2023; are you ready for regime changes?

2023, and still no sign of the ‘Roaring Twenties’

Three years ago, lots of ‘Year Ahead’ pieces were talking excitedly about a new decade of growth for the global economy. The comparison to the post-WW1 ‘Roaring Twenties’ was used a lot – finally, the world would move out of the low-growth, low-inflation, low-interest-rate era and put the Global Financial Crisis behind it. Flapper dresses and speakeasies, here we come!

Then, everything changed. 2020 was dominated by COVID and lockdowns, while 2021 was all about the arrival of vaccines and freedom (except for China). At this time last year, optimism was building again that the growth boom had been delayed, rather than derailed. The world economy would settle down in 2022…

It didn’t.

2022 was a year of consequences – the result of various actions and decisions over previous years.

- COVID-related stimulus pushed global demand and spending too high in 2021, pushing inflation in 2022 to multi-decade highs

- The last few years of US and European politics – global powers retreating from the world stage to deal with internal issues – emboldened Russia to invade Ukraine in February, and China to become more aggressive about the future of Taiwan

- The end of a low interest rate environment brought various bubbly investments down to earth, led by US technology and the chaotic wild west of crypto currencies

- The extreme polarisation of politics in the last few years resulted in a shift back towards a calmer centre-ground – although the transition was particularly messy here in the UK.

In addition to market turmoil in bonds and equities, these consequences have also led to significant shifts in the way the world works. These regime changes will become more apparent over the course of 2023 – and indeed the rest of the decade. The twenty-twenties might not be roaring, but they certainly won’t be boring…

Regime change: Economic growth

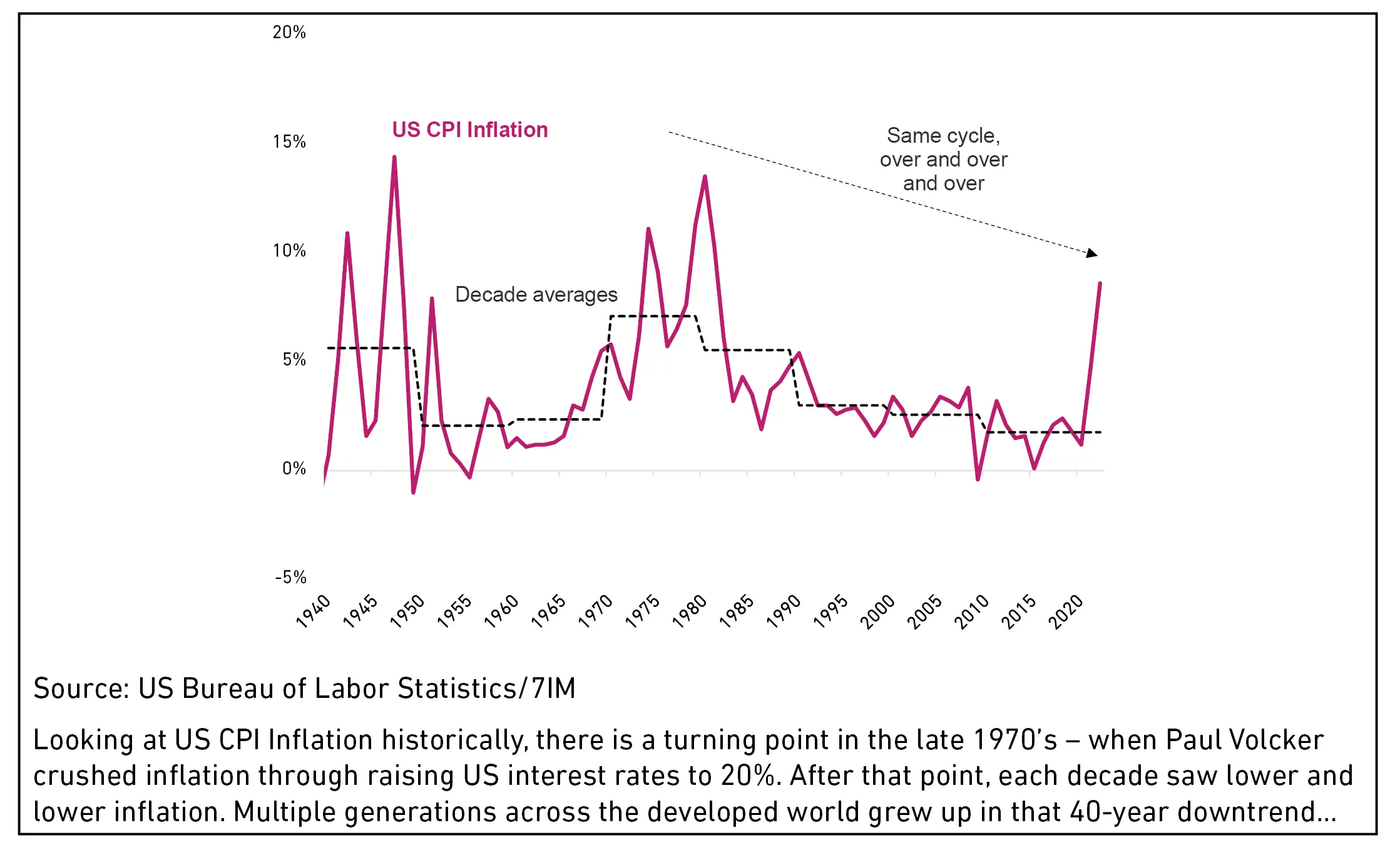

The next period of economic growth is going to feel uncomfortable. It’ll be different to the economic cycles of the last three or four decades. That’s because of the regime change in the two key ingredients that dictate the kind of growth cycle you end up with: inflation and interest rates.

