Monthly commentary

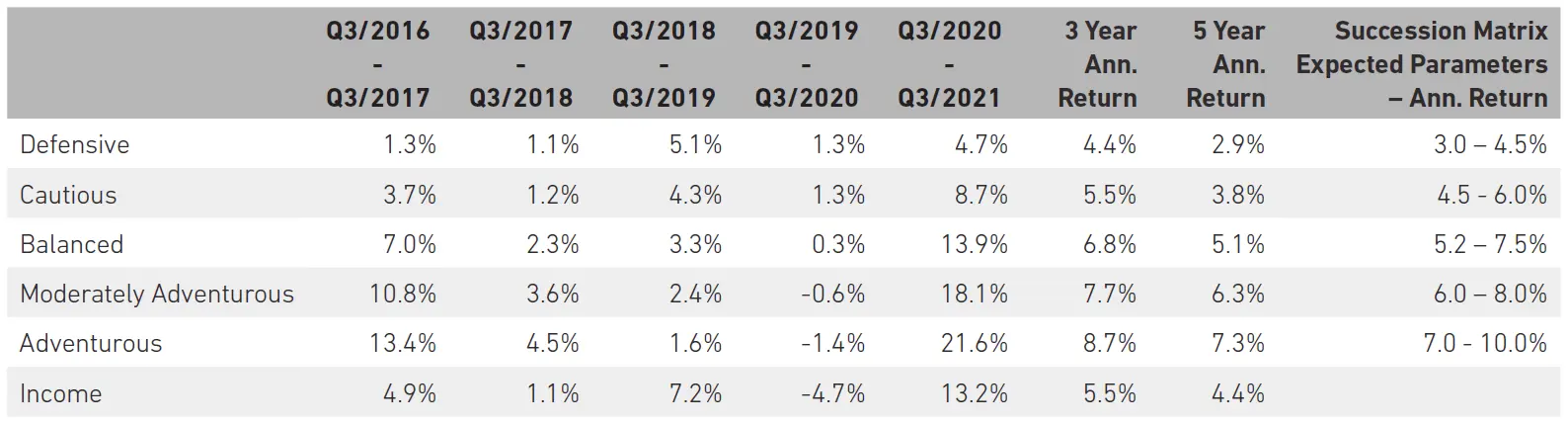

Portfolio Performance

At 7IM, we believe that taking a long-term view is essential when investing. We can’t always avoid the short-term bumps and shocks that the financial world has in store, but a well-diversified portfolio goes a long way towards smoothing out some of the journey. The long-term nature of our strategic and tactical process is a good complement to the Succession Matrix Expected Parameters.

Source: 7IM/FE. Annualised return is defined as ‘Ann. Return’ in the performance table above and is as at end November 2021. The extreme COVID-19 related drawdown at the start of 2020 means performance should continue be viewed with caution. Portfolios are towards the lower end of their ranges for the five-year returns, with the more defensive end struggling a little in the face of low interest rates.

Market and portfolio review

Towards the end of November, it has been impossible to avoid endless headlines about the Omicron variant. Investors took the news very negatively and markets sold off. As 2020 demonstrated, markets (and the press) tend to overreact to Covid-19, and the most recent sell off is likely to be just that, an overreaction; so we’re not too worried.

Almost every scientific and medical authority is saying that it’s too early to draw conclusions about whether this variant is going to cause a significant problem. Within a few weeks, we should know more about the variant – and how effective existing vaccines are in protecting against it. Compared to this time last year, our communal immune systems are in a far more robust state – we know infinitely more about the disease and how to deal with it.

Despite this, scare stories have crept in as a number of countries have taken preventative action. We view this as broadly a pragmatic, stitch-in-time-saves-nine approach. Limiting flights and increasing testing is sensible, and improves the data collection. Avoiding lockdowns is still the priority of most Western governments.

As we’ve said before, our portfolios are all-weather and shouldn’t need changing very often. We remain happy with our neutral equity exposure and, if markets have overreacted, we expect our cyclical tilts to outperform as investors see the positive economic growth that we believe will take place over the next few years.

In other news, Joe Biden has chosen to renominate J Powell as Chair of the Federal Reserve over Lael Brainard. This suggests that Biden favours a slightly less dovish approach and is perhaps more willing to tackle inflation than previously thought. With his renomination, Powell says that he is retiring the word “transitory”, suggesting that actions may need to be taken to manage the potential persistence of higher inflation. Our view is still that inflation will not be a major obstacle for growth going forward – although will likely average at a higher level than the last decade.

After a monumental 16 years as chancellor of Germany, Angela Merkel’s successor has been chosen. The man to follow in her footsteps is Social Democrat, Olaf Sholz, who has made a promise to deliver the “biggest industrial modernisation of Germany in more than 100 years”. Despite this, his first big moves will be in tackling Covid, where he is promoting mandatory vaccines by February.

