Quarterly Rebalance Commentary

Overview

Markets continued their positive march upwards over the course of the last three months. Even a soft April was not enough to dampen positive spirits, with the UK market being an outright leader across the period (for a change!).

February witnessed the S&P 500 hitting 5,000 for the very first time, bringing much excitement to financial markets. All attention was on corporate earnings - Goldman Sachs even referred to Nvidia as “the most important stock on planet earth”, and the chip manufacturer exceeded already high earnings expectations – emphasising exactly how powerful innovation in AI is becoming.

Through March, while the US saw a slow improvement in its economic indicators, the picture in Europe and the UK was not so clear-cut. The latter, for instance, grappled with a longer-than-expected slowdown in inflation, and with sluggish economic growth. The Bank of Japan’s decision to end an eight-year streak of negative rates also made headlines, marking its first hike since 2007.

But none of this affected investor sentiment! More developed markets pushed into all-time high territory, with Europe and Japan joining the party.

In April, however, weaker data coupled with policymakers’ hawkish statements posed a challenge for the optimists. Uncertainty rippled across global markets, leading to declines in many of the largest equity indices. The UK and China managed to buck this trend, delivering some timely positive performance and demonstrating the value of diversification in volatile markets. The biggest declines came from Japan and the US after an incredibly strong start to 2024.

May has started much more like February and March, with the concerns of April seeming a distant memory already. This marks a run of six strong months now for markets, and at the time of writing, it shows no signs of slowing down!

