Monthly commentary

Portfolio Performance

At 7IM, we believe that taking a long-term view is essential when investing. We can’t always avoid the short-term bumps and shocks that the financial world has in store, but a well-diversified portfolio goes a long way towards smoothing out some of the journey. The long-term nature of our strategic and tactical process is a good complement to the Succession Matrix Expected Parameters.

| Q1/2018 - Q1/2019 | Q1/2019 - Q1/2020 | Q1/2020 - Q1/2021 | Q1/2021 - Q1/2022 | Q1/2022 - Q1/2023 | 3 Year Ann. Return | 5 Year Ann. Return | Succession Matrix Expected Parameters – Ann. Return | |

|---|---|---|---|---|---|---|---|---|

| Defensive | 1.35% | -0.77% | 9.27% | 0.75% | -5.37% | 1.37% | 0.93% | 3.0 - 4.5% |

| Cautious | 0.71% | -2.54% | 13.96% | 2.41% | -4.47% | 3.69% | 1.82% | 4.5 - 6.0% |

| Balanced | 1.20% | -5.05% | 19.83% | 4.45% | -3.23% | 6.60% | 3.08% | 5.2 - 7.5% |

| Moderately Adventurous | 1.13% | -8.14% | 26.06% | 6.32% | -1.56% | 9.68% | 4.15% | 6.0 - 8.0% |

| Adventurous | 1.63% | -10.58% | 30.79% | 7.86% | -1.42% | 11.62% | 4.79% | 7.0 - 10.0% |

| Income | 3.28% | -8.68% | 18.97% | 4.16% | -3.28% | 6.22% | 2.48% |

Source: 7IM/FE. Annualised return is defined as ‘Ann. Return’ in the performance table above and is as at end March 2023. Market returns have been poor in absolute terms since the beginning of 2020 with the Covid pandemic and then the inflationary shock of 2022. While portfolios have held up well relative to peers, the three and five year absolute returns are lower than average, even though the since inception longer term numbers are in line with expected parameters.

Summary

There are decades where nothing happens; and there are weeks where decades happen

Back when Lenin said this in the early 20th century, I don’t think he had any idea about Silicon Valley Bank or Credit Suisse merging with UBS in 100 years’ time, but the message fits the past month (and past quarter) to a tee.

In isolation, the whole Credit Suisse situation feels a bit like a butterfly causing a hurricane, with SVB being the butterfly and Swiss banks being the ones caught up in the hurricane. In reality, a lot has been going on for far longer than just the month of March that resulted in the recent banking scares.

For example, here’s the list of scandals which Credit Suisse has found itself navigating over the last few years:

- In 2018, Patrice Lescaudron, a former CS banker, was sentenced to 5 years for forging client signatures to divert client money to make stock bets resulting in $150 million in losses

- In 2018, CS paid $47 million to US authorities over a ‘corruption scheme’ where the bank tried to win business by offering jobs to family and friends of Chinese officials

- In 2019, the bank was involved in a corporate espionage scandal and admitted to hiring private detectives to track two outgoing executives. A further five cases of this were found upon further investigation

- In 2020, an indictment against CS was issued for not running proper checks on clients as a Bulgarian drug ring laundered around $150 million through the bank’s accounts between 2004 and 2008

- In 2021, CS lost $5.5 billion on account of its exposure to the Archegos Capital Management hedge fund

- In 2021, CS suspended $10 billion of investor funds due to exposure to loans from collapsed supply-chain lender, Greensill.

- In 2021, CS was fined £350 million to pay for their long-term involvement in Mozambique’s “tuna bond” bribery scandal, which played a significant part in pushing the country into a financial crisis.

All of this resulted in Credit Suisse being the one to watch out of the big global banks. Pile on top of this the fact that Credit Suisse wasn’t profitable in 2022, and you have yourself a bank with more than a few reputational wrinkles. As a bank, reputation is everything. As Walter Bagehot said once, “Every banker knows that if he has to prove that he is worthy of credit, however good may be his arguments, in fact his credit is gone”.