Portfolio positioning and changes

During November, we rebalanced the Succession model portfolios and made two changes:

Since we went overweight equities in the models in August 2020, equity markets are up just under 40%. Hence, this quarter, we have decided to take our profits from our overweight equity position and return to neutral, resulting in slightly higher cash and alternatives allocations. As our core views suggest, we still believe that the world is well placed for strong economic growth, but this is now being priced in more than it was previously as the strong bull market suggests.

We have also introduced our Asia High Yield position into the adventurous risk profile models by recycling some of our overweight equity profits into the asset class. Our conviction in the asset class is strong, and given the recent issues in the Chinese property sector, we now believe that Asia High Yield is offering returns attractive for an adventurous risk profile.

Core views

A new wave of economic growth… For the past decade or so, the virtuous circle of consumption and investment has just not been able to get going. The scars of the financial crisis were too deep – people bought less while governments reined in spending. As a result, companies kept putting off investing in longer-term projects.

The 2020 recession hit the reset button. People are willing to spend again, while governments have ditched austerity. And so, companies are starting to invest for the future. We are now at the start of a sustained period of growth, fueled by confidence and expansion across all sectors of the global economy.

And a little inflation won’t hurt… Economists tend to dislike thinking about the psychology of inflation, but in a lot of ways, someone’s inflation expectations are a good proxy for their confidence levels. With the right amount of price and wage growth, people are encouraged to make life decisions which are positive for the economy. We haven’t heard the word “Goldilocks” for some years now, but there really is an amount of inflation which is just right to keep things humming.

7IM portfolios are positioned for a changing environment… For this coming growth phase, we believe a more selective exposure will be better than a large overweight to the broad equity market. A more robust consumer-driven cycle will see different winners emerge. Regions and industries which have struggled to attract investors over the past decade are better positioned to capitalise than the huge US tech giants (although there are lots of small US companies which will do well).

We’ve also made sure that our fixed income positioning isn’t unnecessarily exposed to rate rises, using allocations to alternatives and to non-mainstream asset classes.

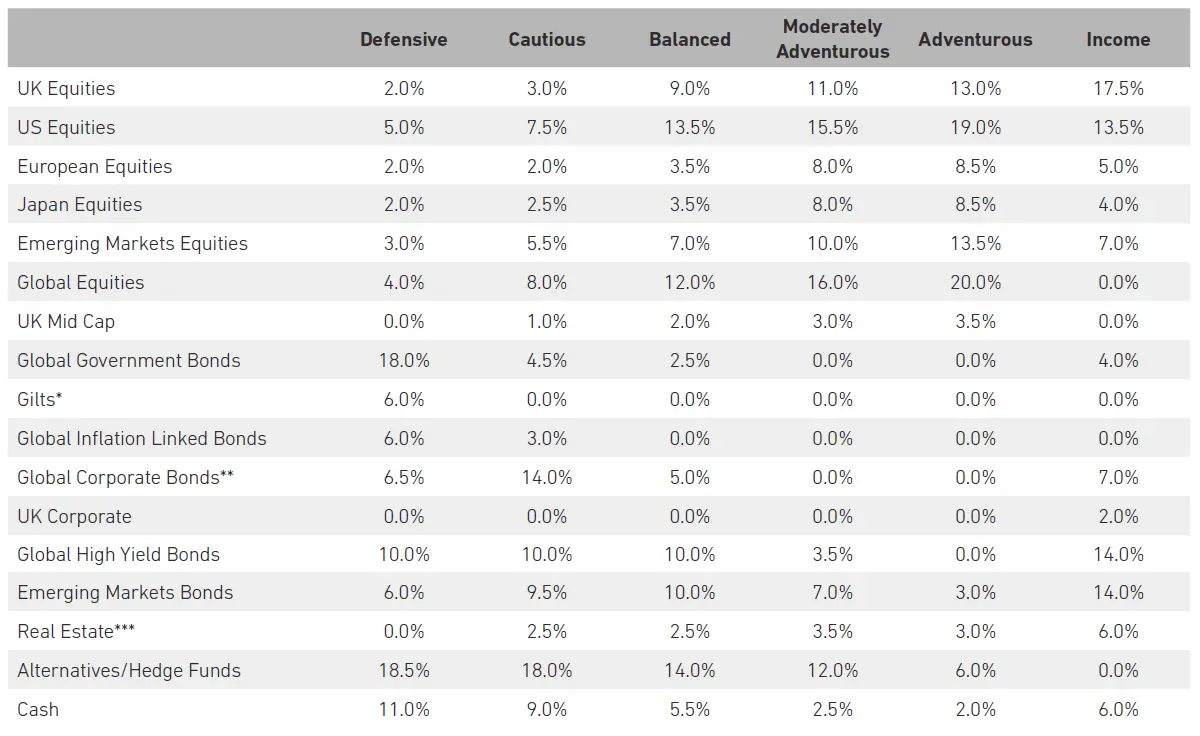

Detailed asset allocation

Source: 7IM. *Includes Short Term Sterling Bonds **Includes Convertible Bonds ***Includes Infrastructure

Read more from 7IM

7IM and Succession have come together to give your clients access to a range of risk-rated, low-cost model portfolios to help them achieve their goals.