The Bank of England is catching up

What is the latest from the Bank of England?

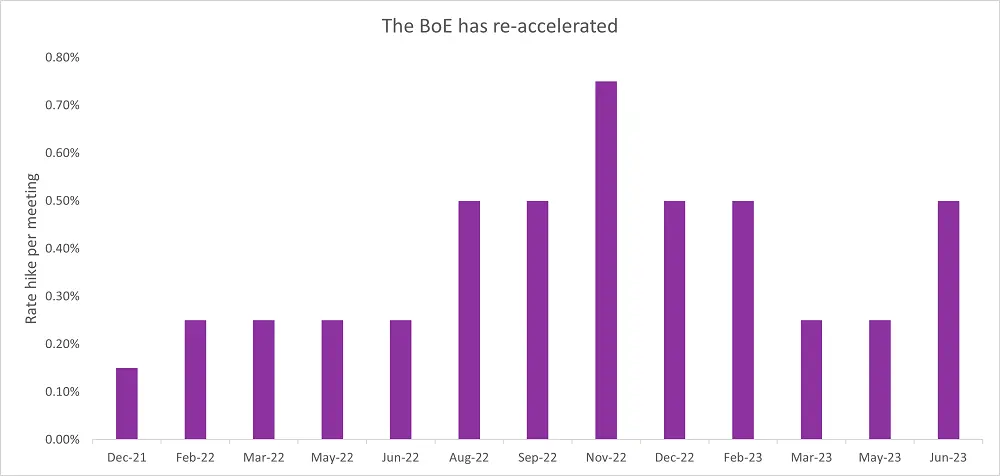

Yesterday the Bank of England raised interest rates by 0.5% to 5%. We’ve already had a few of these – yesterday’s rise marks the 13th rate hike since the hiking cycle began in 2021. It also marks the fifth time in those 13 that it has been 0.5% or higher (remember November’s 0.75% hike?!). What has drawn attention, though, is that Bank has re-accelerated the process, rather than sticking to the usual slower pace of 0.25%. In addition, the market has gone on to expect interest rates to hit 6% by the end of the year. Over in the US in contrast, the market is expecting the Federal Reserve to pause soon and even cut early next year. Why the divergence?

Source: Bank of England, 7IM

The UK is behind the US

There are many differences between the UK and the US economies. The stimulus measures they undertook during the Covid recession were different (the US went for big cheques into people’s accounts while the UK preferred the slower furlough approach). Additionally, the UK imports more food, has much closer proximity to European energy concerns and has a bigger squeeze on the labour market. Put together, the UK’s inflation problem has become more drawn out. This can be seen by comparing the US’s ‘core’ inflation (stripped of volatile components) to the UK’s. The US has at least peaked and, while slow to come down, isn’t showing many signs of accelerating. The UK, on the other hand, has not shown signs of peaking. The Bank of England is erring on the side of caution.

There is light at the end of the tunnel

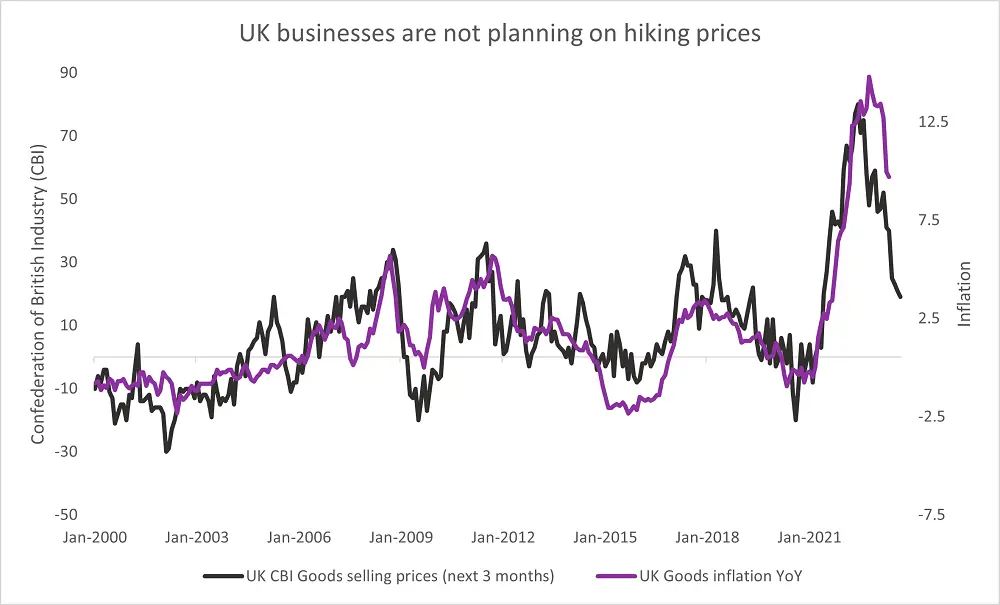

It’s well known now that the canary in the inflation coalmine was global supply chain pressures. People locked in their home, desperate to spend on something, anything, splurged on goods. As a result, businesses across the world ratcheted up their prices for goods across the board. With supply chain pressures mostly gone, those same companies are seeing fewer opportunities to raise prices. The chart below shows a survey of UK businesses planning to raise prices over the next three months. Last year, almost all companies were planning on raising prices. Note that figure is falling close to zero. And where business prices go, inflation tends to follow… eventually.

Source: CBI, ONS, 7IM

What it means for 7IM portfolios

Our portfolios are well insulated from UK-specific shocks like this. Our equity exposures listed in London tend to be the larger companies where around 70-80% of revenues come from anywhere but the UK. Similarly, in the bond parts of our portfolios, our exposures tend to be tilted towards the US and European parts. Overall, our view remains unchanged. We believe the rate hikes in the US are slowing its economy down enough to lead to a recession, while inflation will continue its slow descent downwards. Our positioning continues to favour an underweight to equities, an overweight to bonds and alternatives and the latest news from the BoE doesn’t change that.

Discover more

I confirm that I am a Financial Adviser, Solicitor or Accountant and authorised to conduct investment business.

If you do not meet this criteria then you must leave the website or select an appropriate audience.