Monthly commentary

Monthly musings: Trump, tariffs and tech

January’s done, there’s a new President in town, and other than some provocative gestures from Elon Musk, the inauguration passed off relatively seamlessly. As far as Trump seems to be concerned, that was the starting pistol on his last four years in charge, and he’s gonna make ’em count.

As we expected, he’s started with a lot of fire and fury on tariffs, immigration and defence spending. The consensus is that this is simply a starting point for negotiation – but it’s definitely worth considering that some of his policies might cause real economic damage, both in the US and around the world.

For example, if the tariffs on China, Canada and Mexico continue at Trump’s proposed rates (10%, 25% and 25% respectively) over the next year, there could be half a percent wiped off US growth, and an extra percent on US inflation. Now, the thing with “growth that doesn’t happen” is that people find it hard to get upset about. But price rises? That does hurt. The question for the next twelve months is whether it will hurt enough for Trump to change his mind – it won’t be the data; it will be the people complaining (probably on X).

Speaking of complaining, it’s been extremely interesting to hear the whining from the US AI companies about China stealing data – and the backlash from creative industries, journalists and academics around the world suggesting that this “theft” is no different from what AI tools are doing to them!

I have to say, if I were a Chinese artificial intelligence program, I’d be feeling a little uncomfortable somewhere in my circuitry. Stealing some of the limelight from Donald Trump in his first month in power? Annoying the CEOs of the world’s biggest companies by popping the tech stock bubble (see below)? Not something you’d ordinarily recommend…

Our view (which we’ve said elsewhere too), is that it’s never clear what is going to dislodge the current market darlings. It could be an upstart competitor (like DeepSeek). It could be competition with another giant for the same slice of pie. It could be regulation from governments. It could just be that there’s no growth left (“younger generations don’t use Facebook”). But something will happen.

When the dot-com bubble burst in 2000, there was much wringing of hands. But out of the chaos came many of the companies which define the world today. The same will happen again. We’re just a little too close to the action to see the bigger picture.

And while the disruption is going on, it might be worth having a few investments in industries where AI isn’t the be all and end all; whether that’s housebuilders, or banks, or supermarkets. They aren’t exciting, but that doesn’t mean they’re bad investments!

