Talking Tactics

Modern sports is full of numbers.

A couple of decades ago, the team of a marathon runner, cricketer, or tennis player likely consisted of a coach, an agent, and perhaps a physio. Most of these team members would be ex-athletes themselves. Now, almost all serious athletes – whether individuals or teams – have a data analyst on call.

After all, more than most things, succeeding at sport is about doing the exact same thing, time and time again, better than anyone else. And data is crucial. The "marginal gains" approach from Sir David Brailsford’s British cycling team is a great example of this. The "Moneyball" success in US baseball is another. And even modern football analysis is in terms of 'xGs' and 'progressive carries'.

Of course, it’s not just your own performance that’s worth collecting data on – it’s also your possible opponents’. Do they prefer to lead, or come from behind? Are they easily riled by a crowd? Do they tend to serve down the middle on big points?

Because although the usual advice is to “play your own game”, it’s important to know what you’re facing...

The investment “opponent”

Of course, investing has always attracted data nerds. For investors, even if we don’t change the way we invest, it’s important to have an idea of what might happen next. What kind of environment might we be heading into - as that can affect how our portfolios might perform. What’s the game plan?

This is always challenging, but the last few years have proved particularly difficult. The Covid pandemic, the emergency stimulus, the inflation that followed, and the resulting interest rate hikes all happened more quickly than any previous data analysis prepared us for. But now, four years on, the aftershocks may finally be fading.

Supply and demand imbalances have mostly been resolved, while the last gasps of stimulus cash are being spent. Spending has also moderated with retail sales in the US flatlining this year, with recent poor earnings results from consumer goods companies such as Nike, Levi’s and H&M, suggesting there’s less disposable income available.

Taking it all together, we can suggest that the next 12 months are very unlikely to see higher interest rates, but nor will they see rates fall sharply. The global economy is likely to grow sluggishly, without the same post-COVID confidence boom.

At the margins, the last few years of interest rate hikes are starting to weaken parts of the global economy – as they are designed to. The housing sector isn’t firing on all cylinders and employment isn’t growing as strongly as it was.

As a result, inflation across the world is settling down to a more tolerable level. That’s essential for businesses looking to plan their future investments. For the past few years, they’ve not managed to get an accurate picture of the “true” level of demand for their product. Was it artificially suppressed in Covid? Was it artificially boosted by stimulus? Those ripples are fading, and surveys of businesses and consumers point towards an expectation that the future will be calmer.

In terms of knowing the opponent, it looks like the next 12 months will be a tougher environment for companies to make strong profits. Ordinarily, that would mean an environment of lower interest rates, to try and pep things up.

However, with the wild card of inflation still very much in the public consciousness, central banks won’t go wild with rate cuts. Reduce interest rates too early, spark growth too quickly and maybe inflation surges again. The lesson of history is that high inflation is a catastrophe – and it’s better to be cautious rather than blasé (not that many central bankers are blasé people…).

Taking it all together, we can suggest that the next 12 months are very unlikely to see higher interest rates, but nor will they see rates fall sharply. The global economy is likely to grow sluggishly, without the same post-Covid confidence boom. And that’s an outcome a central banker would be very happy with. Arguably, it’s their gameplan…

Investment tactics

There’s only so much you can know about your opponents. They can always surprise you with a new player, an innovative tactic or a different style of play. When it comes to investing, uncertainties around the outlook remain. How far will central banks go? Will inflation return? And which way is economic growth heading?

Just like in sports, we never know the answers to these questions beforehand. And so, our gameplan needs to acknowledge that. At 7IM, our gameplan is to hold a diversified portfolio with some offbeat positioning that should help over the next 12 months:

Overweight bonds

Bonds are supposed to be the safe assets, while equities are the "higher risk" ones. However, in the last few years, this has flipped on its head. While equities have been up materially, we’ve seen government bonds – the safest assets of them all – fall by double digits.