Fast forward to March, and more straws get loaded onto Credit Suisse’s already reputationally weary back. ‘Material Weaknesses’ were found in the banks reporting, and then Saudi National Bank – Credit Suisse’s top investor – announced that it would not be providing any more cash. It was at this point that the banks shares really went into freefall and Swiss authorities realised that they needed to do something.

Swiss Authorities stepped in, and Credit Suisse announced that it would borrow 54 billion Francs from the Swiss National Bank. After an initial share price pop, it became clear that this was not going to be enough, and the Swiss government brokered a deal whereby UBS would buy Credit Suisse for $3.2 billion. The bank founded over 160 years ago is no more.

In America, something seemingly pretty detached from Europe had been going on in the months running up to the UBS/Credit Suisse deal. Here’s a potted version of what went on and why:

A highly specialised US bank mismanaging its balance sheet risk shouldn’t be too related to a Swiss bank with a bad reputation, but it’s possible that the fear SVB’s collapse caused was contagious.

Just prior to the forced deal, Credit Suisse looked a long way from default judging by most metrics analysts look at – it was an A-rated issuer! And it’s impossible to say for sure whether the Credit Suisse situation would have happened if this hadn’t gone on in America, but if you put enough straws on any animal’s back – whether it be a mouse, camel, or elephant – it will eventually break.

Portfolio Positioning and Changes

During March, we made the following changes to portfolios:

- Began reducing AT1 bonds to their new target weight. The asset class has struggled on account of the stress in the European Banking sector. We believe that it is prudent risk management to downsize the positions and have been carefully reducing the allocation in tranches.

- Added to our climate change position. This is a trade that we have strong conviction in, and we believe that now is an opportune time to add.

Core views

At 7IM, we have a number of long-term core views that help to guide our investment decisions and allocations within portfolios.

