Monthly commentary

Monthly musings: The dangers of crowdsourcing

Fancy a festive trip – a quick city break with a Christmas market? Fair enough; about 4 million Brits go abroad in December. But how do you find out the best places to eat and drink? Well increasingly, people get on Instagram and TikTok to search for the best spots.

But be warned. Just because something has traction online, doesn’t mean it’s true! You’ve probably seen the news reports over the last month, with tales of American tourists being lured to Angus Steakhouses with fake reviews.

Now obviously, as a Brit, there’s something quite funny about the idea of a load of Midwestern visitors queuing up to eat at somewhere The Standard described recently as “sad steaks seasoned with despair”.

But there’s also a genuine point that popularity isn’t always a guarantee of quality. If you’re only in town for a couple of nights, you can’t waste a meal, so it’s important to check your sources and do your due diligence.

If your mum or best mate has said that Angus does good steak, that should mean more than a random collection of online suggestions... your relatives are more likely to know you and your preferences and less likely to want to see you miserable.

Doing something just because you think everyone else is... sounds familiar.

As we approach the end of the year, the popularity of the big US technology stocks has been significantly higher than any stocks or asset classes. Whether that’s the weight in the index, or the relentless media coverage, everyone is interested.

And while some of that hype is justified, there are plenty of other ‘restaurants’ to explore in the UK. Looking off the beaten track, whether that’s for new flavours or revisiting some classics, can pay dividends (literally in some cases).

The UK stock market has shown elements of both this year – the FTSE 100 might not have grown at the same pace as the S&P 500 (where growth in this index was mostly concentrated on the Magnificent 7) – but there’ve been some investment delights if you’ve been brave enough to look.

A few old favourites like NatWest, Barclays and Rolls Royce have still delivered the goods; they’ve all grown by more than any Mag Seven stock except Tesla. And a couple of lesser-known names, such as Bakkavor and Hochschild Mining have done the same.

So now, the tourists are coming. This month, we saw Canada’s ABC Technologies make an offer to buy FTSE 250’s TI Fluid Systems and Australian company Macquarie also approached UK waste management group Renewi.

The signs are there – UK stocks are undervalued. Serious investors know where the real hidden gems are, and that isn’t usually on TikTok.

