Don't forget to remember

Humans are guilty of many things, and forgetting is something we are all guilty of from time to time. The upshot of being forgetful can vary greatly, depending on context.

In 1999, NASA lost a $125 million Mars orbiter because some engineers forgot to convert imperial units to metric units. This led to a serious miscalculation of the spacecraft's trajectory, and it ultimately burned up in the Martian atmosphere.

A more topical example of forgetfulness is that of Silicon Valley Bank. The bank got so used to low rates that they pretty much forgot how to manage their risk for an environment where interest rates soar. André Esteves, co-founder of Brazil’s Banco BGT, sums it up well. He claims that “any junior analyst” from Latin America would have been able to manage the interest rate risk on SVB’s balance sheet.

Not because “SVB were morons and Latin American interns are smart”, but rather because “SVB had 15 years of low and stable interest rates and Latin American interns did not.” Rates in Latin America move around dramatically, so people are used to rates rising and don’t have time to forget that it can happen.

As investors, if we forget about something, that is unlikely to lead to an explosion, but the consequences for portfolios can be just as dire.

What’s under the interest rate bonnet?

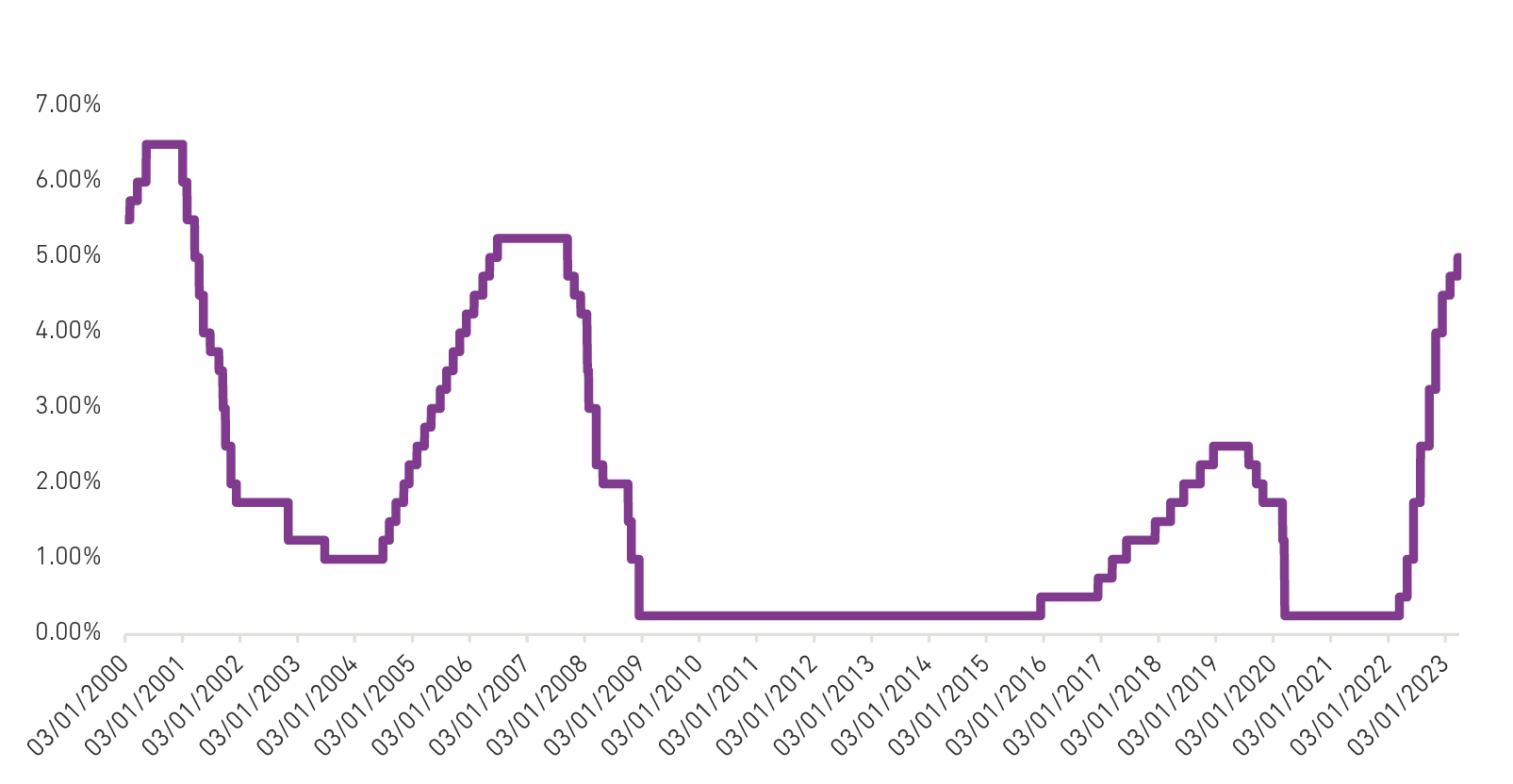

US interest rates have sky-rocketed over the past 12 months:

Fed Fund Rate

Data source: Bloomberg

At face value, you might think that the way interest rates impact the economy is simple. Higher rates mean money is more expensive, so people spend less and economic activity slows down. In reality, the process is much more complicated than that.