Chart of the month

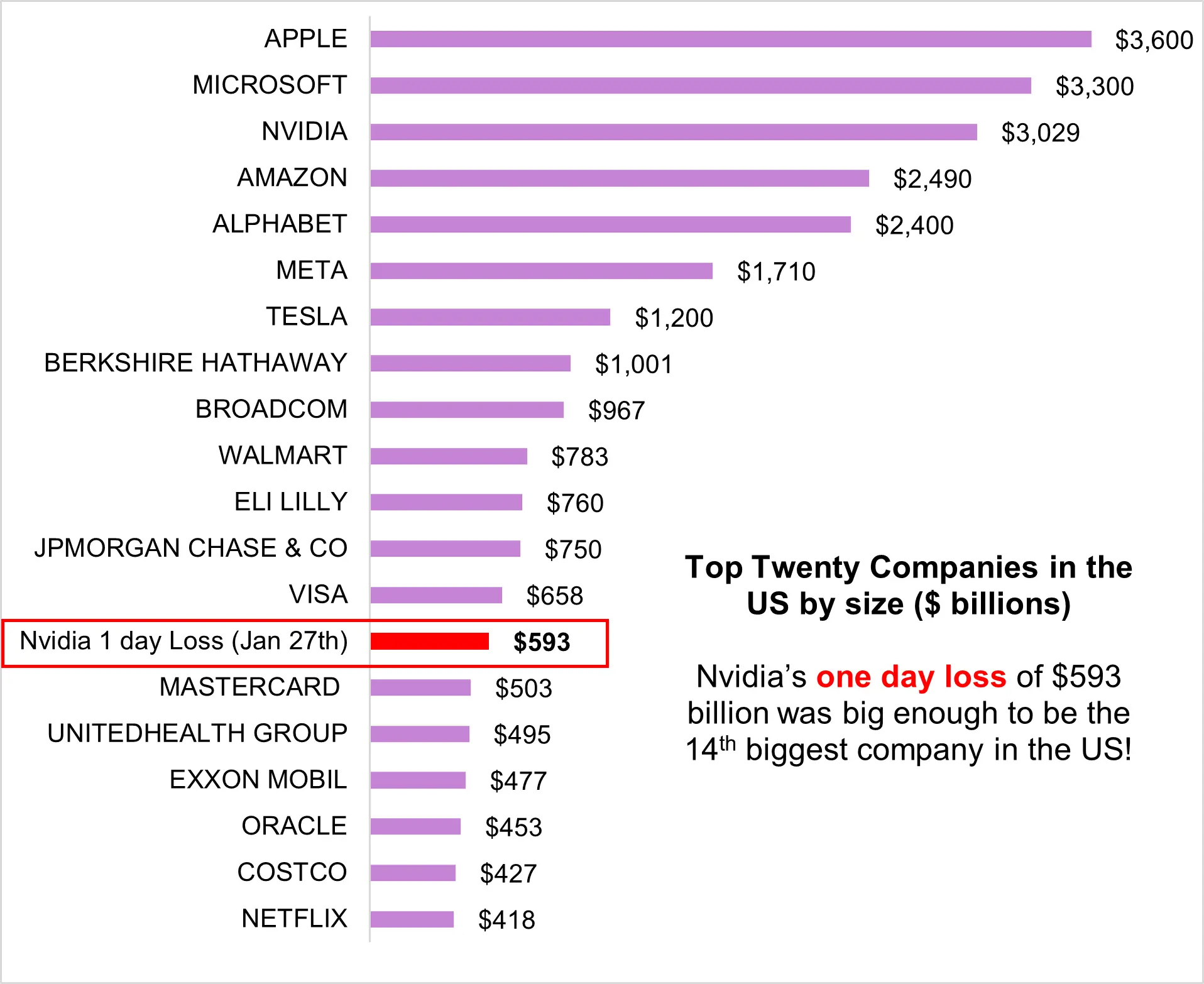

You never know exactly when a market becomes too top heavy. Big companies can stay big for a long time. But there’s certainly a few warning lights flashing when the daily moves of the biggest company are bigger than most of the rest of the market!

Nvidia lost $593 billion in value on the back of DeepSeek’s fast and frugal AI announcement – enough to wipe out ExxonMobil or Netflix in one go. Nvidia isn’t a bad business. It’s not going away. But as investors weigh up its valuation, the US market is likely to be very volatile and susceptible to shocks.

Source: Factset. Data as at 3 February

January Markets Wrap

Markets rode the January blues as if it were surfing a wave, with plenty of ups and downs to contend with, but finishing on a high across most markets and asset classes.

