Monthly commentary

Monthly musings: A matter of perspective

There’s been a lot to take in over the past month – whether it’s in anticipation of the UK’s Budget at the end of October, trying to digest all the speculation around the US elections in early November, or dissecting the news around geopolitical conflict in many parts of the world.

But here’s the good news for investors: the world isn’t falling apart!

In fact, in our view, there’s a lot going well that just isn’t getting a lot of airtime.

Take inflation. A huge worry for much of the world over the last few years. Yet in the UK, CPI inflation has fallen under the Bank of England’s 2% target (1.7% in September), without the economy falling off a cliff. That’s a win!

And to that end, the Bank of England is now able to cut rates in earnest, reducing the likelihood of that cliff edge further. Lower rates feed through very quickly in the UK, so not only has growth been resilient, chances are it will get better!

And in fact, the UK situation is true across the world. Compared to the start of the year, rates are lower, inflation is falling and consumer confidence is holding up.

With that context, perhaps it’s no wonder that this year has been good almost regardless of where you’ve invested. From Developed Market stocks to Emerging Market Bonds, and everything in between; returns are lookin’ good. That wasn’t in many people’s forecasts at the start of the year!

Of course, it’s not like there aren’t things to worry about. US politics. The Middle East. The possible rise of AI and the future looking worryingly like an Arnold Schwarzenegger film.

So, no need to get carried away – spreading investments sensibly around the world is absolutely the right thing to do. But there’s no need to panic and head for the hills either; stop and take in the view!

Chart of the month

We thought we’d add a little picture every month – saves us writing another thousand words!

Imagine if I asked you who would win a race between Usain Bolt, Mo Farah and Adam Peaty? You’d need to know if it’s a sprint, a marathon, or swimming before you answered...

And the same is true for equity investing. Who do you back in a race? The S&P 500, the FTSE 100 or the NASDAQ? Well, over what period and in what economic circumstances?

Source: FactSet/7IM. Data as at 29 October. Past performance is not a guide to future returns.

If we’re talking about a three-year run, the FTSE 100 would actually get the win – despite the last three years being a seemingly not-stop hype cycle for tech and AI!

There’s a caveat: this assumes all the dividends have been reinvested (although even just on price alone, it’s a photo finish).

Dividends are like hydration stations along the way – you could keep going without them, but why wouldn’t you top up?!

October Markets Wrap

Despite the noise around the impending US election in the beginning of November, the geopolitical tensions, and the disparities across US corporate earnings… the S&P 500 ended the month pretty much as it started.

The negative headlines (about the big tech stocks not making quite as many billions of dollars as expected) were largely offset by some better-than-expected earnings outlooks for next year, particularly across the financial services sector. We are starting to see a trend of the recent winners underperforming a little – which we’ve been flagging as a risk for some time.

And it’s worth keeping an eye on how the market might react to future volatility. Having stronger opposing forces in the market might create more movement in both directions and investors might become a bit more sensitive to smaller changes. Properly diversified portfolios, however, hold the secret to growth amid volatility.

In the UK, inflation dipped below the 2% target, aided by lower petrol prices and air fares. More importantly, the 1.7% figure – which is below the Bank of England’s 2% target – was also supported by stubborn services inflation easing off. Will this prompt the Monetary Policy Committee to accelerate the rate cuts?

In the meantime, The Budget announcement, where the government said it would ramp up borrowing to unexpected levels (an extra £30bn a year), didn’t generate a Liz Truss-like reaction, nor did it see much positive reaction.

After Rachel Reeves confirmed that fiscal rules would change, resulting in potential extra borrowing, the 10-year UK government bond yield jumped to 4.3%. However, we would urge investors to remember that bond yields around the world have risen since mid-September – so the UK isn’t really out of whack.

We’ve said countless times that what happens in politics and government rarely attracts significant market movements. We’ve seen that in the Budget, and we’ll (likely) see that in the US elections. And even in the event of any short-term wobbles, there might be opportunities presented.

