Monthly commentary

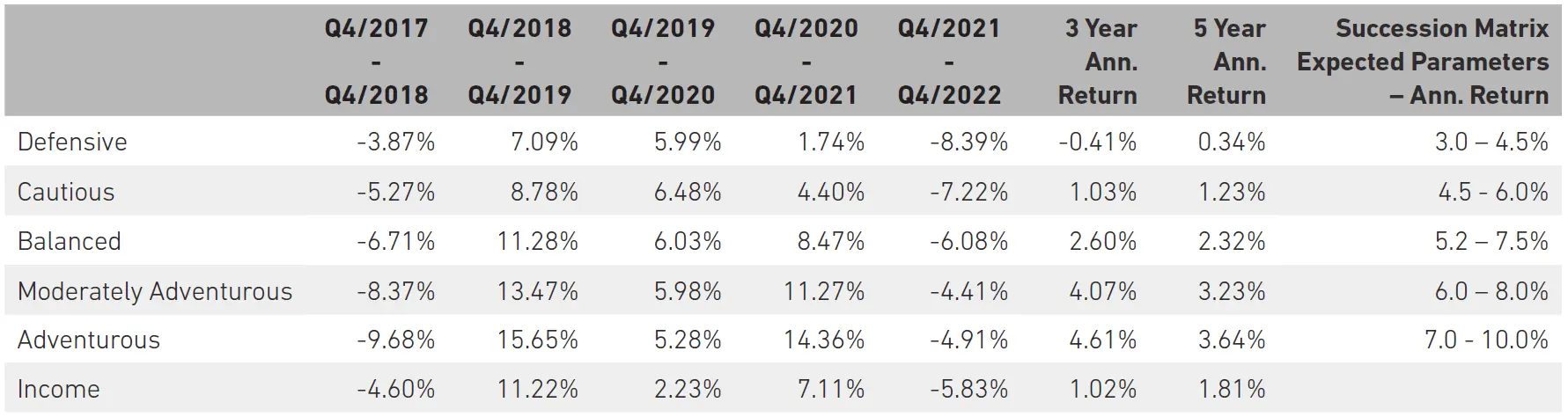

Portfolio Performance

At 7IM, we believe that taking a long-term view is essential when investing. We can’t always avoid the short-term bumps and shocks that the financial world has in store, but a well-diversified portfolio goes a long way towards smoothing out some of the journey. The long-term nature of our strategic and tactical process is a good complement to the Succession Matrix Expected Parameters.

Source: 7IM/FE. Annualised return is defined as ‘Ann. Return’ in the performance table above and is as at end December 2022. Market returns have been poor in absolute terms since the beginning of 2020 with the Covid pandemic and then the inflationary shock of 2022. While portfolios have held up well relative to peers, the 3 and 5 year absolute returns are lower than average, even though the since inception longer term numbers are in line with expected parameters..

Summary

Tough times teach investors lessons. Here are a few of the things we believe multi-asset investors should take away from 2022:

1. Diversification really is the only free lunch

The opening phrase of most 2022 market commentaries will be something along the lines of: “Over the year, global stocks have fallen around 20% and global bonds have fallen by around 15%”1.

So, if 2022 has been the year where seemingly everything goes down, why am I talking about diversification being a free lunch?

It is because, while it is true that 2022 was the worst year for the 60/40 portfolio since the Great Depression, this does not fully depict what the year has been like for a genuinely diversified multi-asset portfolio. Bonds and equities are not the only tools at our disposal.

Genuine alternatives should be a key part of any portfolio that claims to be diversified, but you hardly ever hear about them in ‘Year in review’ commentaries. This is because alternatives are very hard to index. The strategies available are hugely idiosyncratic and often quite complex, so turning them into an index isn’t really that helpful – the combined performance of a long-short stock picker, and a quant hedge fund doesn’t really tell you anything.

In our portfolios, we use alternatives to diversify away from equity and bond exposures. In 2022 when equities and bonds have suffered, our alternatives allocation has served us very well and we believe that they are a necessary ingredient in a well-diversified portfolio.

2. Nothing lasts forever

In the years leading up to 2022, it really felt like growth/tech stocks only ever go up. 2022 showed us that this is not the case.

