Profiting from the expected and unexpected

What do engagement rings, wine lists and digestive biscuits all have in common? How about if I include an anchor as well?

Confused?

Let me explain. Most people are familiar with the idea of spending a month’s salary on a ring1, many will have all experienced the temptation to avoid the cheapest bottle of wine on a menu2, and everyone is aware that digestives aren’t as big as they used to be3!

What they have in common is being real-life examples of ‘anchoring bias’. We take the first piece of information we come across, and that becomes our baseline. I should spend x on a ring, this second bottle of wine should cost y, a digestives packet should be this price, whatever its size.

And, as ever with human behaviour, it crops up in the investment world too. As we enter 2025, it’s hard not think about year-ahead projections as an obvious culprit. Use what happened last year as an anchor for what will happen in the next 12 months. Politics a little volatile this year? Expect the same. Growth slowdown? Tough times ahead. Good year for markets? Expect another.

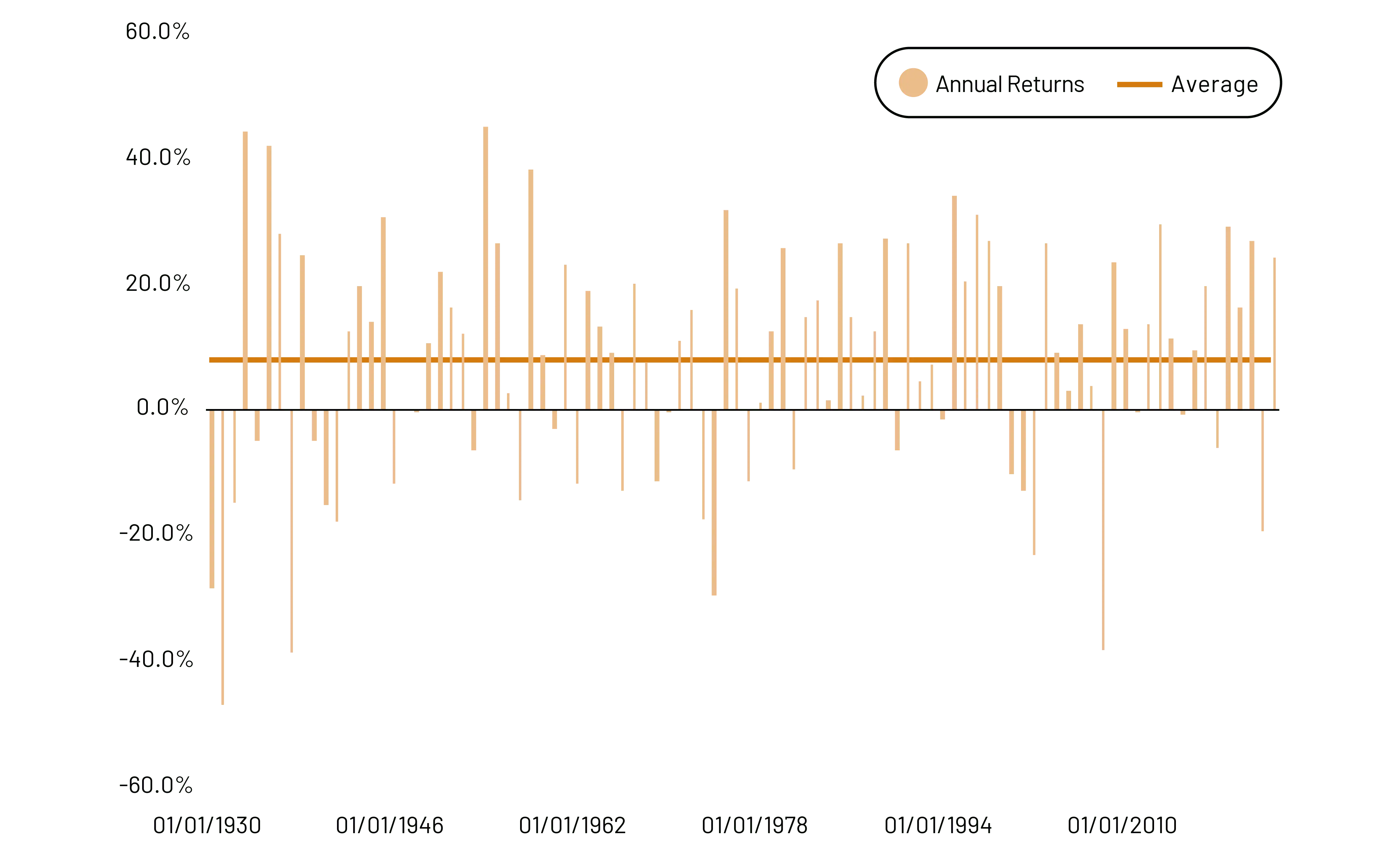

The trouble with this line of thinking is that it belies the way markets actually work. While markets tend to deliver an ‘average return’ (e.g. people tend to think of equity returns as an 8% average over the long term), there are some huge swings around this average. And these swings are driven by surprises – which, by definition, you don’t see coming (see ‘Equity returns aren’t stable’ box)!