Since the 1970s, every consecutive period of growth between recessions saw lower interest rates and lower inflation than in the one before. Inflation by decades shows the same thing – see the box below.

From 1980 onwards, each cycle tended to echo the one before. No matter how bad the recession, it would finish with the new lows in inflation and a fall in the cost of borrowing.

The next economic cycle will be different. In the next decade, interest rates won’t be lower than in the 2010s – and inflation is unlikely to be either. For the first time in half a century, the cost of borrowing money in the developed world will be higher than before. Projects that made sense when money was cheap – whether infrastructure, or product development, or property purchases – will suddenly have much higher hurdles to clear.

Ultimately, a more challenging business environment should drive increases in productivity and in competition. But that means waving goodbye to the old world – which is likely to be a difficult process. That’s why there is likely to be a global recession next year. Pain before progress.

Regime change: Global trade and geopolitics

No one thinks about global supply chains until they fail. Previously, the snarl-ups have tended to be localised. Floods in Thailand. Earthquakes in Japan. A fire in Rotterdam port. Even a massive ship stuck in the Suez Canal. The global economy hesitates, then finds another way – prices and delivery routes adjust.

In a static global political environment (or one dominated by one superpower), market forces usually work just fine. But that’s no longer the shape of the world, and the last three years have highlighted that in some areas, relying on pure economics isn’t anywhere near enough.

For key strategic national interests, supply chain security trumps supply chain efficiency. For Europe, right now, the most pressing issue is energy. Relying on Russian imports was fine, until it very much wasn’t. For the United States and China, the supply chain concern is technology. The most traded good in the world isn’t oil, it’s semiconductors, which represented 15% of all global goods trade in 2020. Most of the world’s semis come from Taiwan – more than 50% of them from one single company!*

There are other strategic areas too – nuclear power plants, military equipment, vaccines and other medical treatments. Suddenly, ‘offshoring’ looks like a risk to national security.

The supply chain shifts become even more interesting when we consider the shift towards clean energy. The geographical distribution of natural resources helps to shape history (think of oil in the Middle East). And lots of the metals and minerals needed for the world to go green are in countries that haven’t held the levers of power before. Chile has a quarter of the world’s copper reserves, and 42% of lithium reserves. Indonesia has a fifth of the world’s nickel, while the Democratic Republic of Congo has half of the global cobalt deposits. And Australia is the reserves runner-up in all four of those resources.

Regime change: Business models

Many of the most successful businesses (large and small) in the last few decades were all about intellectual property. Which is a fancy way to say that other than Apple, not many large companies make things. Amazon delivers to you, Google searches for you, and Facebook… builds a metaverse you aren’t interested in?

In high tech, the real world was irrelevant, imagination and the internet were enough. Anyone interested in starting a company and making millions headed to Silicon Valley to develop an app, or build a platform, or create a crypto-currency. With so much cash available (and so little return available in ‘safe’ investments), people were keen to speculate. Unproven business models were the way of the world. There would be failures or frauds like FTX or Theranos, but enough successes to counteract them.

And people were willing consumers! With cash in the pockets of the middle classes, new apps were seized upon to make life easier – for dating, food delivery, tv-streaming, everything.

In a world of cheap money, those things made sense. But now the situation has changed. Consumers are worried about costs. Why renew your Netflix subscription when BBC iPlayer is free? Why get food delivered if home cooking is cheaper? Why upgrade your phone if the old one works?

That shift in consumer demand can break business models. Investors won’t be looking to speculate, or to back moonshot ideas. They’ll want reliable cash-flows and proven products. They’ll want money in the next year, not the next ten years. Which means that the winning companies of the next cycle (in share price terms) will be those with tangible assets and proven business models. Mining and energy companies with the ability to provide the world with what it needs to keep turning. Industrial businesses which make essential, but unexciting products. Food supplies, pharmaceuticals, and railroads. The new world still needs traditional companies. It just forgot that for a few years.

Implications

So how do we invest through this regime change?

There are a few points to consider (which we’ll talk more about through the course of the year)

- Expect investor psychology to swing violently. As people try to adjust, there will be highs and lows of sentiment. Keeping calm and avoiding reacting on a day-by-day basis is crucial.

- Be prepared to be nimbler, especially in fixed income. In previous high-inflation environments, interest rates moved often and big. Being aware of opportunities and taking profits in government bonds is likely to add real value.

- Don’t rely on the winners of the last cycle. In equity markets, that means avoiding overpriced and unproven businesses, and probably means dampening down on the tech giants too – there may come a time when they’re cheap enough, but it isn’t right now. In bond markets, that might mean avoiding expensive high-grade bonds and moving into higher-yielding but riskier areas.

- Diversify your diversifiers. We’ve built an alternatives portfolio which has delivered strong returns this year. It requires constant attention and monitoring, but it should be just as useful next year as last year.

*Source: Deutsche Bank

These regime changes will become more apparent over the course of 2023 – and indeed the rest of the decade. The twenty-twenties might not be roaring, but they certainly won’t be boring…

Find out more

You can download the article as a PDF here.

We’re excited to announce that 7IM for Private Clients, London, has now merged with, and rebranded to, Amicus Wealth Management.

This marks a vital step forward in our mission to deliver the very best wealth management for our clients.

While our name has changed, our values and commitment remain the same. We’ll continue to provide personal, bespoke financial planning, built around you.

Explore Amicus Wealth Management