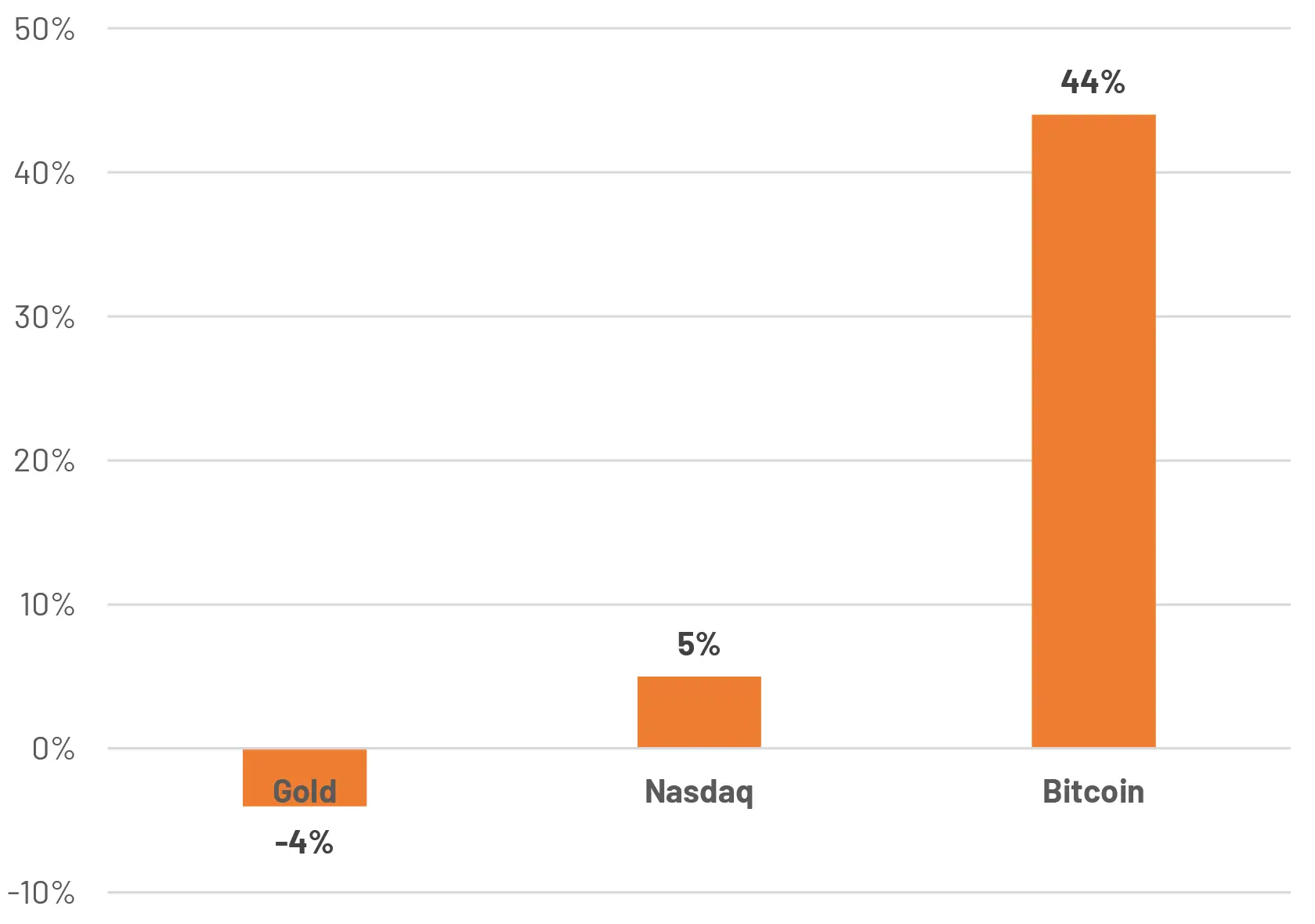

Chart of the month

It’s been a good year for gold, up nearly 30%.

However, since Donald Trump’s election victory, the shine has come off. While stock markets rejoiced, with bitcoin and US currency joining the same party, there has been no Midas touch for the precious metal.

As ever, it’s tough to know exactly what’s going on behind the price movements, but some combination of higher tariffs, slower rate cuts and the possibility of a resolution in Ukraine seem to be making things a little tougher as we approach the end of the year.

Source: Bloomberg Finance L.P. Data as of 2 December 2024.