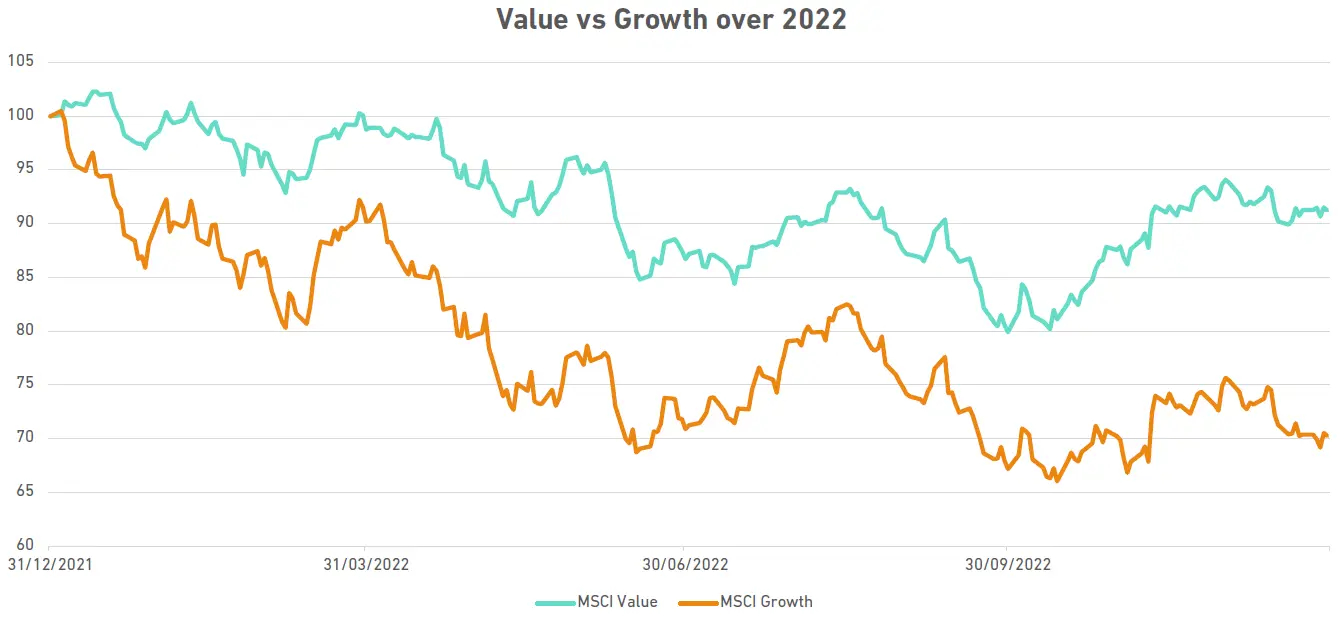

My favourite example of this is looking at value vs growth. The chart below shows the MSCI growth and value returns for investing £100 in the five years running up to 2022:

Source: Bloomberg Finance L.P.

Over this time period, growth trounced value as big tech took to the skies. If you also had £100 and were new to investing in 2022, you might think – ‘growth always does well, I’m going to put my money into that.’

The next chart shows the return from investing £100 in the same indices over 2022:

Source: Bloomberg Finance L.P.

Although it lost in absolute terms, value outperformed growth by over 20% in just one year. Trends that once seemed unbreakable – crypto, ARK, Chinese growth, falling interest rates, etc. - … eventually break.

As multi-asset investors, you shouldn’t hold the same view forever. The world changes, the economy reaches a new stage in a cycle, and the assets that are in favour will switch.

3. Beware of predictions

Around the start of each year, all the big investment banks and buy-side firms cast their predictions about the year ahead.

A lot of these places will have reams of PhDs and CFAs working tirelessly to build the best expected returns framework in the business. So surely, they are pretty good at predicting what will happen? …NO!

Let’s look at where they thought the S&P would end 2022, at the time of writing their year ahead predictions at the end of 2021:

| Bank | 2022 S&P year-end prediction |

|---|---|

| Goldman Sachs | 5,100 |

| J.P. Morgan | 5,050 |

| Morgan Stanley | 4,400 |

| Bank of America | 4,600 |

| Citi | 4,900 |

| Barclays | 4,800 |

| Credit Suisse | 5,200 |

| Deutsche Bank | 5,250 |

| RBC | 5,050 |

Source: Eddie Domnez LinkedIn

The S&P actually ended 2022 at 3,839.50.

You might be thinking, ‘2022 was a really tough year with surprises around every corner.’ This is true, but even if you use longer time periods, Wall Street’s track record is still terrible, and studies confirm this.2

Predicting what is going to happen in markets is extremely hard. When they wrote each of their predictions, Wall Street probably made highly reasonable assumptions given the data they had… but the world changes in highly unpredictable ways.

Portfolio Positioning and Changes

During December. No changes were made to our model portfolios. they will be rebalanced in November in line with our quarterly rebalancing schedule.

Core views

At 7IM, we have a number of long-term core views that help to guide our investment decisions and allocations within portfolios.

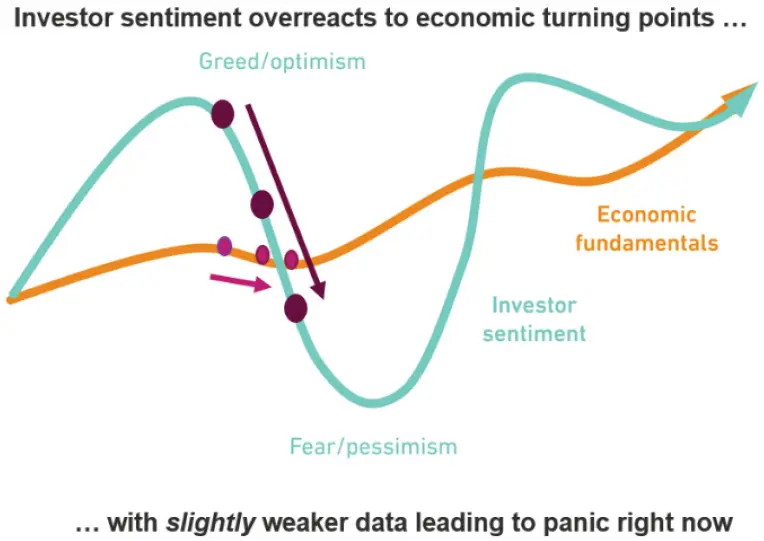

Over the next twelve months, we think markets will generally move sideways with volatility. In this environment, it is important to rely on a stable identity. Economic uncertainty creates fear and investor sentiment tends to overreact to economic turning points. Going forward, we believe that:

- Inflation will come down. Goods inflation is slowly normalising, and supply chain pressures are easing.

