Putting the Autumn Budget in perspective

Finally, the first incoming Labour budget in 27 years* has been delivered. There are a lot of personal finance changes to digest and I’ll leave that space to the relevant experts – watch this space.

Here’s my take:

I thought it was brave of Rachel Reeves to take a swing at Kwasi Kwarteng’s chaotic mini-budget before the impact of hers was digested by the market, but, you know, I love the confidence.

And to be fair, it seems to have been justified. Financial markets don’t appear to have seen anything too alarming in what the Chancellor had to say.

Market response

Basically, nothing to see here (as you’d hope after the last two months of speculation and leaking).

- The big, global companies in the FTSE 100 are down a little, but not out of line with other European markets. The more UK-focused FTSE 250 companies are up a little – but again, nothing to really relate to what’s going on in the Houses of Parliament. The very small-cap AIM market has actually bounced by around 3%, possibly anticipating worse than the 20% inheritance tax rate.

- UK Gilt yields have declined a little – no chaotic scenes here; in fact, the promise to spend less than the country makes in tax by 2027 was very well received.

- The Pound is broadly unmoved, and still around August levels vs. the US Dollar

Economic Implications

Just in case you missed it the Chancellor is prettttty keen on “investment” (I stopped counting at 50 mentions). And, cards on the table, so are we.

And the tone is definitely encouraging about investing in capital**. There are lots of specific schemes receiving specific funding over multi-year periods with lots of exciting buzzwords like gigafactory and aerospace and AI.

But from our perspective, genuine growth can only be built on solid foundations; investment in the basics is what delivers over the long term. Whether it’s potholes, childcare or a spotty WiFi connection, the theory is simple – if you don’t have to worry about the simple things, you’ve got more time to do things that matter for the economy; whether that’s start a business, meet a friend for a coffee, or go for a run.

So it’s actually the less exciting proposals about road repairs, broadband in rural areas or the Trans-Pennine transport upgrades which are most important. There’s no point having an access road which punctures tyres, a state-of-the-art battery factory that can’t get online, or social housing in areas which can’t be reached by bus or train.

And execution of these is vital – both economically and psychologically. Like anything, in order to be trusted, you have to get the basics right: if you can’t nail the coffee order, you won’t be trusted to pitch the big clients. And if the government gets the potholes fixed, they’ll be given more leeway to do more impressive things in the future.

The big topics – NHS, education, energy – are slightly less graspable. However, given our research into healthcare stocks as part of our portfolios, we think that the idea of moving towards prevention, rather than cure, is the right long-term approach.

We’ll need to take a look at the details to figure out what’s not being said, or where the numbers might need some explaining, but if the tax increases are used to fix the small problems quickly, and genuinely tackle the big problems like the NHS and the education system, the money might well be considered well-spent. It’s all about making it happen, though.

Investment Implications

As we’ve said numerous times, the UK Budget is (usually) not a market-moving event. We watch it carefully, of course, but we very rarely think it merits portfolio action or preparation.

Now it may well be that there IS some market volatility this week. But the likely catalysts are the Q3 earnings results from five of the largest companies in the world.

Already, we’ve had Google report $88bn of sales in the last three months (that’d plug a few budgetary gaps…).

And tonight we have Facebook and Microsoft, before Amazon and Apple on Thursday.

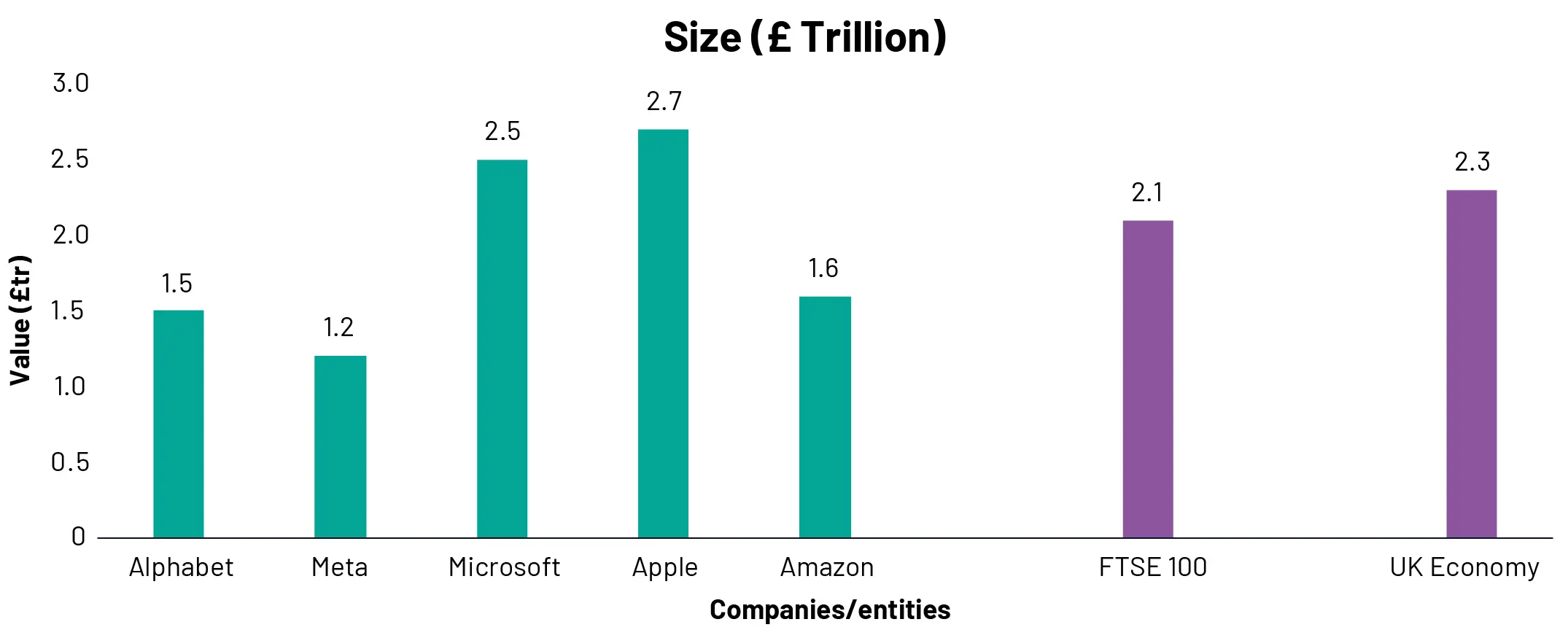

How’s this for a little bit of a chastener to patriotic pride – comparing the size of those business, the UK market, and the UK economy.

Source: 7IM/Factset/ONS. Data as at 30 October.

On a serious note, it’s important to remember (from the investment perspective) that we own companies, not economies. And the prospects for most companies across the world right now look pretty reasonable.

* And 14 years since its last Budget delivery

** There’s a little bit of accounting going on (with assets being taken off liabilities), but you know what, that’s no worse that we see in the balance sheets of large businesses.

Watch now

Ben Kumar offers his analysis on the government's Autumn Budget.

More from 7IM

I confirm that I am a Financial Adviser, Solicitor or Accountant and authorised to conduct investment business.

If you do not meet this criteria then you must leave the website or select an appropriate audience.