Quarterly Rebalance Commentary

Overview

Since the model rebalance in mid-February, markets have had a huge amount of news to digest.

During February, markets struggled despite some economic data that would usually be considered positive. The stagflationary environment that we find ourselves in can make it hard to know what to make of some data points. An example of this in February was the lower-than-expected US unemployment figure wasn’t seen as a positive. If unemployment is the necessary evil to bring inflation down, it’s hard to know whether low unemployment figures are a good thing.

March was an extremely eventful month for markets. At the start of the month, Silicon Valley Bank collapsed as their poorly managed balance sheet risk led to a loss of confidence in the bank and ultimately, heavy deposit flight. Then, the seemingly unrelated Credit Suisse also experienced deposit flight to the point that they could not meet redemptions leading to the Swiss government brokered deal with UBS.

After a manic Q1 for markets, an uneventful April and May have been a relief. Equities posted modest gains, with the FTSE 100 leading the way on account of some positive signs from inflation data. There was some noise around the potential issues that the US debt ceiling might create, but markets did not respond much.

Core investment views

At 7IM, we have several long-term core views that help to guide our investment decisions and allocations within portfolios.

Over the next 12 months, we think that the global economy will slide into a recession. In this environment, it is important to rely on a stable identity. Economic uncertainty creates fear and investor sentiment tends to overreact to economic turning points. Going forward, we believe that:

- Inflation will come down. Goods inflation is slowly normalising, and supply chain pressures are going

- Central banks are getting close to the end of their hiking cycles, but there is still a bit more work to do

- A US recession is highly likely. Most leading indicators are pointing towards a recession, but the recession shouldn’t be too long or deep.

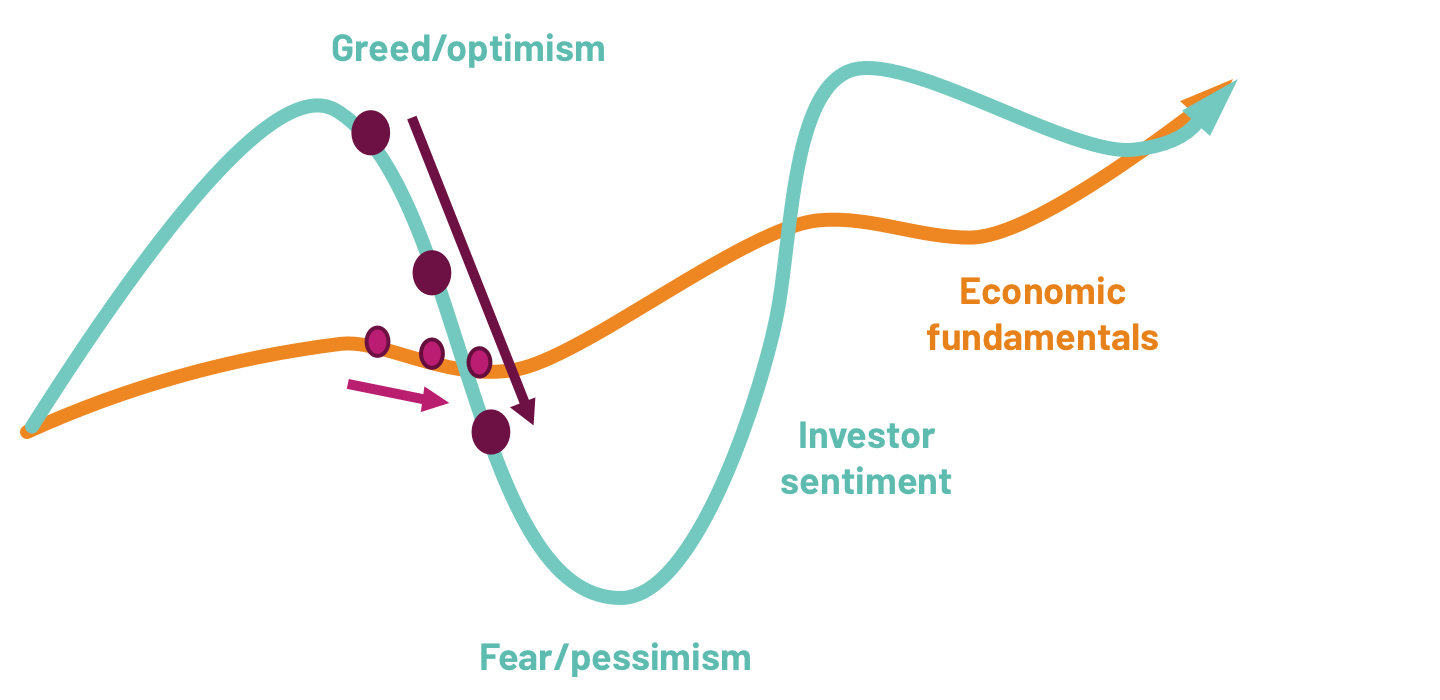

Investor sentiment overreacts to economic turning points…

... with slightly weaker data leading to panic right now

Source: 7IM

And so, investors are starting to worry about what’s next for financial markets. Economic data isn’t likely to stabilise until next year. Equity markets are unlikely to perform well.

We know our investment identity helps us to deliver in just these kinds of environments. We have positions that can generate returns despite this volatile backdrop.

At a headline asset class level, our portfolio positioning has moved underweight credit since last quarter:

Tactical Themes

Asset allocation changes

We have made the following tactical changes to portfolios in this quarterly rebalance:

- Reduced our weight in AT1s. We still have a lot of conviction in AT1s as an asset class. European banks are fundamentally sound, and AT1s are offering very attractive yields. However, given recent volatility, we believe that downsizing the position is prudent from a risk management point of view.

- Added to our climate change position. The long-term case of this position remains very strong, and we believe now is an opportune time to add, given recent market moves.

Manager changes

This quarter, there have not been any major manager changes across our model portfolios.

You can download the commentary as a PDF here.