Interest rates – neither up nor down

By the time you’re reading this it’ll probably be time for Nursery Rhyme Week, the biggest date in the calendar for parents with young kids.

It’s not often we start an investment view around old nursery rhymes. But it’s hard not to think of the Grand Old Duke of York when contemplating monetary policy. The apparent meaning of the rhyme was to express the futility of military action. And as we embark on a new cutting cycle, there are questions over the effects of monetary policy. The Bank of England spent almost two years climbing the interest rate hill, spent a year atop and looks to be marching interest rates back down again.

And for what? By the end of next year, interest rates will be back to where they were in December 2022. Were the set of hikes up to 5.25% necessary? Did holding interest rates at 5.25% for almost a year make any difference? Was any of it required?

These questions are crucial for cautious clients. The actions of global central banks have had material impacts on their short-term performance. As interest rates rise, bond prices fall. And Cautious portfolios hold bonds which during 2022 meant that as interest rates went up by more than expected, portfolio values were impacted by more than expected.

1. For years, there was no hill in sight

Not that long ago that rates were close to zero, and it felt like we’d be there for a long time. Since the 2008 financial crisis, the economy had been in repair mode. The result was that the factors that traditionally drove inflation were pushing it down. Consumer confidence was

low holding down prices. House prices were stable compared to the buying frenzy of the early noughties. Global trade was still flowing smoothly. Commodity prices had not just fallen but crashed. And governments kept a lid on their own spending. Together, these factors kept interest rates low. And it looked like each of each of these factors would stay as they were. Surely, there was nothing on the horizon that would reverse any of these factors?

2. Covid turned the hill into a mountain

And then Covid. Not only did one or two factors reverse, but they all did. Consumers suddenly found themselves with deep pockets following the initial lockdown and proceeded to spend

on anything, on everything, pushing up prices everywhere. The lockdowns drove a new frenzy of homebuying as those living in cities suddenly found the need for a study and a garden. At the same time, lockdowns shut down factories across the world stymying global trade putting up the price of goods in short supply. Despite the price of oil moving temporarily negative, prices climbed higher culminating in the surge around the Russia invasion of Ukraine. All the while governments spent record amounts of taxpayers’ money on bailing out economies they thought would be in indefinite lockdowns.

One factor, by itself, will have been enough to push prices higher. But each of these factors came, one after the other, pushing prices higher and higher. And so, up the interest rate hill we went.

3. It felt like we’d never come down

The effect of so many things happening at the same time gave the impression that this was structural, or even permanent. Fear of a 1970s-style wage/price spiral gripped investors. There was talk of central banks changing their inflation targets from 2% to something higher (the economists’ way of saying higher inflation might be permanent). And some had just resigned themselves to higher rates – after all, we managed it in the 90s.

But this isn’t the 90s. The idea that we’ve gone from near zero to near five overnight is not realistic. Some of the factors on the list might have changed somewhat, the trade war between US and China is ongoing while commodity prices have a long-term carbon transition tailwind. However, wherever interest rates land over the next few years, it’s unlikely we need to stay on top of the hill forever.

The Bank of England (BoE) thinks so too, feeling confident that it can start reducing interest rates even with inflation above 2%.

We started the descent in August and are looking to move down towards 3.5% by the end of 2025. What does this mean for investors? Well, the last year has shown why cash is such a suboptimal investment.

4. Investors like being ‘neither up nor down’

We started the descent in August and are looking to move down towards 3.5% by the end of 2025. What does this mean for investors? Well, the last year has shown why cash is such a suboptimal investment. The temptation is to hold cash given it has risen to a generational high, sit it out until it comes back down and then rotate into other investments.

The flaw in this logic is that markets aren’t waiting for you to get back in. Apart from fleeting moments of panic, investors are better placed to allocate their capital to investments that are designed to deliver returns above cash. Government bonds, corporate bonds and equities amongst others. These assets are pricing in moves in cash rates before they happen. To illustrate this, look at UK and US long-term bonds the year leading up to the first rate cut by each central bank. US bond yields fell by 1.3% from their highs and UK bond yields fell 0.7%. Remember bond prices move in the opposite direction to yields. So, investors who chose to sit in cash rather than invest have missed out on substantial capital returns.

We wouldn’t advocate just investing in one asset, but rather a blend of assets that align with your risk tolerances. Take the AAP Moderately Cautious, which contains a mix of bonds and equities. It returned 9.89% in the year leading up to the first BoE rate cut. That’s almost double what a cash investor could have received. It’s not surprising that a blend of assets designed to beat cash, did beat cash.

