Credit Suisse Update

When an economic slowdown is on the go, and in particular, driven by interest rate rises, these things happen. In times like these, be prepared to be unsurprised by surprises.

In a nutshell

The markets have become worried that Credit Suisse could be the ‘next’ SVB. But the banks couldn’t be more different. The Swiss bank is fundamentally sound and subject to regular stress tests by its regulators. There is a danger that the worry becomes a self-fulfilling prophecy. Clients pull their money because they’re worried other clients are going to pull their money. So far, the Swiss Central Bank has intervened to stabilise the situation. This should be enough, but we monitor closely. In terms of portfolios, our exposures to Credit Suisse at a portfolio level are around 0.6%, through our European bank debt position. This is small in absolute terms (similar to the exposure to Russia in February 2022), as multi-asset portfolios are designed for these situations. This does not change our outlook or positioning but, in fact, reinforces our view that sideways and volatile markets will persist for some time.

What’s happening with Credit Suisse?

Yesterday Credit Suisse equities sold off by over 20%, while its Credit Default Swap approached levels that suggested a default was imminent. These kind of market moves bring back visceral memories of 2008. Back then, we saw a mortgage bubble, on top of poor lending standards, on top of low regulatory scrutiny, on top of risky derivatives, on top of ‘off-balance’ sheet activities, on top of low capital protection.

But today is very different to the financial crisis. Lending is much safer; regulators scrutinise balance sheets to within an inch of their lives, while banks worldwide are forced to hold enough capital against the loans they make to withstand events two or three times as bad as the financial crisis.

This doesn’t stop the market from panicking, though. At the heart of the issue is that Credit Suisse is not a very profitable business and has been run poorly for a long time. Over the years, there have been numerous low-level scandals, fines and regulatory breaches – symptoms of poor governance and weak leadership. So just a few days after a US bank went under, the markets are asking if there is something more sinister happening at Credit Suisse. The truth is, we shouldn’t confuse a poorly-run business with a risky or failing business. It might not be making much money, but it still does actually make money. The regulators apply stress tests every year, and Credit Suisse passes with flying colours.

What is needed, then, isn’t a bailout but better management and time. To that end, the whole executive team has changed completely in the last two years. Other than the company secretary, the longest-serving executive is the CEO of the Swiss Bank, at 3 years. The importance of this cannot be overstated. New management has no vested interest in maintaining things as they are, so there has been a wholesale reassessment of the group and its strategy over the last 12 months – acknowledging the weaknesses the market is now panicking about. This isn’t new news. Finally, the Swiss National Bank stepped in last night to confirm any liquidity assistance, which should buy Credit Suisse time. As things stand, the market looks to have got ahead of itself on this issue, and things could start improving soon. We continue to watch this closely.

Have this week’s events changed 7IM’s outlook?

It’s been a challenging time for investors. There has been some good news – US inflation is falling, albeit slowly. We think this trend is going to continue with inflation heading closer to the Federal Reserve’s 2% inflation target, perhaps next year. This means, central banks should be nearly done with raising interest rates.

And about time too. The pace of interest rates has been breathtaking. In the US, we’ve gone from 0.25% to almost 5% in less than a year. With inflation starting to fall, the central banks will have room to breathe and may even start cutting by the end of next year (2024).

But that doesn’t mean smooth sailing ahead. To bring inflation down, central banks need to engineer an economic slowdown, or perhaps a recession. But engineering a slowdown is far from easy and often comes with surprises. You could say those surprises are … unsurprising. We are seeing some now. Did anyone envisage SVB going under? No. Or that the market would ‘target’ Credit Suisse? No. But when an economic slowdown is on the go, and in particular, driven by interest rate rises, these things happen. In times like these, be prepared to be unsurprised by surprises.

As things stand, we continue to expect central bank actions to slow down the US and Europe economies and be reactive to problems that arise, just like we’ve seen in the last week. The authorities aim to step on the brakes but also to avoid anyone going through the windshield.

How are portfolios positioned?

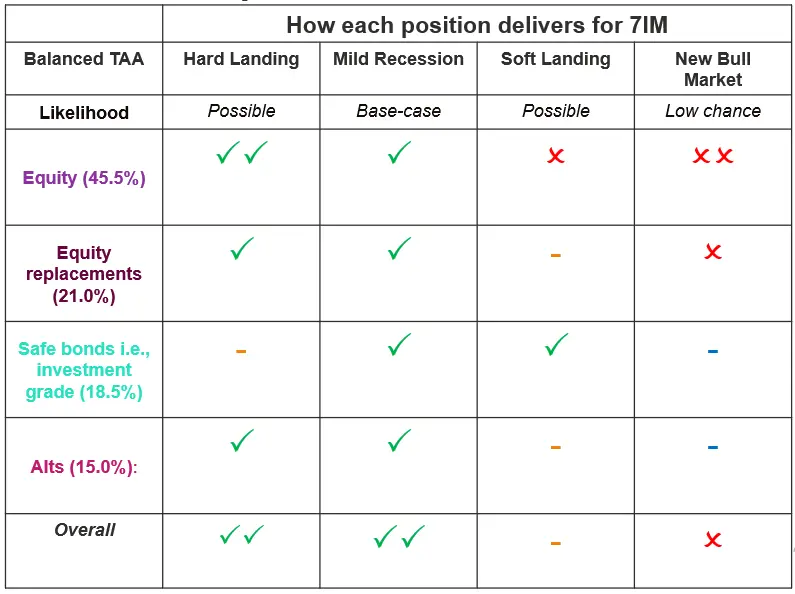

This year the market has gone from pricing an extra 1% hike in US interest rates by December to pricing in 1% of cuts. The stronger-than-expected data from the start of the year raised expectations of a ‘No-Landing’, but this week markets seem worried about a re-run of 2008. European banks’ stocks rallied almost 15% this year before giving it all back in the last week. Markets are leaping from extreme optimism to extreme pessimism very quickly, leading to a sideways with volatility environment. We have been positioned for these kinds of outcomes for a while now: underweight equities, overweight safe bonds and maintaining our alternatives allocation.

The intervention from the Swiss authorities overnight was welcome, and the situation is fluid, so we will continue to keep you updated. As for 7IM exposures to Credit Suisse, they are below. We run globally diversified portfolios, so we will always make sure exposure to any one company remains limited.

| Cautious | Moderately Cautious |

Balanced | Moderately Adventurous |

Adventurous | |

|---|---|---|---|---|---|

| Credit Suisse exposure | 0.6% | 0.6% | 0.6% | 0.5% | 0.3% |

Discover more

You can download the article as a PDF here.