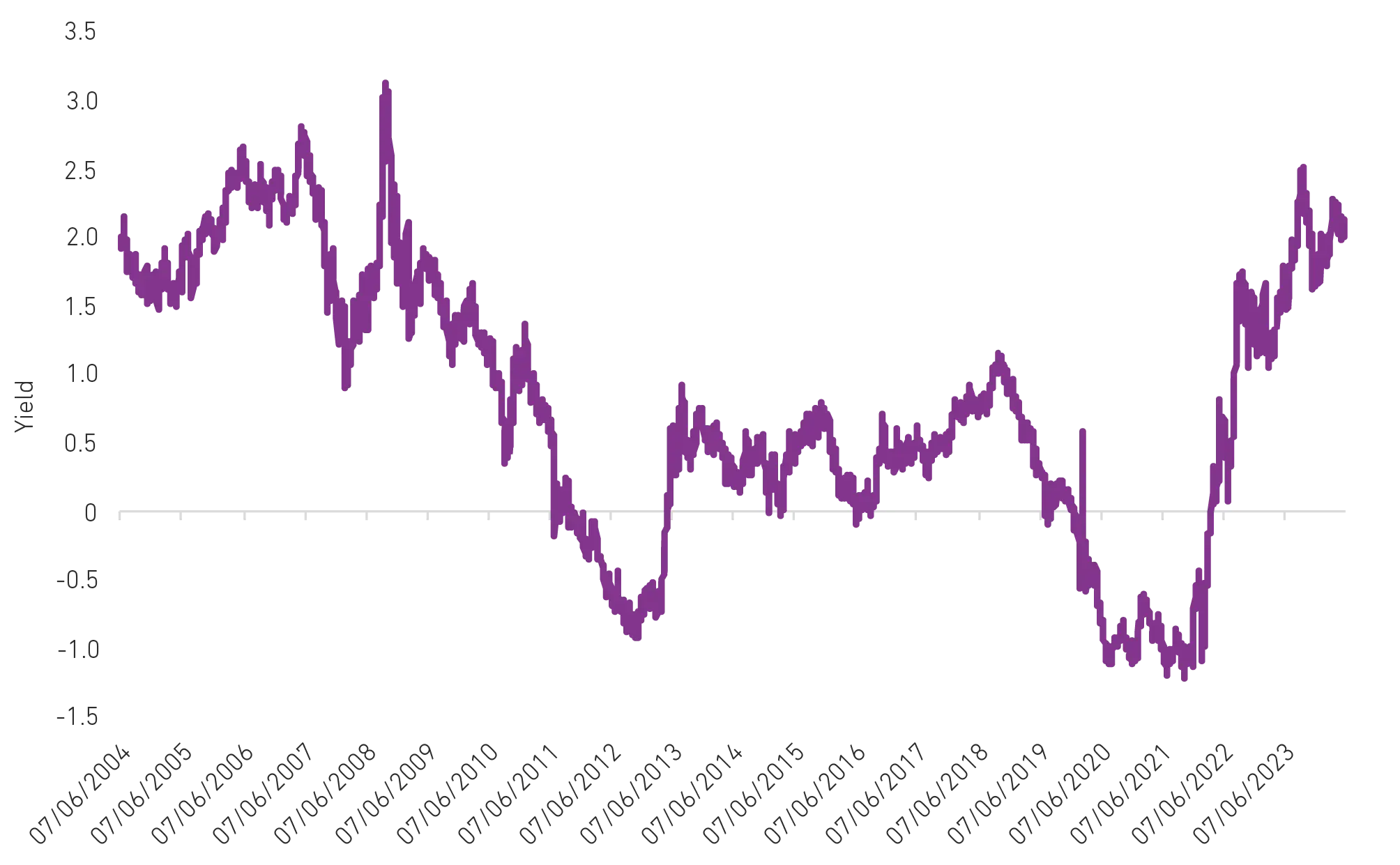

Surging inflation and interest rates are the main culprits – bond prices and rates move in opposite directions. This is offering investors a historic opportunity to invest in real yields – income that is higher than inflation – at levels we haven’t seen in over two decades (see chart). That’s a free shot on goal, in our view.

US 10-year real yields (Bond yield minus inflation)

Source: Macrobond/7IM

Alternatives

Holding bonds will be key to delivering outperformance over the coming years. If the economy weakens, central banks are likely to dust off their old playbook of cutting interest rates. And those rates fall, bond prices will rise – hence our overweight above.

However, we shouldn’t forget the experience of the last few years. Surprises can happen. And so, we look to ‘diversify our diversifiers’. If the game changes, and bonds don’t play the role they have in the past, we own a portfolio of alternative strategies ready to deliver diversifying returns, much like they did in 2022-23.

Healthcare

The global healthcare sector remains one of our favorite long-term investments. Earnings stability helps to weather economic downturns, valuations are attractive, and it’s coming off one of the worst periods of performance in decades. As always in sports, form is temporary, but class is permanent. And at the same time, if there’s one area where AI really can make a difference, it’s likely to be here.

Metals and mining

Metals and mining stocks are as solid as it gets – net debt is close to zero, profit margins remain elevated and dividend yields are higher than the markets. Add on to that, these companies will be at the centre of the climate transition. The long-term tailwind is clear. And we’re paid handsomely to wait.

Japanese Yen

As US interest rates have risen, Japanese interest rates have stayed low – and so Japanese investors have naturally moved some of their money out of Japan, weakening the currency in the process.

But this won’t last forever. If a currency gets too cheap, exports will soar, which eventually pushes the currency back up. Timing is tricky, but this is why holding on to cheap currencies pays off in the long run.

At the time of writing, the Japanese Yen is the cheapest it has ever been – ~40% below fair value estimates. At the same time, US inflation is easing, which should lead to falling rates. This will lead some Japanese investors to repatriate their money, boosting the currency.

And of course, in a world in which the US economy starts to struggle, the Yen would benefit even further as its safe haven status becomes in demand – so the position can play a defensive role too.

This is offering investors a historic opportunity to invest in real yields... a free shot on goal.

More from 7IM