- Central banks are getting close to the end of their hiking cycles, but there is still a bit more work to do.

- A US recession is highly likely. Most leading indicators point towards a recession, but the recession shouldn’t be too long or deep.

And so, investors are starting to worry about what’s next for financial markets. Economic data isn’t likely to stabilise until next year, so ‘Sideways with volatility’ is the most likely scenario for the next few months.

We know our investment identity helps us to deliver in just these kinds of environments. We have positions that can generate returns despite this volatile backdrop.

Source: 7IM

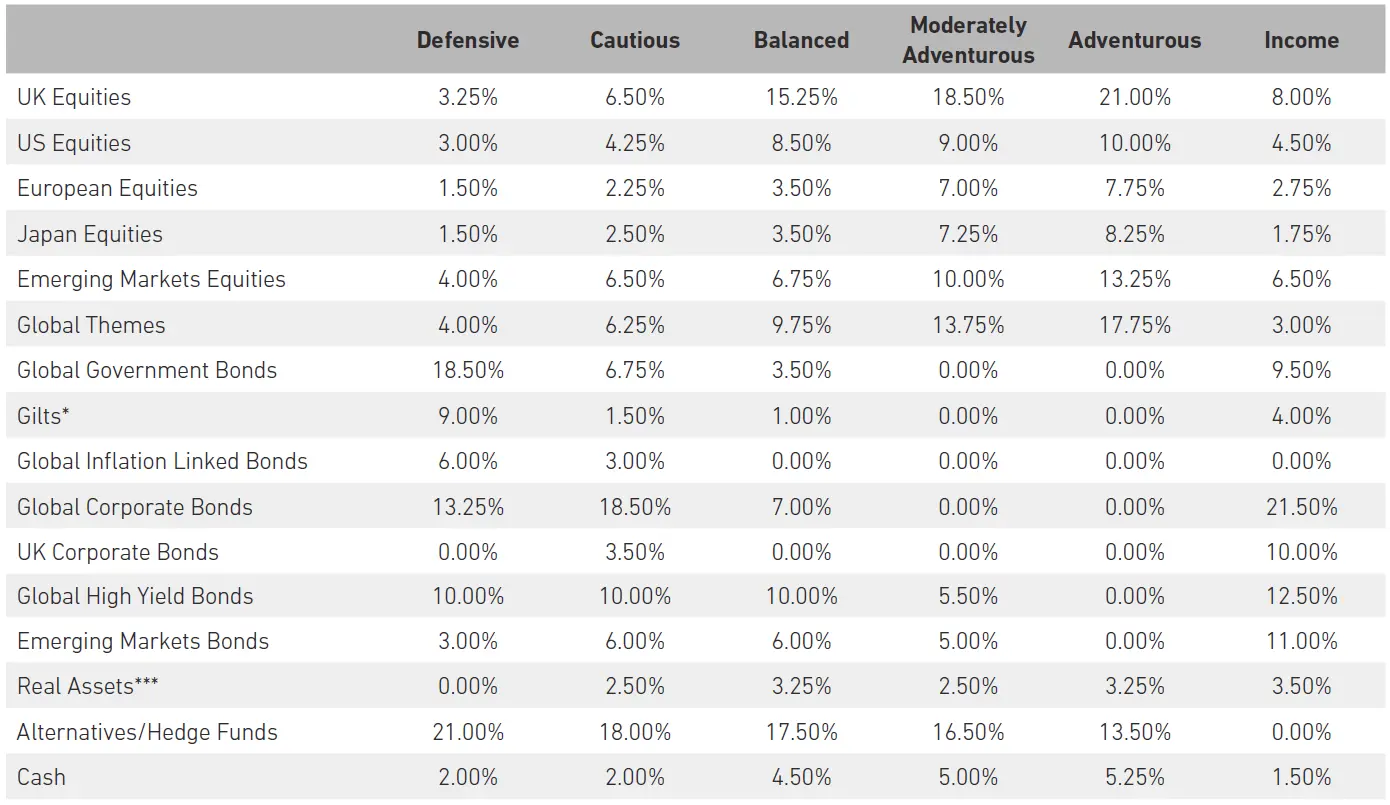

Asset Allocation

Detailed asset allocation

Source: 7IM. *Includes Short Term Sterling Bonds **Includes Convertible Bonds ***Includes Infrastructure

1 Bloomberg Finance L.P.

2 https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4184885

Read more from 7IM

You can download the commentary as a PDF here.