First, let’s consider equities to see this.

For markets to deliver more than the elevated expectations, the possible drivers of this are endless. It could be something on the horizon – a borrowing binge, or maybe Trump’s new administration decides to turn on the stimulus taps. Or it could be something less obvious – perhaps a new technology makes energy incredibly cheap, or something like Putin retreating. All are plausible.

And fo markets to fall from here? Maybe higher interest rates finally start to bite. Or perhaps the anti-trade policies coming from the US eat away at profit margins. But there are less obvious outcomes too – tech regulation comes in or maybe Putin expands even further. The possibilities can become endless.

And how about bond markets? While bond markets swing around less than equities do, are the actions of central bankers any more predictable? It can seem tempting to believe that they are – after all, if you knew the mind of Andrew Bailey, surely there’d be an advantage?

Well, unfortunately the same anchoring problems apply – you’ve just moved them onto someone else’s plate! Central bankers are as human as the rest of us, and therefore just as susceptible to surprises. Maybe inflation takes off again, as tariffs bite. Or maybe growth slows so much that rates need to fall. Or a war. Or a food crisis. Again, there are too many possibilities to lay out.

The point is that worrying about the causes of big swings is less important than accepting that they will happen from time to time. And most important of all is to understand how portfolios might react when those surprises do happen. We want to avoid anchoring on what has happened (and why), and think about what might happen, and what it would mean.

Profiting from the expected... and the unexpected

If market returns are driven by surprises which are inherently difficult to predict, then how should we build portfolios?

First, it is important to remember that even if nothing surprising happens that’s not too bad an outcome! Equities should appreciate a little, and pay a bit of a dividend, while bonds will pay a coupon. If the world goes exactly how markets are expecting, it still pays to invest.

And if the surprises come? Portfolio diversification is the best weapon. Different investments are affected by different surprises. Blended carefully, they can push and pull in different directions, leading to a smoother investment journey.

If market returns are driven by surprises which are inherently difficult to predict, then how should we build portfolios? First, it is important to remember that even if nothing surprising happens that’s not too bad an outcome!”

So, in average periods, everything should do ok. German government bonds, and Japanese industrial shares, and British energy company debt, and Indian tech firms (etc., etc.) all chug along nicely. During periods of upheaval, some investments may falter, others will thrive, and others may hold steady – the good and the bad cancel each other out; and the whole portfolio should end up at average (or ideally just above).

At 7IM, we assemble portfolios with this principle in mind. We incorporate Alternatives into the mix, broadening the range of responses to unexpected events. By combining asset classes that react differently to different surprises, we aim to smooth client returns over time.

Anchoring is a natural tendency; markets often extrapoate recent trends, making unexpected outcomes difficult to anticipate. As we enter 2025, we acknowledge the challenges the year will bring.

There’s political upheaval at home and abroad, there’s technological upheaval everywhere, and higher interest rates still pose a challenge. Any of these forces, plus others, could lead to surpriing outcomes. But rather than trying to predict surprises, we focus on building portfolios designed to perform, no matter what the future holds – and no matter where our brains might have anchored!

To try and circumvent our brains’ tendency towards emotion, we build statistical models which strip the psychology away. We let these models (built without reference to short-term noise) tell us when there might be chances to move portfolios significantly. At the moment, they’re suggesting that there’s nothing too extreme out there in the world, so accordingly portfolios shouldn’t be extremely positioned. Hence a reasonably neutral equity and bond allocation, spread around the world. We’re letting the market currents do the work for now and keeping an eye out for opportunities.

S&P Annual Returns vs Average

Source: Bloomberg Finance L.P.

1 The idea that we spend a portion of our salary on an engagement ring is surprisingly recent https://www.theatlantic.com/ international/archive/2015/02/how-an-ad-campaign-invented-the-diamond-engagement-ring/385376/

2 We use the first bottle as a baseline, but don’t want to look cheap

3 Shrinkflation in digestives is rife. Since 2014 the size of digestives has reduced by up to 28%! https://www.bakeryandsnacks.com/Article/2024/09/05/5-uk-products-hit-hard-by-shrinkflation/

More from 7IM

I confirm that I am a Financial Adviser, Solicitor or Accountant and authorised to conduct investment business.

If you do not meet this criteria then you must leave the website or select an appropriate audience.