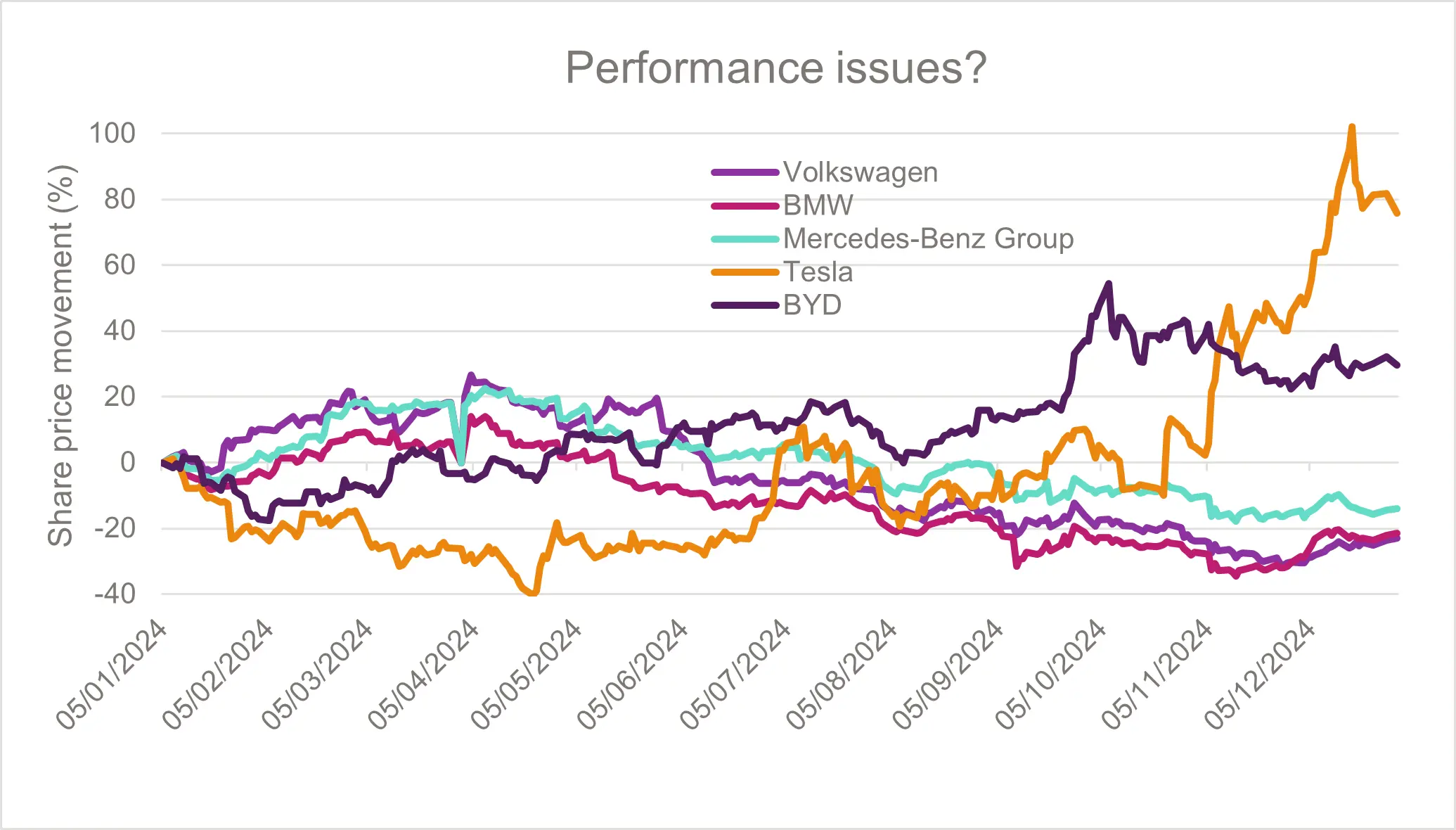

Chart of the month

While most car manufacturers are trying to switch gears towards more innovative solutions, some companies are doing better than others.

And 2024 was not a great year for German carmakers. To be fair, recent years haven’t been great for them.

Back in the ‘80s, when excellence on the road belonged to Germany, and expansion plans outside of its local market meant new partnerships outside of the country. Branching out to other countries, though, meant sharing their secrets.

And that’s how China began learning from the best. Fast-forward to the 2020s and you see brands like Nio, Xiaomi and BYD with improved models, crushing their German counterparts.

Source: Factset. Data as at 3 January, 2025

That’s what the chart above says. Volkswagen, BMW and Mercedes all saw their share price perform negatively in 2024.

In contrast, BYD’s share price went up more than 20%. Of course, Tesla played in a league of its own (a league of seven).

European carmakers need to find solutions to remain competitive. Fast.

December Markets Wrap

Some stubborn inflationary pressures, coupled with high wage growth, led the Bank of England (BoE) to keep rates on hold in the Monetary Policy Committee’s last meeting of 2024.