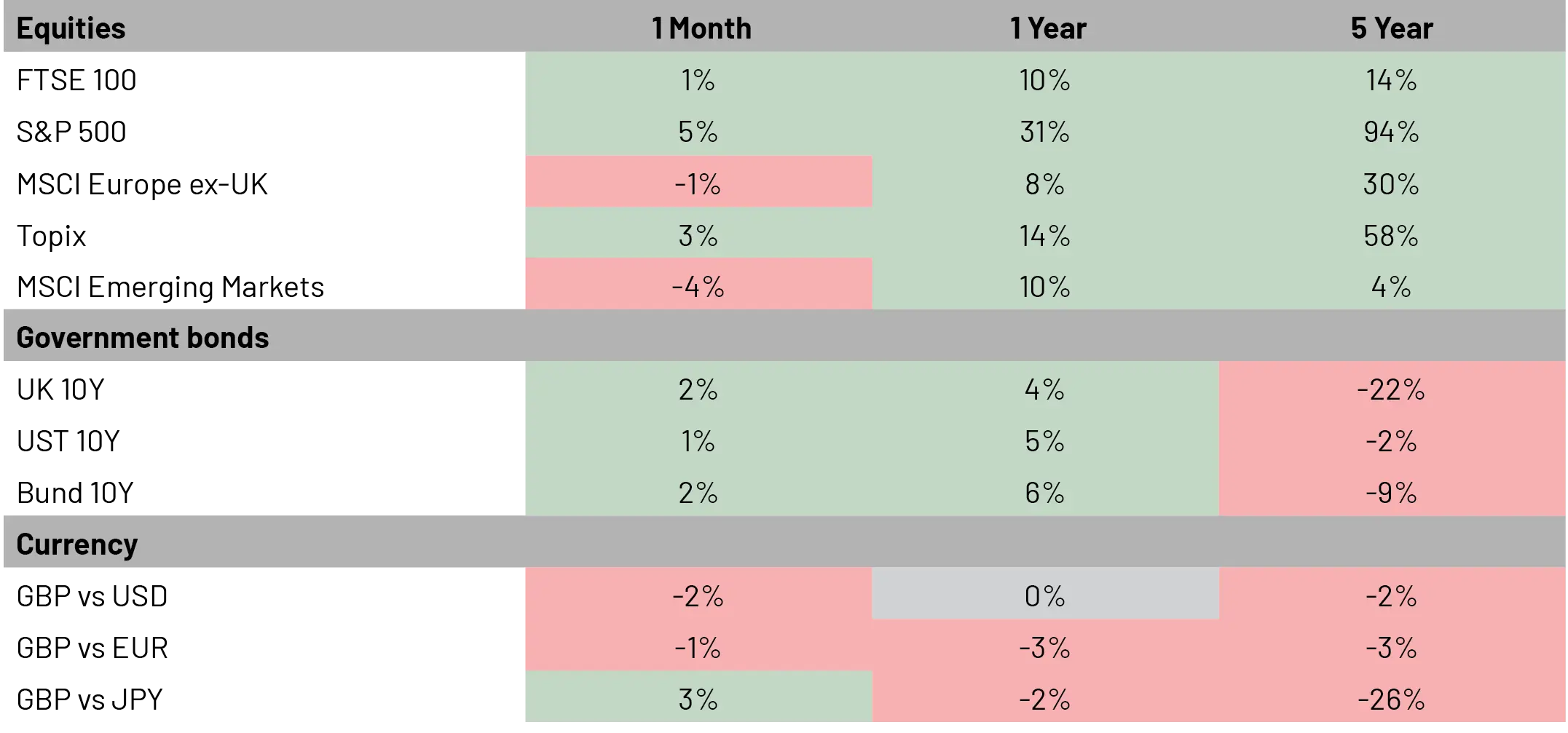

November Markets Wrap

Notwithstanding the S&P 500’s growth over the course of this year, US stock growth was further bolstered by a Trump win in the beginning of November. Markets grew optimistic of the policies that could boost US stocks after the republican president’s victory.

Bitcoin and the US dollar also benefitted from the same optimism.

Analysts are expecting US stocks’ upwards trend continuing well into next year and beyond. Goldman Sachs forecasts the S&P 500 will hit 6,500 by the end of next year (at 6,032 as at 29 November).

Meanwhile, effects of UK the Budget announcement at the end of October didn’t trickle into the financial markets – as expected. The tougher measures around government spending and borrowing could affect the economy down the line, but for markets it is business as usual.

Inflation levels, which in September had been celebrated to reach 1.7%, accelerated slightly to 2.3% in October on the back of higher energy prices. This increase could prompt the Bank of England to adopt a more cautious approach in its next rate-setting meeting, occurring on 19 December.

Market Moves

Source: Bloomberg. Data as of 2 December 2024.

What we’re watching in December:

- 11 December: US inflation figures for November

- 12 December: ECB interest rate decision

- 18 December: UK inflation figures for November

- 18 December: US Fed interest rate decision

- 19 December: Bank of England’s interest rate decision

You can download the commentary as a PDF here.

I confirm that I am a Financial Adviser, Solicitor or Accountant and authorised to conduct investment business.

If you do not meet this criteria then you must leave the website or select an appropriate audience.