Monthly commentary

Monthly musings: One game at a time

Following the global financial crisis and Covid-19, central bankers have never had a higher profile. After every meeting, there is a post-match interview style statement; financial journalists try to get the policymakers to tell them what’s going to happen next, and the policymakers politely explain that they don’t know, and they’re just taking it one match meeting at a time.

And so we saw with the US Federal Reserve this month. The headline was a 0.5% cut in interest rates (a thumping win). But the tone of Jerome Powell’s statement was almost entirely out of the post-match playbook:

“We've been very patient about reducing the policy rate. We waited, other central banks around the world have cut, many of them several times. We've waited and I think that that patience has really paid dividends in the form of our confidence that inflation is moving sustainably under 2%... I do not think that anyone should look at this and say oh, this is the new pace.”

Did you spot the key theme?

Patience doesn’t get a lot of traction in the modern market. At the start of 2024, the market was expecting rates to be cut five or six times, and the Federal Reserve proved impressively impervious to the pressure (a bit like a manager ignoring the crowd’s cries to substitute on a favourite player).

But the season is far from over. And the pressure won’t let up. Although inflation is coming under control, policymakers are soon going to have to switch their focus to growth. There’s a lot of excitement and speculation over whether such a big cut indicates the start of a recession; the Fed also started cutting cycles with 50bp back in 2001 and 2007, which led to a recession within months.

But there are two points before dissolving into doom and gloom. Rate cuts don’t cause recessions – they are an attempt to prevent it. And the policymakers are just as aware of monetary policy history as the market.

Remember that economics in general – and monetary policy in particular – is a social science, not a physical one. The rules and laws are constantly evolving and changing along with the wider world – again, a bit like tactics in sport shift over time. The people in charge are both learning lessons from history, and also making new mistakes (for the next generation to learn from).

So, stereotypical and lacklustre as it sounds, we think the best thing to do is take the Fed’s advice and blend it with our own approach. Be patient, stay diversified, and focus on the long term, rather than worry about week-by-week results.

September Markets Wrap

The Labour government spoke of a “painful” Budget announcement coming up on 30 October, knocking consumer confidence down to its lowest levels in the UK since Covid-19. This is despite the fact that inflation showed signs of stability, remaining at 2.2% in August, unchanged since the previous month.

This slowdown in inflationary pressure certainly gave the Bank of England more confidence in keeping the rate unchanged in the latest monetary policy meeting. As it stands, traders have priced in rate cuts in November and December.

In contrast, the Federal Reserve, which had decided to hold rates in the August meeting, decided to begin cutting rates from September in a largely expected decision. Chair Jerome Powell said the 50bp September cut would help to limit the possibility of a downturn. Like in the UK, inflation could still rise and therefore the Fed is acting carefully; this means that, even though the market has priced in a few more rate cuts this year, analysts could be overestimating the amount of easing if inflation doesn’t take the expected trajectory.

Overall, global developed markets were steady in a month of monetary policy changes and some consumer uncertainty. We did see a last-minute boost in the emerging market space, with Chinese stocks leading the way in the wake of heightened stimulus being announced by the Chinese Government. Over the second half of September, Chinese stocks returned 25% to investors who had experienced some pain in holding businesses in the region.

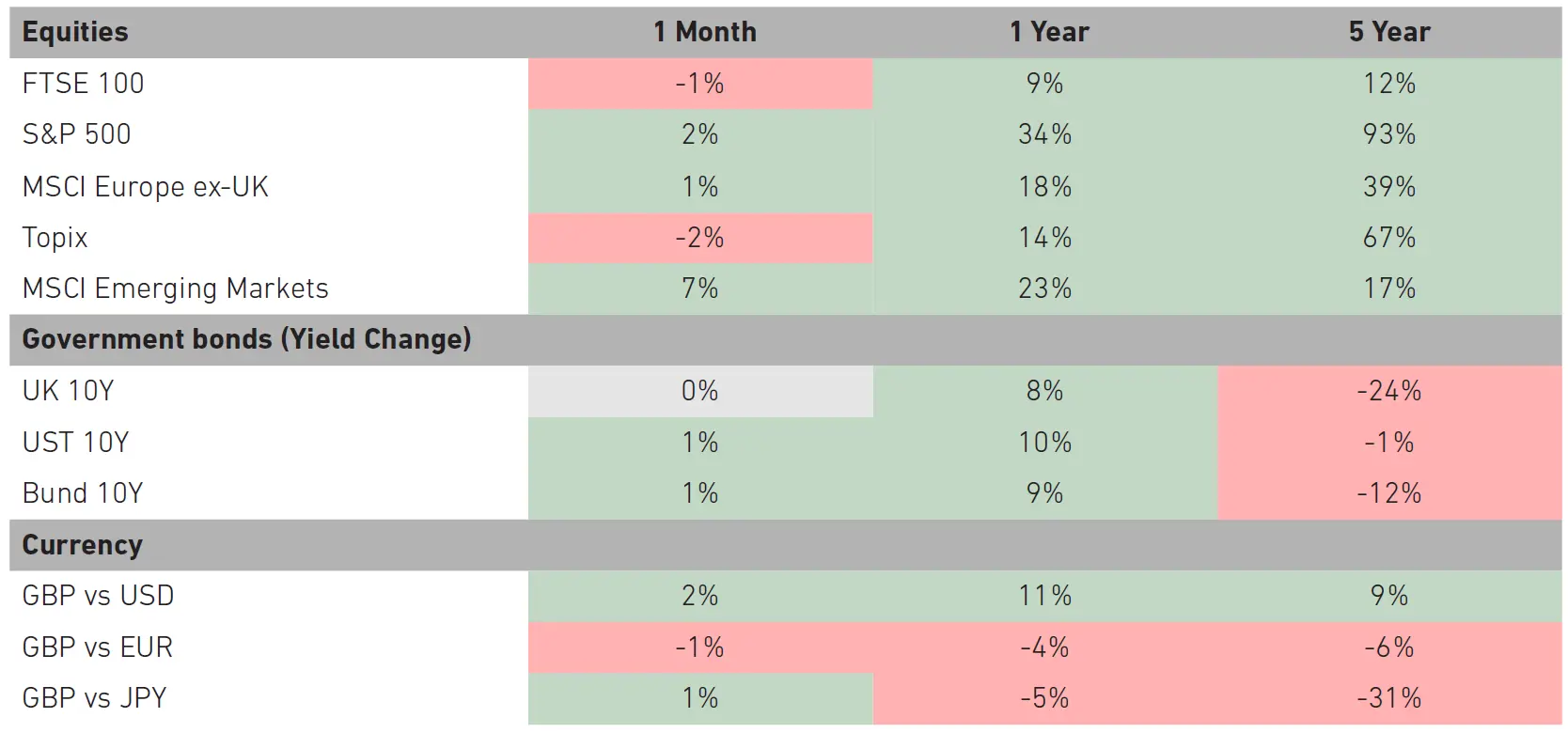

Market Moves

Source: Bloomberg. Data as of 30 September 2024.

What we’re watching in October

- 11 Oct: US CPI

- 17 Oct: ECB interest rate decision

- 30 Oct: UK Budget

You can download the commentary as a PDF here.

I confirm that I am a Financial Adviser, Solicitor or Accountant and authorised to conduct investment business.

If you do not meet this criteria then you must leave the website or select an appropriate audience.