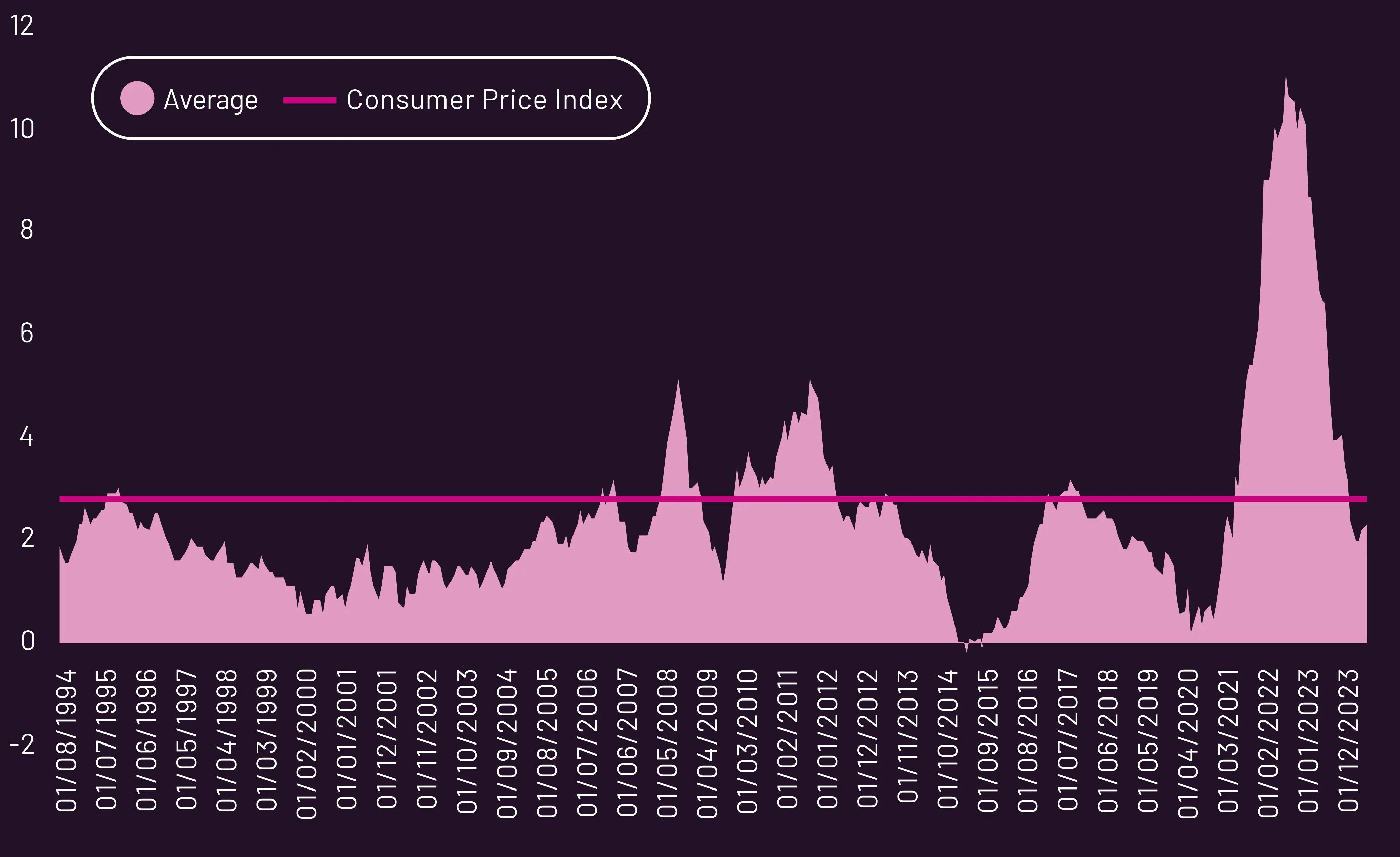

Inflation returning back to long-run average

An extraordinary set of forces conspired to push inflation higher post-Covid. During lockdowns, consumers spent most of their income on goods. Those same lockdowns stymied the flow of global trade. Together these pushed prices higher. House prices rose by double digits. Commodity prices surged. And government stimulus hit record levels. This pushed inflation towards double digits. But two years later, we are now back to long-term averages. The question is how far will the BoE cut interest rates? Whatever the answer, investors shouldn’t wait to find out. Those holding cash should consider rotating into investments instead.

UK Consumer Price Index (CPI) vs Average

Source: Office for National Statistics

More from 7IM