Monthly commentary

Summary

July has been a pretty busy month. The world experienced the hottest month on record, Alcaraz won his first Wimbledon title, ‘Barbenheimer’’ box office sales soared, Twitter lost its wings, and back at home, we have seen a ‘Farage vs. Banks’ battle brewing.

The financial markets have also been dealing with lots of events this month, so let’s take a closer look:

- Sticking to the inflation fight… In line with market expectations, central banks continued their fights against rising inflation. Across the pond, the Fed hiked rates by 25bps to a 22-year high after a “break” in June. In the Eurozone, the ECB is determined to return inflation to its 2% medium-term target, also raising rates as a result. The Bank of Japan also joined the tightening wave after decades of monetary stimulus, which surprised the market a little, sending Japanese yields to a nine-year high.

- In the midst of rate hikes, global equity markets have been buoyant:

| Index | July performance |

|---|---|

| S&P 500 | 3.2% |

| Nasdaq | 3.8% |

| FTSE 100 | 2.4% |

| Eurostoxx 50 | 1.8% |

| TOPIX | 1.5% |

With everyone piling into stocks, the S&P 500 and Nasdaq continue to lead the party. The long streak of monthly gains shows the market remains bullish following stronger-than-expected growth data, corporate earnings, and cooling inflation. The AI mania remains a driver of performance of US stocks. As the Q2 earnings start to come out in August, the mega-cap Magnificent Seven will have to show they’re worth the hype.

- Positive economic rumbles in Beijing… China signalled more support for the real estate sector, which has been in a multi-year growth drag, and to boost domestic consumption. Hope is running high, as Chinese equities had their largest rally since January and the gains continue into August.

Actions taken

During July, we have:

Replaced our holding in Berkshire Hathaway with US Equal Weight Index. We no longer have as strong a conviction in Berkshire due to the changes in the macro backdrop since its addition and the significant weight of mega-cap technology stocks (Apple), which could turn into a significant negative contributor against our recessionary base case outlook. We have made significant profits on Berkshire since the purchase in mid-2020 – outperforming the S&P 500 by 30%. We have shifted into a more diversified approach to US Equity, which still dilutes the mega-cap tech names.

Core investment views

At 7IM, we have a number of long-term core views that help to guide our investment decisions and allocations within portfolios.

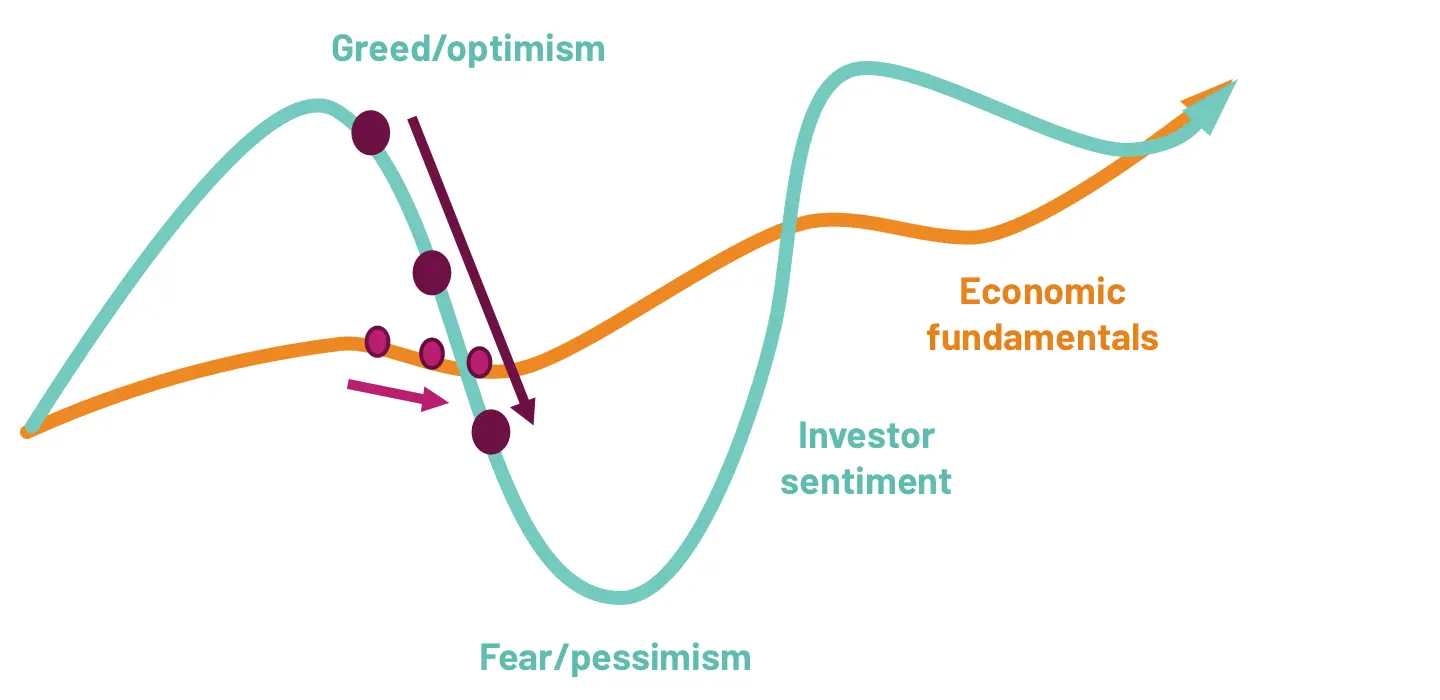

Over the next 12 months, we think that the global economy will slow down – prompting bouts of volatility. In this environment, it is important to rely on a stable identity. Economic uncertainty creates fear and investor sentiment tends to overreact to economic turning points. Going forward, we believe that:

- Inflation will come down. Goods inflation is slowly normalising, and supply chain pressures are going.

- Central banks are getting close to the end of their hiking cycles, but there is still a bit more work to do.

- A mild US recession is still likely. Most leading indicators point towards a recession, but the recession shouldn’t be too long or deep.

In such an environment, investors will start to worry about what’s next for financial markets. Economic data isn’t likely to stabilise until next year. Equity markets are unlikely to perform well in the medium term.

We know our investment identity helps us to deliver in just these kinds of environments. We have positions that can generate returns despite this volatile backdrop.

Investor sentiment overreacts to economic turning points …

… with slightly weaker data leading to panic right now

Source: 7IM

You can download the commentary as a PDF here.

I confirm that I am a Financial Adviser, Solicitor or Accountant and authorised to conduct investment business.

If you do not meet this criteria then you must leave the website or select an appropriate audience.