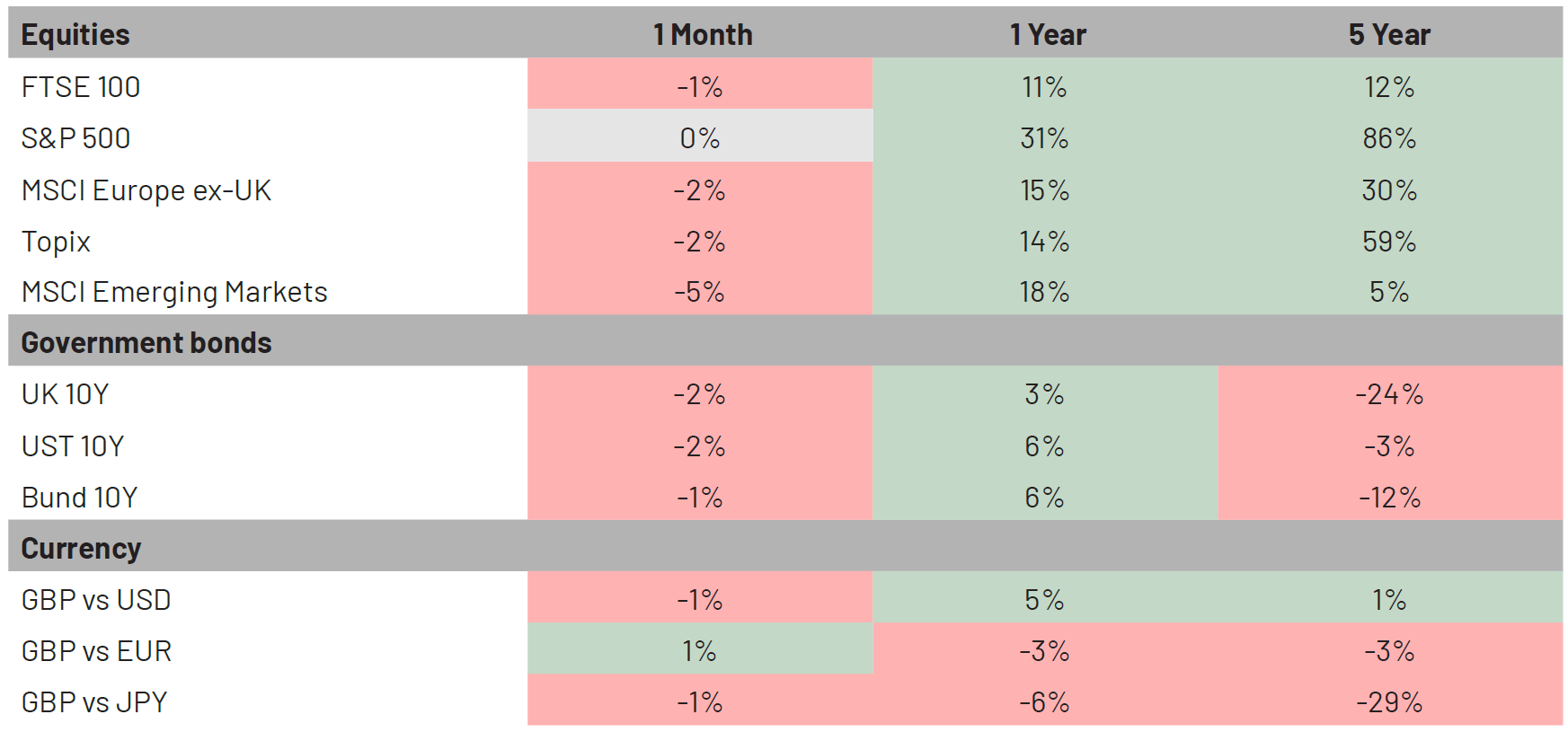

Market Moves

Source: Bloomberg. Data as of 1 November 2024.

What we’re watching in November:

- 5 Nov: US election

- 7 Nov: Bank of England interest rate decision

- 7 Nov: US Federal Reserve interest rate decision

- 13 Nov: US inflation October

- 20 Nov: UK inflation October

You can download the commentary as a PDF here.