If I were an influencer pt. 2: the comments section

Cash savings accounts are finally offering a meaningful return. But that doesn’t mean that investors should change their portfolios.

Last quarter, I tried to imagine that we were producing social media content. The obvious 'hook' in today’s investment climate was, and still is, 'Three BIG problems with cash'. This turned out to be a wildly popular topic amongst our followers (you, the readers). Like any good content creator, inspiration for future topics often comes from the comments section.

So, this quarter, I thought I’d look at the most popular questions our readers have asked...

1. “Current interest rates are high enough for me. What’s the point of investing?”

The rise in interest rates over the last few years has been astonishing. Just 18 months ago, they were close to zero. Now: the highest they’ve been in a decade. And looking at the actual number, cash rates of 5.25% are pretty attractive. Lock it away for a year, take no investment risk and get paid a handsome return over and above what the Bank of England believes will be long-term inflation (2%). What could be wrong with that?

In isolation, we agree that this is a great ‘risk-free’ return. The question we’d ask back is, if you think interest rates are worth locking in, why just do it for a year? Why not lock it in for longer?

This is what the bond market offers you. Today, you can lock in a ‘risk-free’ return over five to 10 years of almost 4.5% per year just by lending to the UK government. And the UK government has an excellent track record of paying lenders back. Or you can go further and lend to a range of different borrowers too. From big, stable investment-grade companies like Visa, Disney and HSBC to smaller, but still pretty serious high-yield companies, which include the likes of Nissan, Ford and Vodafone.

How best to lock in those higher interest rates? Well, the 7IM Moderately Cautious portfolio has around two thirds of its assets in income-generating assets. From short-term government bonds all the way to corporate bonds that mature decades into the future. Put together, investing offers the chance to lock in higher interest rates across the world, to different types of lenders, over multiple years – something an annual cash account can’t do.

2. “Even 7IM are saying we’ll be sideways with volatility for a while. Why hold any equities?”

We’ve established that a large part of a 7IM portfolio will lock in higher interest rate exposures for longer than cash can currently. But our analysis (and history) suggests that this won’t be enough to deliver inflation-beating returns over the long run. This is why we need equities.

The problem with equities is that they can be scary. It can seem like they are subject to uncontrollable global forces; investment banks, hedge funds and traders all moving the markets in unpredictable ways. Putting your hard-earned cash into that maelstrom doesn’t seem appealing.

But that’s a bit like never going outside again because there was once a thunderstorm. But the storm subsides. This was a key finding from Nobel prize winner Robert Shiller1. He found that most of the short-term movement in equities was not explainable by the underlying health of the company. This sounds scary. But hold equities for long enough, he says, and they find their way back to something more sensible.

Take the FTSE 100, a market of large companies listed in the UK; AstraZeneca, HSBC and BP. Altogether, the index has a dividend yield of over 4%. While the dividend yield is not as certain as, say, the yield on a UK government bond, it’s pretty stable over history, whether markets are up, down or sideways. This is because the CEOs of these companies have an incentive to keep their investors happy – and the best way to do so is to pay them back a cut of annual profits.