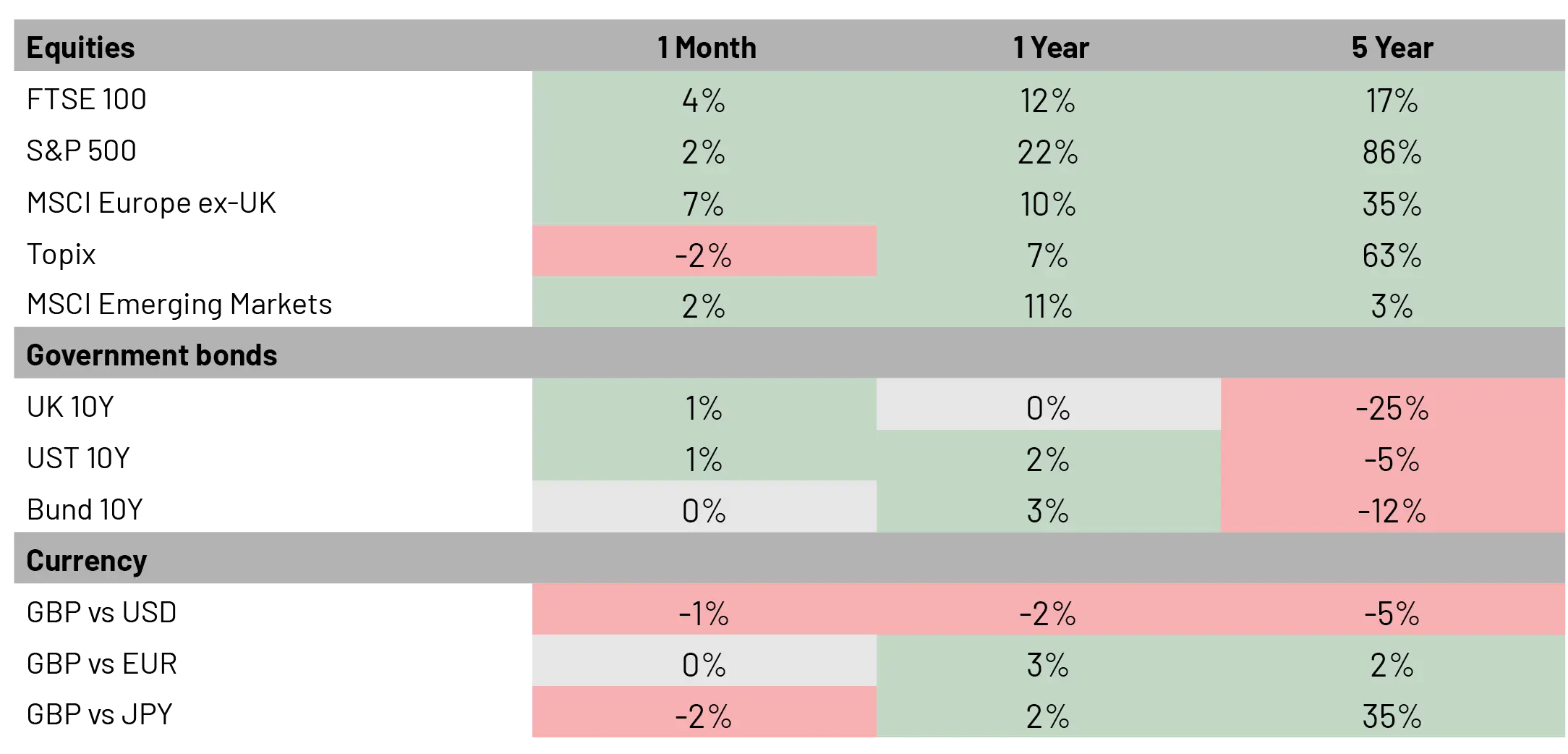

Weakness in AI names such as Nvidia and Broadcom dragged on Nasdaq returns, with the technology focussed index returning 1.6%, lower than the index’s bigger, broader brother, the S&P500, which returned 2.7%.

Closer to home, the FTSE 100 performed strongly, reaching another record of 8673.96 (+4.2%) as investors looked to diversify away from technology and into the more defensive characteristics posed by the FTSE 100.

All eyes will be focussed on the upcoming Bank of England meeting. Central banks remained cautious in their tone during January, likely due to the pending tariff policies set to be employed by President Trump, with the Fed holding rates in their recent meeting. Fixed income traders as a result pushed out their rate expectations to the second half of 2025, awaiting the potential inflationary impact of President Trump’s global restrictions.

Market Moves

Source: Bloomberg Finance L.P. Data as of 3 February 2024. Past performance is not a guide to future returns.

What we’re watching in February:

- 6 February: BoE Official Rate announcement

- 19 February: UK inflation data

- 24 February: Nvidia Earnings Call (are the other big tech companies getting fed up with paying the “Nvidia tax” – having to fork out billions for chips? Have they now got some viable alternatives?

- 26 February: Berkshire Hathaway Earnings Call (lots of non-tech businesses as part of Warren’s empire, so a good barometer for the health of the US economy)

More from 7IM

You can download the commentary as a PDF here.

I confirm that I am a Financial Adviser, Solicitor or Accountant and authorised to conduct investment business.

If you do not meet this criteria then you must leave the website or select an appropriate audience.