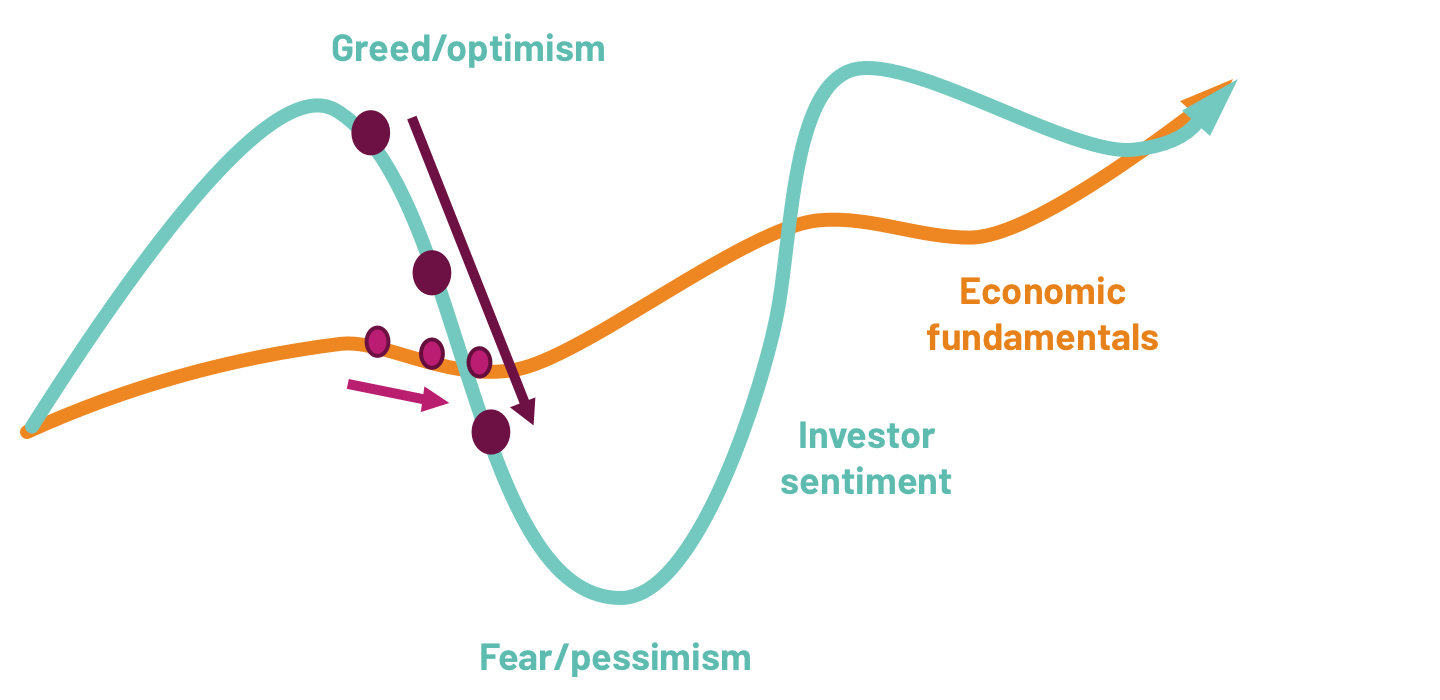

Over the next 12 months, we think markets will generally move sideways with volatility. In this environment, it is important to rely on a stable identity. Economic uncertainty creates fear and investor sentiment tends to overreact to economic turning points. Going forward, we believe that:

- Inflation will come down. Goods inflation is slowly normalising, and supply chain pressures are easing.

- Central banks are getting close to the end of their hiking cycles, but there is still a bit more work to do.

- A US recession is highly likely. Most leading indicators point towards a recession, but the recession shouldn’t be too long or deep.

Investor sentiment overreacts to economic turning points …

… with slightly weaker data leading to panic right now

Source: 7IM

And so, investors are starting to worry about what’s next for financial markets. Economic data isn’t likely to stabilise until next year, so ‘Sideways with volatility’ is the most likely scenario for the next few months.

We know our investment identity helps us to deliver in just these kinds of environments. We have positions that can generate returns despite this volatile backdrop.

Asset allocation

Detailed asset allocation

| Defensive | Cautious | Balanced | Moderately Adventurous | Adventurous | Income | |

|---|---|---|---|---|---|---|

| UK Equities | 4.50% | 6.50% | 15.00% | 18.25% | 26.00% | 8.75% |

| US Equities | 4.00% | 5.75% | 11.00% | 12.25% | 25.00% | 7.75% |

| European Equities | 2.00% | 2.50% | 3.25% | 6.25% | 11.00% | 3.00% |

| Japan Equities | 2.25% | 2.75% | 4.00% | 6.75% | 11.00% | 2.50% |

| Emerging Markets Equities | 1.75% | 2.75% | 2.50% | 5.25% | 11.00% | 2.50% |

| Global Themes | 3.50% | 6.00% | 9.50% | 13.00% | 0.00% | 4.00% |

| Global Government Bonds | 24.00% | 11.50% | 8.50% | 0.00% | 0.00% | 11.00% |

| Gilts* | 11.00% | 3.00% | 2.50% | 0.00% | 0.00% | 6.00% |

| UK Corporate Bonds | 5.00% | 8.50% | 5.00% | 0.00% | 0.00% | 10.00% |

| Global Corporate Bonds** | 9.25% | 14.25% | 4.00% | 0.00% | 0.00% | 18.75% |

| Global High Yield Bonds | 10.00% | 10.00% | 10.00% | 8.50% | 0.00% | 12.50% |

| Emerging Markets Bonds | 3.00% | 6.00% | 6.00% | 5.00% | 3.00% | 11.00% |

| Global Inflation Linked Bonds | 6.00% | 3.00% | 0.00% | 0.00% | 0.00% | 0.00% |

| Real Assets*** | 0.00% | 3.25% | 3.25% | 2.75% | 5.00% | 4.50% |

| Alternatives/Hedge Funds | 17.50% | 16.00% | 15.00% | 14.50% | 6.00% | 0.00% |

| Cash | -3.75% | -1.75% | 0.50% | 7.50% | 2.00% | -2.25% |

Source: 7IM. *Includes Short Term Sterling Bonds **Includes Convertible Bonds ***Includes Infrastructure

You can download the commentary as a PDF here.