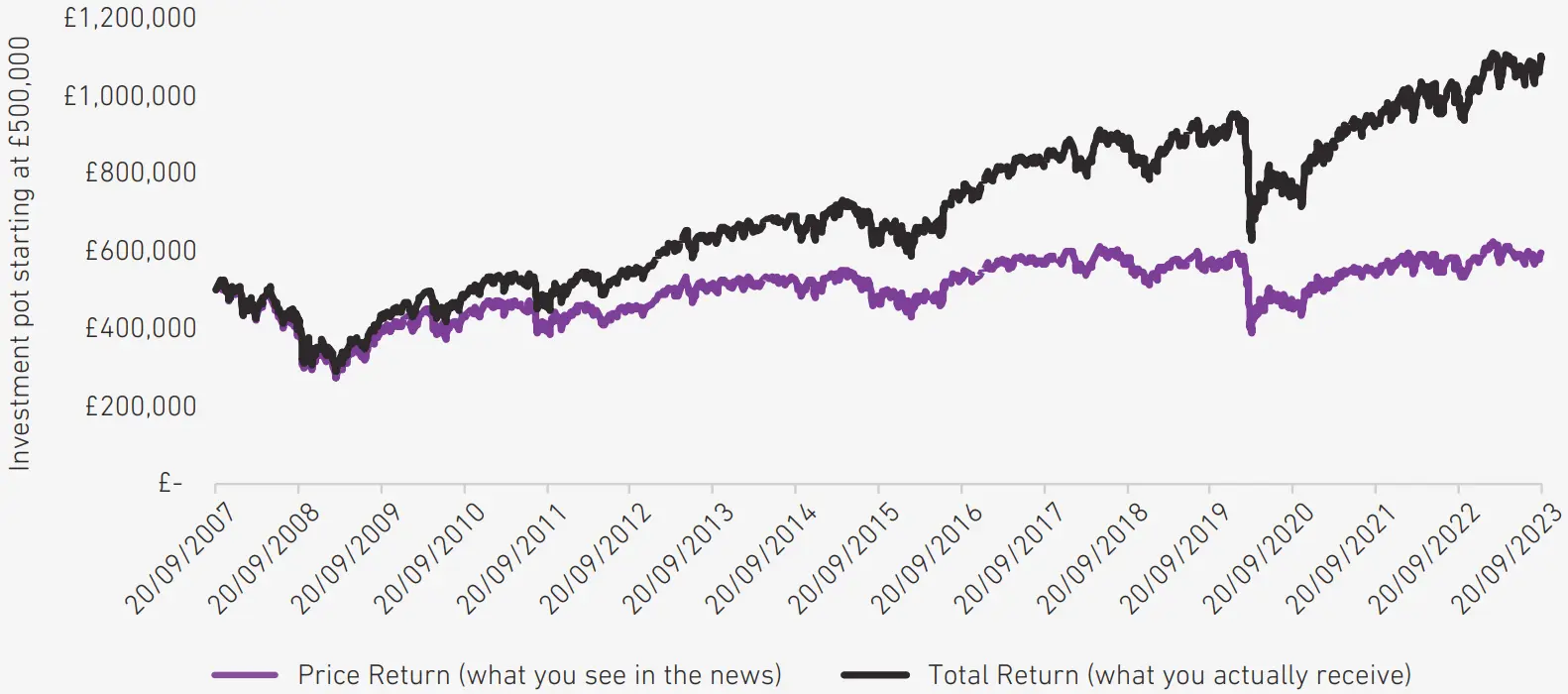

The impact has been that since 2007 (the peak before the financial crisis), about 80% of the market’s returns (nearly 5% per year) have come from the dividends (see graph on page 9). That includes two major recessions. So, while it’s always tempting to wait for a 'better entry-point', this example shows that you don’t need to if you want a slice of inflation-beating returns.

3. “The last few years have been underwhelming. When am I going to see a return on my investment?”

7IM portfolios mix equities, which look to offer an inflation-beating return, alongside bonds, which look to provide the certainty of locking in interest rates. But it isn’t lost on most people that investment returns haven’t quite stacked up over the last couple of years. However, these points are connected.

Bonds have lost money in that period, with the UK gilt market being one of the worst hit. This is because interest rates have risen (causing the price of bonds to fall) – in the UK, yields have gone from close to 0% all the way to 4.5%. So, what has hurt investors recently is what also makes bonds even more attractive now – prices are lower, and yields are higher. The upshot is the bond part of your portfolio is now much more likely to make a high return.

Similarly, equities have been sideways and volatile for a couple of years now. But what we tend to find is that periods of equity market choppiness eventually give way to stronger returns. Remembering that CEOs are keen to return money to shareholders through things like dividends when they can, means that periods of low returns don’t usually last too long (otherwise there’d be no investors left!).

Put together, the last couple of years of downward bond returns and sideways equity returns have pushed up the guideline returns of portfolios. Take the 7IM Moderately Cautious portfolio again, where long-term annual returns have gone up from 3.5% to 5.5% in the last two years. This is by no means a guarantee that returns will come immediately. But there’s never been a better time to gain exposure to these inflation-beating, cash-plus long-term returns. The chance won’t be here forever – the last two years have shown how quickly things can change. And the cost of moving to cash now could become costly very quickly.

So, what has hurt investors recently is what also makes bonds even more attractive now – prices are lower, and yields are higher.”

Equity returns – don’t listen to the headlines!

Investors often hear about the price movements of the stock market… 'The FTSE climbed x-points to y-thousand and something'. This gives the impression that investors need to wait for big price moves to make their returns. Instead, dividend returns (which is just a slice of company profits) have a big part to play.

Take the FTSE 100 since 2007. While the price movement has delivered a return of less than 1% per year, investors actually received a return of almost 5% per year. That’s the difference between a 15% return and doubling your money! Through two major recessions, companies have found a way to pay investors who stick with them through good times and bad.

Source: Bloomberg Finance L.P.

More from 7IM

I confirm that I am a Financial Adviser, Solicitor or Accountant and authorised to conduct investment business.

If you do not meet this criteria then you must leave the website or select an appropriate audience.