Looking at the patterns of the last year, the decision to hold was consistent. The rationale for the BoE has always been to act with caution and only cut rates in the absence of most negative signals.

The situation contrasts slightly with that of the US. The Federal Reserve cut rates by 25 basis points to 4.5%, in a sign of confidence in the cooling of inflationary pressures.

For markets, December was as eventful a month as every other December. It’s usually a time, however, where people look at how the year has fared.

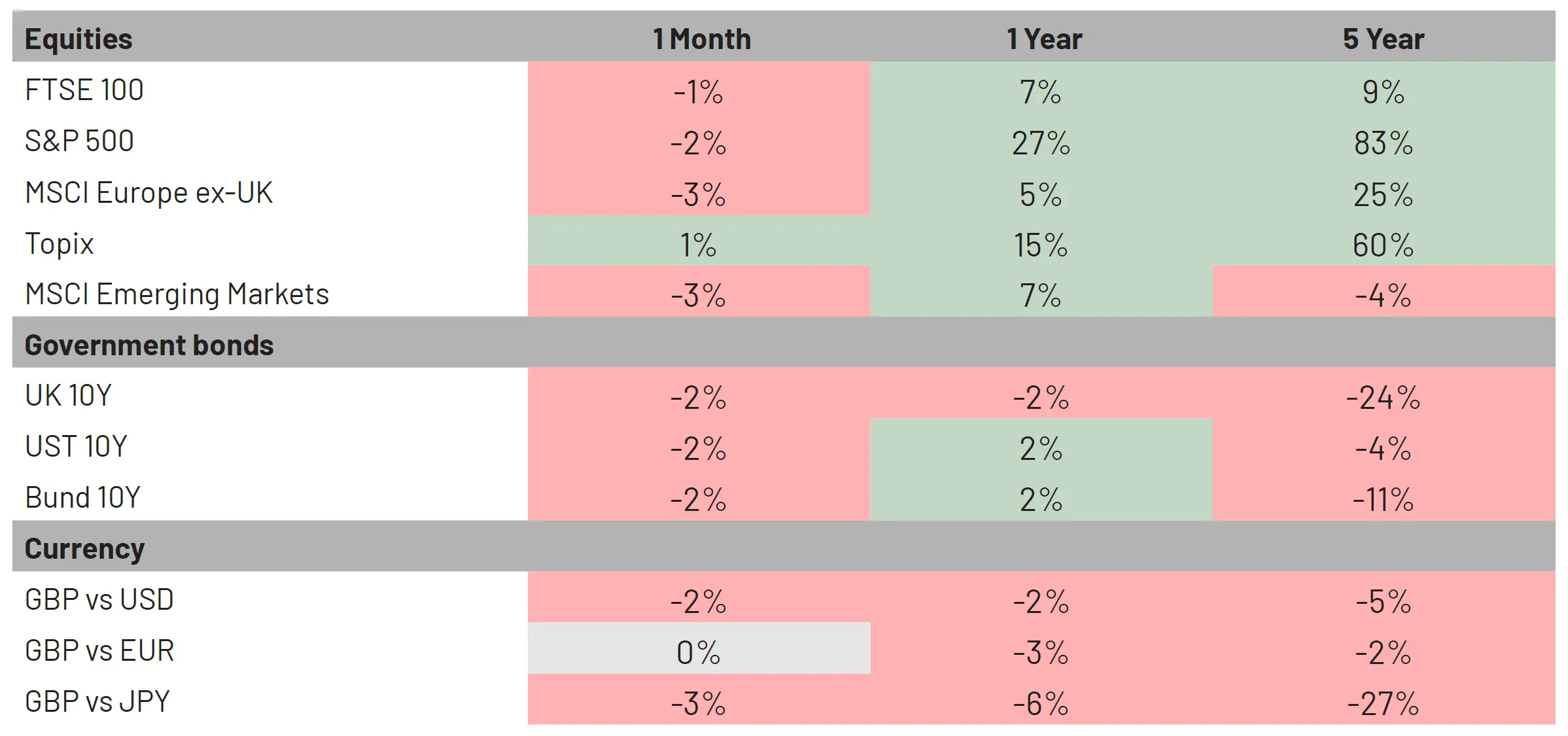

The S&P 500 gained 27% over the year, while the FTSE 100 and the Stoxx Europe 600 delivered a 7% growth.

Market Moves

Source: Bloomberg Finance L.P. Data as of 6 January 2025

What we’re watching in January:

- 15 January: UK and US inflation figures for December

- 20 January: Trump inauguration

- 29 January: Fed interest rate decision

More from 7IM

You can download the commentary as a PDF here.

I confirm that I am a Financial Adviser, Solicitor or Accountant and authorised to conduct investment business.

If you do not meet this criteria then you must leave the website or select an appropriate audience.