Core investment views

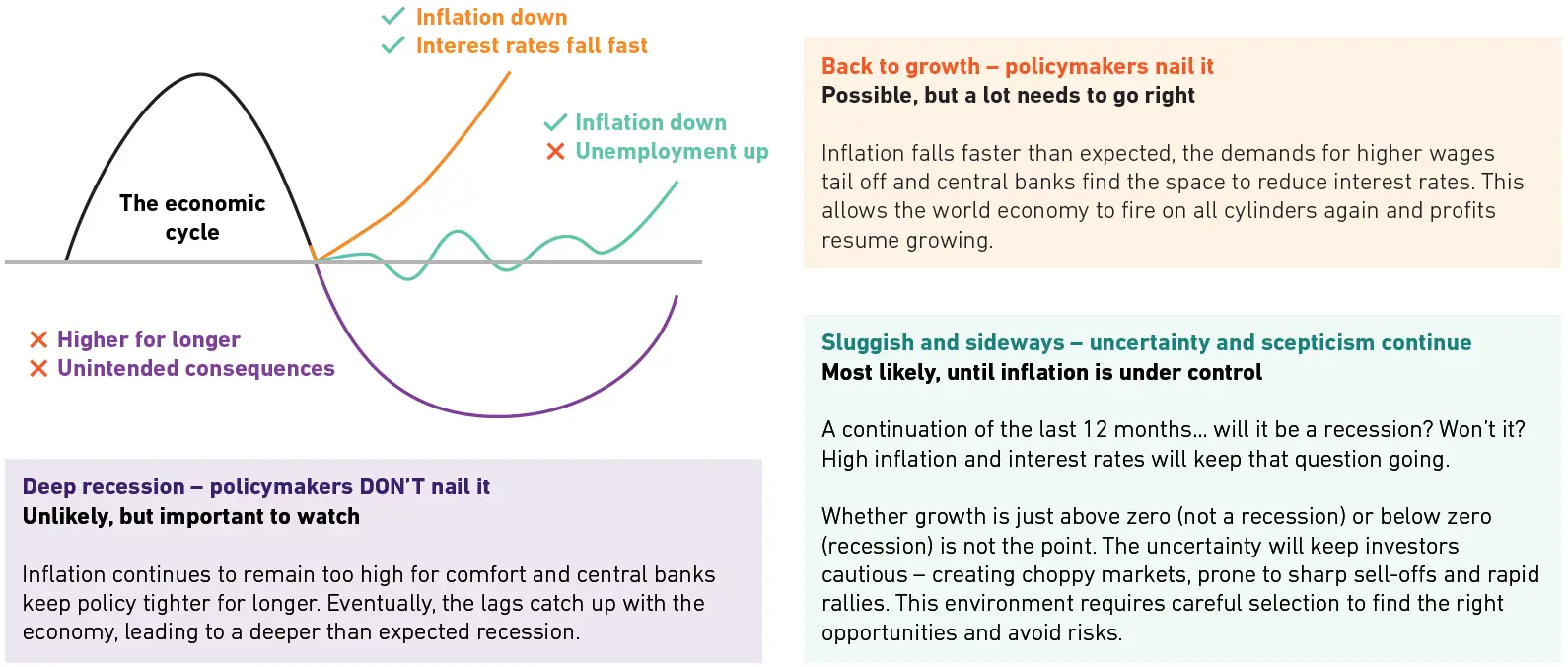

Despite the general optimism, it would be foolish to adopt a fully positive stance at any point in time. Even in a largely positive market, it is important to make sure no stone is left unturned to avoid any surprises on the downside. That is what we’re doing at 7IM - our properly diversified portfolios enable us to grow in every kind of environment:

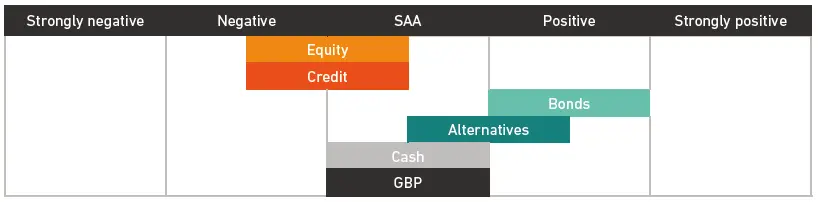

Tactical Asset Allocation

In an environment with lots of uncertainty and a lack of confidence, we want to make sure portfolios are insulated against shocks, while still generating sufficient returns to make investing worthwhile. And we think our portfolios are set up to do just that.

Portfolio positions

There’s no one answer… When managing a diversified long-term portfolio, there shouldn’t be a single ‘big’ call. For an outlook which calls for selectivity, especially in the medium and short term, we’re finding lots of different opportunities – both to protect capital and to grow it.

| Long term: Thematic | |

|---|---|

| Healthcare companies | The future of humanity |

| Climate transition leaders | Investing in a greener world |

| Alternatives | Diversify your diversifiers |

| Metal & mining companies | Invest in the commodity supercycle’s main beneficiaries |

| Medium term: Opportunities | |

|---|---|

| Avoid concentration | Thinking differently about US equity exposure |

| AT1s | European bank bonds are more resilient than feared, and yields are attractive |

| Short term: Portfolio risk appetite | |

|---|---|

| Underweight equity risk | Reduce equity exposure as returns will be limited for the time being |

| Overweight bond duration | Bonds can do well if inflation continues to fall |

Asset allocation changes

This quarter, we have implemented the first phase of the move towards the 2024 Strategic Asset Allocations after completing our annual refresh. Additionally, we made a few tactical changes to portfolios this quarter. Here are the combined asset allocation changes:

- A small strategic increase to equity, primarily through US and European allocations

- A small rotation from corporate bonds into government bonds

- A minor reduction in Alternatives exposure

- A trim to the AT1s position as prices recover back to their highest in two years

- Moving UK Mid Cap exposure back up to a neutral weight by rotating out of their larger UK peers following strong performance from FTSE100 companies

- Removing the Healthcare Innovation position and rotating the proceeds into the US diversified position (only relevant for higher-risk profiles).

Manager changes

This quarter, we have:

- Added the HSBC European Index Fund to portfolios to provide exposure to larger European companies in a very cheap and efficient vehicle.

Please note: All of the comments in this document refer to the models we run on the 7IM platform, but the models are also available on a range of other platforms. As much as possible, we try to replicate the models we run of the 7IM platform across all platforms, but due to differing security availability, not all of the points outlined in this document may be relevant across these platforms. If you are unsure whether certain changes apply to models on a specific platform, please reach out to a member of the team.

You can download the commentary as a PDF here.

I confirm that I am a Financial Adviser, Solicitor or Accountant and authorised to conduct investment business.

If you do not meet this criteria then you must leave the website or select an appropriate audience.