Monthly commentary

Monthly musings: Is the MAGA honeymoon over?

In football, there’s a phenomenon called the “new-manager bounce”. A struggling team gets a new coach and becomes revitalised; the same group of players achieving spectacular victories instead of lacklustre defeats*. The equivalent period for world leaders is getting shorter and shorter, and even Donald J. Trump isn’t immune.

The past few weeks has seen a shift in market sentiment towards the US, and in particular, the assets which performed particularly strongly just after the election in November 2024. So what’s changed to go from married market bliss at Christmas, to it’s all over by Valentine’s Day?

It’s probably worth dealing with one thing first. This isn’t about Bitcoin falling to $85,000. While that might well be related to sentiment surrounding Trump, we’re more interested in the real economy and the assets which appear in portfolios.

Starting with the US economy, inflation expectations are rising while consumer confidence is dropping. There are a couple of reasons that we can put our finger on. The first is tariffs – and unlike Trump’s term, consumers now know what to expect. Prices will be going up. Which hurts their confidence.

The second factor is the employment multiplier. Elon Musk’s government efficiency drive might sound good to productivity economists and CEOs. But what ordinary people hear is “job cuts”. Close a government office in a small town, and suddenly everything else gets dragged down too. The employees might be “inefficient”, but their dollars are as valid as anyone else’s at restaurants and shops and theatres.

People are pointing to the reversal in post-election trends in asset prices to support this. Mega-cap tech (especially Tesla!) is struggling. The dollar is weaker. And US Treasuries are pricing in rate cuts (suggesting economic weakness ahead). The cherry on the cake is the fact that Warren Buffett is now sitting on his largest cash pile ever.

So, is it all over?

Well, just as we were cautious about the excitement in November, we’re just as cautious about the pessimism in February. The US economy is a beast. It takes a lot to shake it up. And there are other policies in the works which might be positive for assets. Tax cuts usually boost confidence, and a cessation of global hostilities would – in the short term – probably see some relief.

The red lights are not flashing for any of our economic indicators and one thing remains key, diversification. Diversified positioning in periods of uncertainty, provides the ability to protect in the short term, but also to take advantage of long opportunities that present themselves.

* As a long-suffering Spurs fan, I’ve seen a fair few of these. It’s a close-run thing between the Conservative Party and Tottenham Hotspur when it comes to leadership changes this decade…

Chart of the month

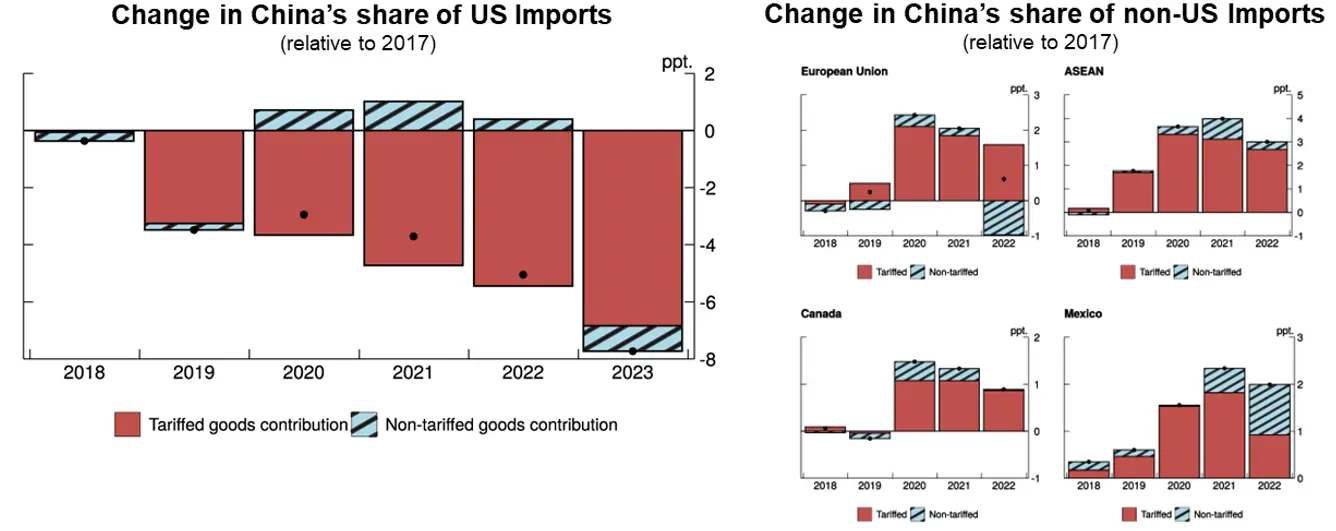

OK, fine it’s more like five charts. But they’re important to understand US trade policy (data is provided by the Federal Reserve).

Last time, he wanted to hurt China. So, he slapped on a load of tariffs. The result, on the left, was that US imports of Chinese goods fell sharply. Hurrah!

But the global trade system is sneaky. What happened was that the rest of the world increased their imports from China… and promptly shipped them off to the US. The containers basically just mademan extra stop, and ended up in the US anyway.

Source: federalreserve.gov

At some point in the last four years, someone explained that to Donald Trump. He’s reacted as if it were a deliberate betrayal from the rest of the world (rather than just how the market works), and so is clamping down on everyone. Tax everyone to hurt China, and to punish them for “helping” last time…

February Markets Wrap

In the February Bank of England meeting, the Monetary Policy Committee decided to cut rates by 25bp to 4.5%. The Bank based its modest reduction on moderating inflationary pressures, which remain “somehow elevated”, and weaker-than-expected GDP growth.

Later in the month, UK economy data confirmed a spike in inflation for January. The rise to 3% over the month represents a 0.5 percentage point increase, driven by slower-than-expected airfare price drops, higher private school costs and more expensive food and non-alcoholic drinks.

Rising inflation was also a pain point on the other side of the Atlantic. At the start of the year, food and gasoline prices pushed US inflation up, with tariffs on several countries having potentially accelerated the upwards trend.

Towards the end of the month, the effect of the 25% tariffs imposed across several industries, and across many other decisions made by US President Trump had a negative impact on markets, particularly the country’s benchmark index, which ended up losing 1% of its value in the month. It’s worth noting that longer-term gains in the S&P 500 remain healthy (see table below).

Meanwhile, in Germany the general elections resulted in a conservative minority win for the conservative party. Markets reacted positively to the results, suggesting optimism around the course of EU’s largest economy after a politically volatile year for the country. The DAX, Germany’s benchmark index, grew 5% over the month.

Market Moves

Source: Bloomberg Finance L.P. Data as of 3 March 2025. Past performance is not a guide to future returns.

What we’re watching in March:

- 6 March: ECB interest rate decision

- 12 March: US CPI data. It will be interesting how inflation has changed in Trump’s first couple of months in office

- 19 March: Federal Reserve interest rate decision

- 20 March: Bank of England interest rate decision

More from 7IM

You can download the commentary as a PDF here.