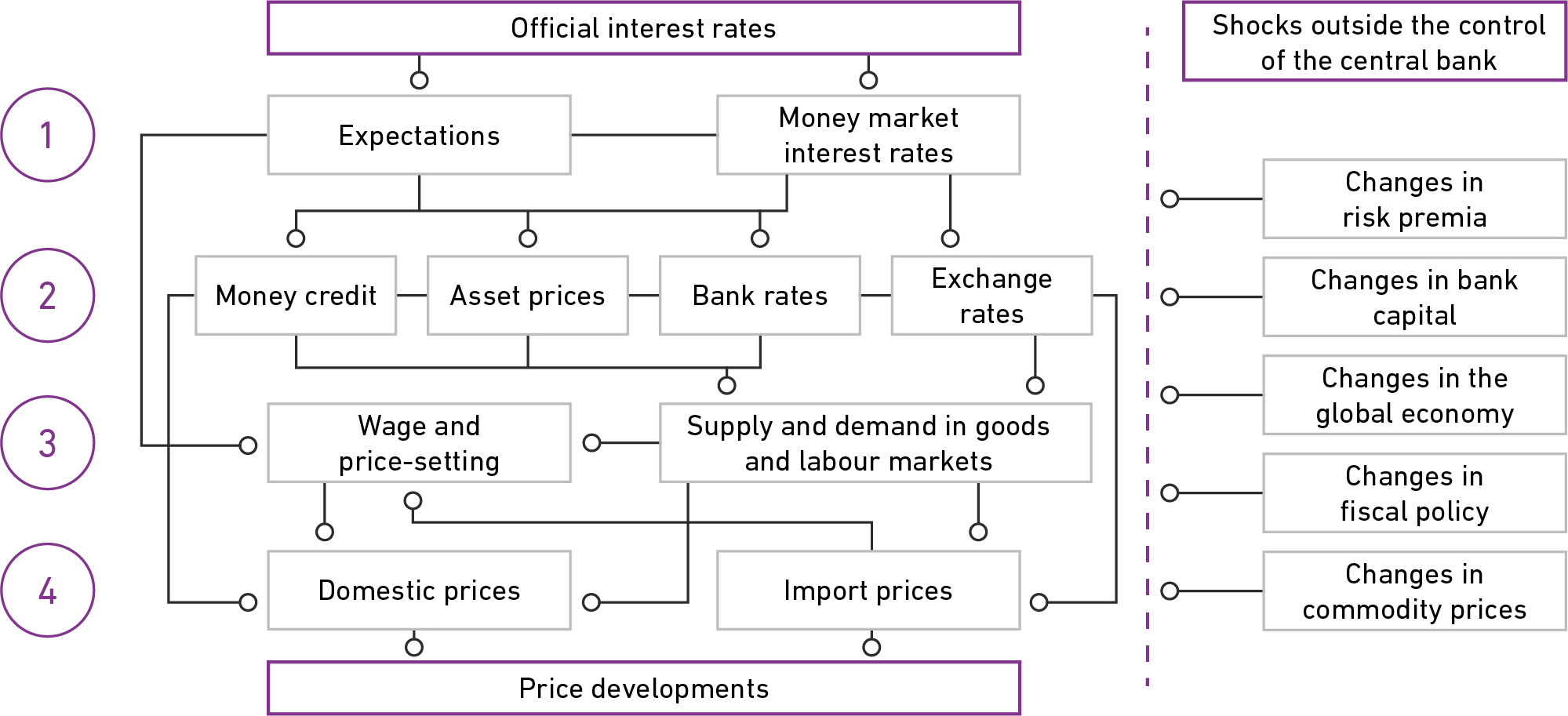

The Transmission Mechanism of Monetary Policy

Other than looking a bit like the London tube map, this flowchart from the European Central Bank highlights the complexity of how central bank rates impact the economy – what economists call the Transmission Mechanism of Monetary Policy:

1. Expectations and money market interest rates adjust quickly.

People stop speculating about the rate rise, because it has been announced, and short-term money market rates adjust pretty much instantly.

2. The impact on the next line down can be quick or slow.

- Asset prices can adjust quickly – discount rates have changed, which can be priced in easily (although this is only the first order effect)

- Bank rates adjust quickly

- Exchange rates will adjust for the change in relative interest rates between countries, which can take time

- The money/credit landscape changes. You pay more on floating rate loans, and you might be less inclined to take out loans that you now have to pay more for.

3. This next line is much slower.

- Wage and price setting takes time. Most people negotiate their salary once a year. So, if your floating rate mortgage payments rise, you might have to wait a year to negotiate a higher salary to cover it. There’s also time and costs associated with your local grocer changing their prices

- Changes in the labour markets can take even longer. The higher cost of capital takes a long time to bite firms and laying off employees to make space for this takes even longer.

4. This next line is just a function of the lines above.

- Domestic prices rely on changes in supply, demand, wages, and (of course) prices

- Import prices are impacted by interest rates.

To complicate things still more, throw in a load of potential exogenous shocks on the right-hand side of this framework that might happen, might not happen, or might all happen at the same time…

What the bulls are forgetting

Hopefully, that diagram will convince you that interest rates don’t impact the economy overnight. If you need more evidence, central banks themselves are the first to say that it takes time for the economy to fully feel the effects of rate rises:

- “Some estimates suggest that it takes between one and two years for monetary policy to have its maximum effect” – Reserve Bank of Australia

- “A large body of research tells us that it can take 18 months to two years or more for tighter monetary policy to materially affect inflation” – Federal Reserve Bank of Atlanta

As you can see from the chart, US rate hikes have only been going on for a year and are still happening. It will take a while yet for the economy to feel the full effect of these hikes.

The current hiking cycle has already pushed over a few dominoes. US inflation has started to tick down, some poorly risk-managed banks couldn’t keep up with outflows, and Credit Suisse – a non-profitable and reputationally damaged bank – was pushed over the edge by a combination of factors.

More dominoes will fall

The interest rate rises are still having their impact and more needs to happen for them to have their full desired effect on the economy – returning inflation to target levels. The domino that tends to precede inflation is unemployment. When unemployment rises, it’s harder for workers to negotiate higher wages, and the upwards pressure on prices subsides. US unemployment hasn’t really budged yet. It’s hovering around 3.5%, which is a historically low level.

We believe that markets got overexcited about not very much at the start of the year. A couple of cracks have appeared, but the global economy has not felt the full impact of rate rises – this is yet to come. In this kind of environment, equity markets are unlikely to perform well.

At this point in the cycle, being fickle and forgetting the past are especially dangerous. An investor with a short memory might be moving overweight equity because markets have rallied year to date, all the while forgetting that dramatic interest rate rises have happened and will take more time to feed through to the economy.

That is why we remain underweight equity risk. We believe that markets got overexcited about not very much at the start of the year. A couple of cracks have appeared, but the global economy has not felt the full impact of rate rises – this is yet to come. In this kind of environment, equity markets are unlikely to perform well. For us to change our core view, many more adjustments need to take place.

Find out more